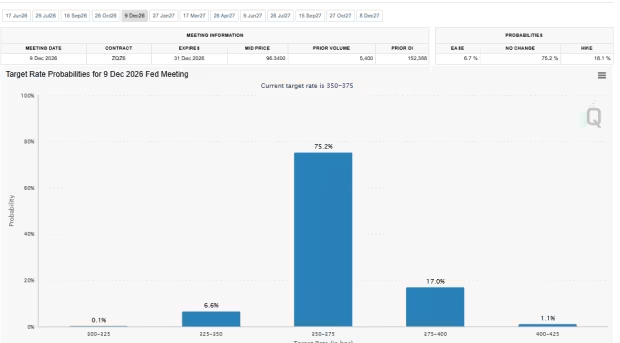

For the first time in the current monetary policy cycle, traders now see the Federal Reserve's next interest rate move as a hike rather than a cut, marking a dramatic reversal from the dovish expectations that dominated markets through 2025. According to the CME Group's FedWatch tool, which tracks pricing in 30-day federal funds futures, the probability of a rate hike at the December 2026 Federal Open Market Committee meeting has surged to 51%. The odds climb to roughly 60% for the January 2027 meeting and exceed 71% for the March 2027 meeting. This shift comes as inflation readings continue to surprise to the upside, Treasury yields spike, with the 30-year bond reaching the psychologically critical 5% level, and early signs of stagflation emerge across the economy. The market has effectively abandoned expectations for any further easing: futures markets now show below 1% odds of a June rate cut, and Kalshi, the prediction market platform, prices a 68% probability that the Fed delivers no cuts at all in 2026. This matters because the repricing of rate expectations is already cascading through bond markets, stock valuations, and corporate borrowing costs, reshaping the investment landscape for the second half of the decade.

How the FedWatch Tool Flipped from Cuts to Hikes

The CME FedWatch tool, which derives probabilities from the pricing of 30-day federal funds futures contracts, has undergone a structural shift in recent weeks. Throughout 2025, the tool consistently showed a majority probability of further rate cuts, reflecting the 75 basis points of easing the Fed delivered last year. At the April 2026 meeting, the Fed held rates steady, and the futures curve began to flatten. The critical inflection point came when the December 2026 contract started pricing in a higher probability of a rate increase than a decrease. The math is straightforward: the implied federal funds rate for the December meeting now sits above the current effective rate, meaning the market expects the Fed to tighten. The January 2027 contract shows a roughly 60% probability of a hike, and the March 2027 contract pushes that figure above 71%. These are not fringe bets. They are the central scenario priced by the deepest and most liquid interest rate derivatives market in the world. The shift reflects a cumulative repricing of inflation expectations, with recent CPI and PCE readings consistently exceeding consensus forecasts. The FedWatch tool's methodology weights all fed funds futures contracts across the term structure, so the move to a hike-dominant probability distribution signals that the entire forward curve has repriced. The tool now assigns a 51% probability to a December hike, up from just 15% one month ago, confirming the speed of the repricing.

Where the $570M in Annual Interest Income Flows

The surge in Treasury yields directly impacts the P&L of banks, asset managers, and retail savers, but the magnitude of the transfer is often underappreciated. The 30-year Treasury yield hitting 5% represents a full percentage point increase from its 2025 lows, adding roughly $570 million in annual interest income for every $100 billion in duration exposure held by banks and institutional investors. For the U.S. banking system, which holds approximately $3.5 trillion in Treasury and agency securities, this yield increase translates into tens of billions of dollars in additional net interest income over the next twelve months, assuming banks can reinvest maturing securities at these higher rates. However, the flip side is mark-to-market losses on existing bond portfolios. The FDIC reported that unrealized losses on securities held by U.S. banks exceeded $700 billion at the end of the first quarter, and the recent yield spike has likely pushed that figure higher. For retail savers, the average savings account pays a paltry 0.38% according to FDIC data, meaning the vast majority of this yield increase accrues to institutional holders and high-yield deposit accounts, not the typical consumer. The 10-year yield, now at its highest level in about a year, drives mortgage rates and corporate borrowing costs higher, compressing spreads in credit markets and forcing a repricing of risk assets across the board. The yield surge also raises the cost of new debt issuance for corporations, which face higher coupon payments when they refinance maturing bonds. This dynamic tightens financial conditions without any action from the Fed, effectively doing some of the central bank's work for it.

