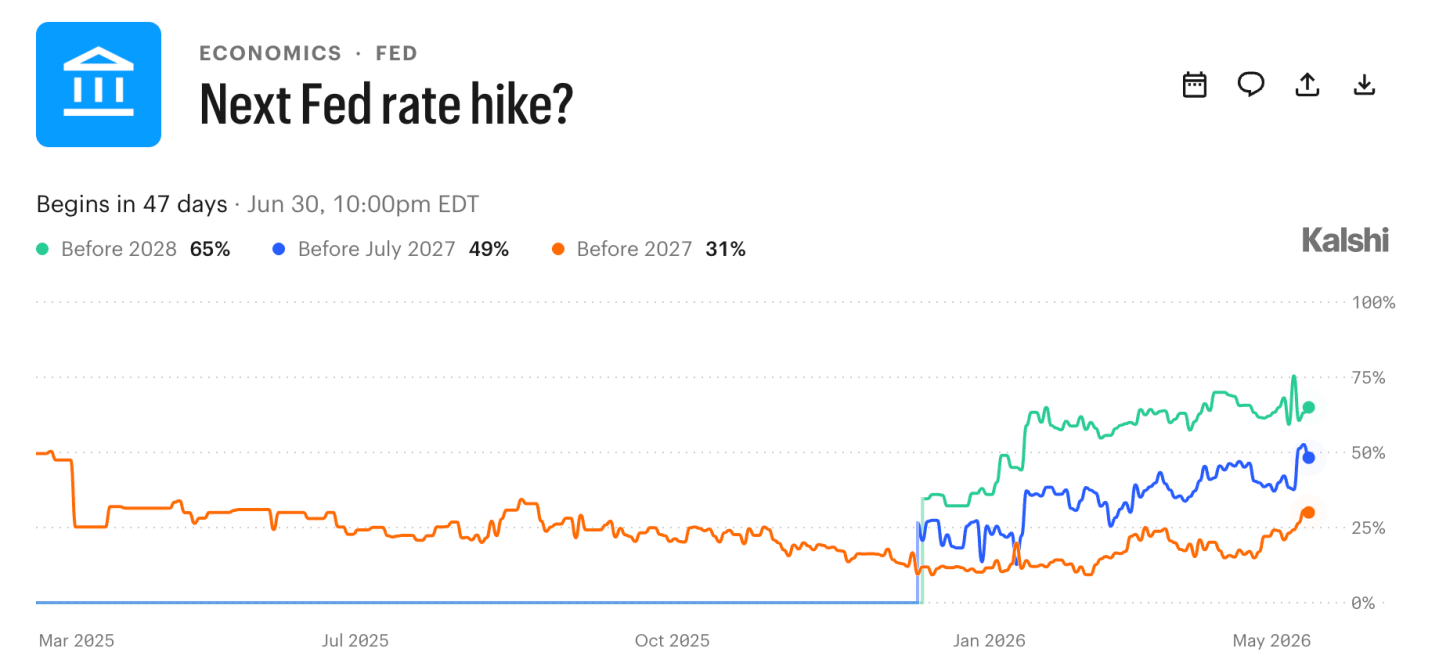

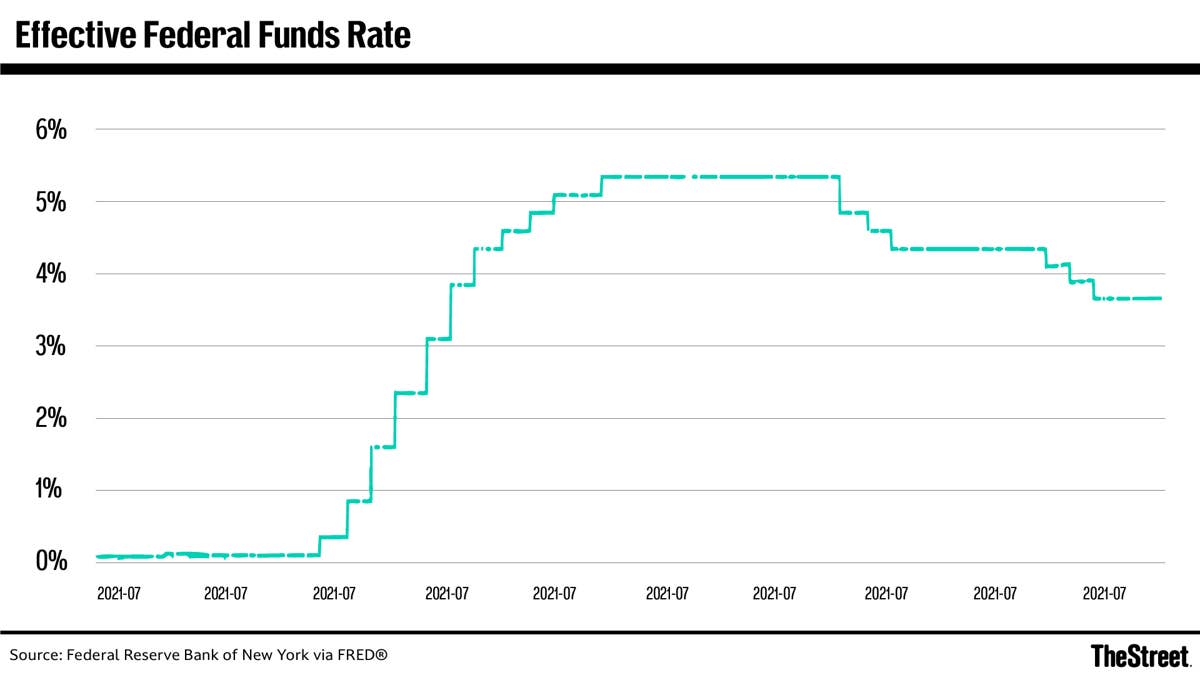

Investors have dramatically repriced the Federal Reserve's path, now assigning a roughly 60% probability to a 25-basis-point rate hike by the January 2027 Federal Open Market Committee meeting, according to CME Group's FedWatch Tool. The surge in hawkish bets follows hotter-than-expected Consumer Price Index and Producer Price Index readings for April 2026, which shattered the narrative of a central bank on hold. The Fed's policy rate has sat at 3.50%–3.75% since December, the final months of Jerome Powell's chairmanship, but the bond market is already moving ahead of the central bank. The 2-year Treasury yield has climbed above 4%, the 10-year yield reclaimed 4.5%, and the 30-year yield topped 5%. These levels effectively tighten financial conditions before the Fed acts. The probability of a hike by the December 2026 meeting is now above 50%, a coin toss that was unthinkable just weeks ago. This repricing lands squarely on the desk of incoming Fed Chair Kevin Warsh, who takes over from Powell at a moment when the central bank's credibility on inflation is being tested by geopolitical shocks, including the Iran war and disruption at the Strait of Hormuz, which have pushed energy prices higher. Why this matters now: The market is forcing the Fed's hand before Warsh has even held his first press conference, creating a high-stakes messaging challenge that will define the early days of his tenure.

The CPI and PPI data that broke the disinflation trend

The shift in rate-hike expectations is rooted in two consecutive data releases that broke the disinflation trend. The April CPI report came in above consensus, followed by a PPI print that reinforced the narrative that price pressures are reaccelerating. The FedWatch Tool, which tracks fed-funds futures pricing, moved from a roughly 40% probability of a hike on Thursday to 50% on Friday, and then to 60% by the start of the following week as the data sank in. The implied probability of a 25-basis-point hike by the December FOMC meeting now sits above 50%, meaning the market sees a coin-flip chance that the Fed moves before year-end. This is a sharp reversal from the start of 2026, when the consensus view was for rate cuts. The current policy rate of 3.50%–3.75% is already above the neutral rate estimates of many Fed officials, but the market is now pricing in a higher terminal rate. The bond market has effectively pre-hiked: the 2-year yield, at above 4%, is trading well above the Fed's upper target of 3.7%, a condition that historically has preceded actual policy tightening. Brij Khurana, a fixed-income investor at Wellington Management, has noted that the market is doing the Fed's work for it, but this also creates a risk of overtightening if the central bank follows through. The probability shift is not just a reaction to one month of data. It reflects a structural reassessment of the inflation regime, driven by supply-side shocks that monetary policy cannot easily address. The April CPI core reading came in at 3.2% year-over-year, above the 3.0% consensus, while the PPI final demand figure hit 2.8%, also topping expectations.