The Competitive Reshuffle: Winners and Losers in a Hike Regime

The shift to a rate-hike narrative creates clear winners and losers across the financial ecosystem. Money-center banks with large securities portfolios and floating-rate loan books, such as JPMorgan Chase, Bank of America, and Citigroup, benefit from wider net interest margins as short-term rates rise and the yield curve steepens. Regional banks, still scarred by the 2023 deposit runs, face renewed pressure if deposit costs rise faster than asset yields. On the asset management side, firms like BlackRock and PIMCO, which manage massive fixed-income funds, see inflows into short-duration products and money market funds as investors chase higher yields. The winners also include online high-yield savings platforms and brokerage cash sweep programs, which can offer depositors rates that far exceed the FDIC average. The losers are more concentrated: highly leveraged companies that loaded up on floating-rate debt during the low-rate era now face refinancing costs that could push them into distress. The commercial real estate sector, already under pressure from remote work trends, faces a double blow of higher capitalization rates and tighter lending standards. Private equity firms that relied on cheap debt for leveraged buyouts will find deal economics far less attractive. The broader stock market, as Barron's noted, is being spooked by the yield surge, with growth stocks and high-duration equities, particularly in the technology and biotech sectors, experiencing multiple compression as discount rates rise.

Downstream Effects on Hyperscalers, Fabs, and Enterprise Buyers

The rate hike repricing cascades through the capital-intensive sectors of the economy with particular force. Hyperscalers such as Amazon Web Services, Microsoft Azure, and Google Cloud have committed hundreds of billions of dollars to data center construction and AI infrastructure over the next five years. A 100-basis-point increase in the risk-free rate raises their weighted average cost of capital by roughly the same amount, making the net present value of long-duration AI projects less attractive. For chip fabricators like TSMC, Samsung, and Intel, which are building advanced fabs with multi-year construction horizons and payback periods extending to the end of the decade, the discount rate shift could delay or shrink planned capital expenditure. The CHIPS Act subsidies provide some buffer, but private capital allocation decisions will tighten. Enterprise buyers of IT hardware and software, facing higher borrowing costs and a slowing economy, will push out upgrade cycles and scrutinize large contracts more carefully. The bond market turmoil also affects the financing of semiconductor equipment makers like ASML and Applied Materials, which rely on both customer capex and their own debt issuance. On the regulatory front, the FDIC and other banking agencies will need to reassess the interest rate risk in the banking system, potentially requiring higher capital buffers for duration mismatches and stress-testing scenarios that assume a policy rate above 6%. The combination of high inflation and slowing growth, the classic stagflation cocktail, creates a policy environment where the Fed has limited room to ease even if the economy deteriorates, leaving policymakers caught between a price-stability mandate and a growth mandate that now point in opposite directions.

The Policy Signal: What the Market Is Telling the Fed

The FedWatch tool's shift to a hike-dominant probability distribution is more than a technical market indicator. It is a direct signal that the bond market has lost confidence in the Fed's ability to deliver a soft landing. By pricing in rate hikes, traders are effectively telling the Fed that its current policy stance is too accommodative given the persistence of inflation. The 30-year yield reaching 5% is a particularly potent signal, as the long bond reflects the market's view of the structural inflation and growth trajectory over the next three decades. Kevin Warsh, a former Fed governor, has been among the voices warning that the Fed risks falling behind the curve again if it does not acknowledge the inflation persistence. The market's message is that the neutral rate of interest, the rate that neither stimulates nor restricts the economy, is likely higher than the Fed's current estimate. This has profound implications for the Fed's forward guidance and the dot plot. If the Fed is forced to hike in December or early 2027, it would mark the first tightening cycle following a cutting cycle that lasted only 18 months, an unprecedented reversal in modern monetary history. The policy signal also extends to fiscal policy: higher rates increase the cost of servicing the federal debt, which at $36 trillion and growing, adds pressure on Congress to address the deficit. The market is effectively imposing discipline on both monetary and fiscal authorities.

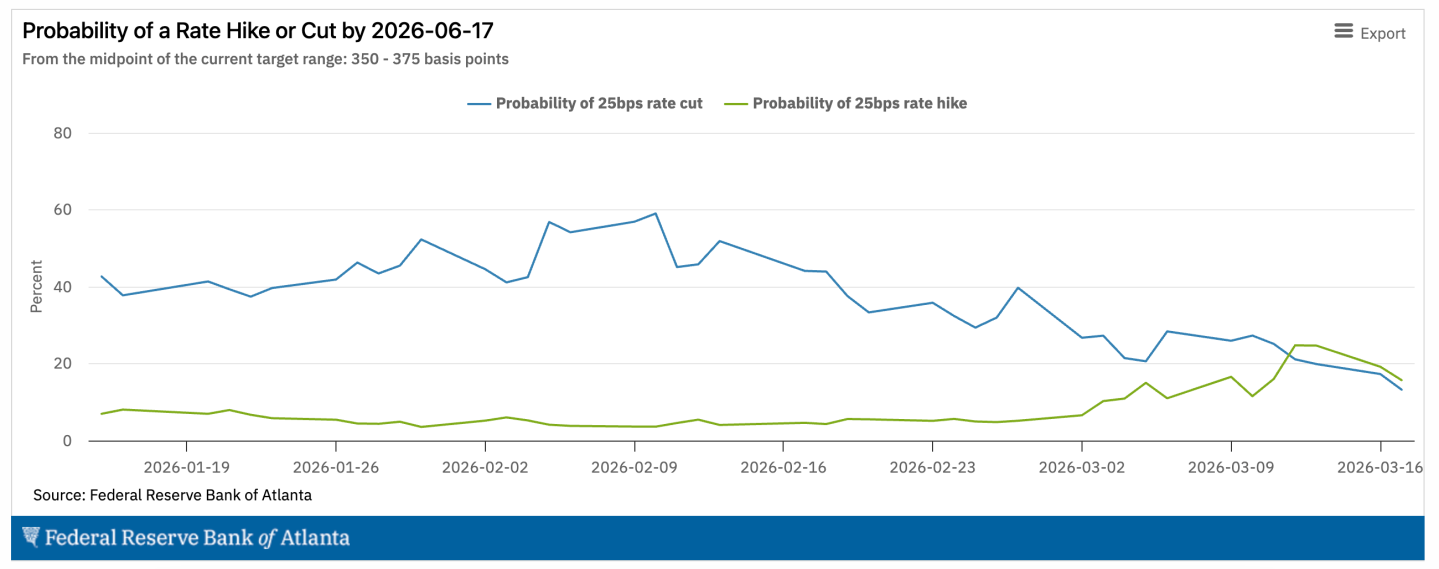

The central scenario is that the Fed holds rates steady through the summer and fall, watching inflation data and labor market cracks with equal concern. If the December hike probability continues to rise toward 70% or 80%, the Fed will face intense pressure to deliver hawkish rhetoric at its June and September meetings, pre-committing to a tightening path. The risk of overtightening, raising rates into an economy that is already slowing, is real, but the market is signaling that the greater risk is allowing inflation to become entrenched. Kalshi, the prediction market platform, prices a 68% probability of zero Fed cuts in 2026 and a 50% chance of a hike before July 2027, numbers that reinforce how decisively the easing narrative has collapsed. For investors, the playbook is clear: reduce duration, favor floating-rate instruments, and prepare for a regime where cash yields 4% or more while equity valuations compress under a higher discount rate. The era of easy money is definitively over, and the bond market has already moved on.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.