How the P&L math changes for banks

The repricing of rate-hike expectations has immediate and divergent implications for the largest U.S. banks. For Bank of America, Citigroup, and JPMorgan, a higher-for-longer rate environment boosts net interest income, as they can reprice loans upward faster than they raise deposit rates. JPMorgan, which has been the most vocal among the big four about the benefits of elevated rates, stands to gain the most from a hike cycle that extends into 2027. The bank's net interest income has already benefited from the Fed's hold at 3.50%–3.75%, and a move to 3.75%–4.00% would add billions in annual revenue. Citigroup, with its large credit card portfolio, also benefits from rising rates, as card APRs are tied to the prime rate. However, the picture is different for Wells Fargo, which has publicly reaffirmed its forecast for two quarter-point rate cuts in 2026, even after the hot CPI and PPI data. The bank reversed its April 6 position of dropping its rate-cut forecast, a move that now looks increasingly contrarian. Wells Fargo's bet on cuts reflects its view that the inflation spike is transitory and driven by energy prices from the Iran war and Strait of Hormuz disruption. These factors could reverse. If Wells Fargo is wrong and the Fed hikes, the bank will face a mark-to-market hit on its securities portfolio and pressure on its net interest margin, as it has been slower than peers to reposition its balance sheet for higher rates. The divergence in bank forecasts creates a trading opportunity: short Wells Fargo, long JPMorgan, as the market prices in a hike that Wells Fargo is betting against.

The competitive reshuffle in bond markets

The bond market's preemptive tightening is reshaping the competitive dynamics across fixed-income markets. The 30-year yield topping 5% is a psychological threshold that triggers a wave of selling from duration-sensitive investors, including pension funds and insurance companies that must mark their liabilities to market. This creates a self-reinforcing cycle: as yields rise, these institutions sell longer-dated Treasuries to reduce duration, pushing yields higher. The 10-year yield at 4.5% and the 2-year yield above 4% mean the yield curve is steepening, which is a positive signal for banks that borrow short and lend long, but a negative for mortgage REITs and other leveraged duration plays. CME Group's FedWatch Tool has become the most-watched pricing mechanism in the market, displacing the Fed's own dot-plot as the primary guide to rate expectations. This shift in pricing power from the central bank to the derivatives market is a structural change: the Fed under Warsh will have to respond to market pricing rather than lead it. The high-yield savings rate market has also responded, with rates reaching up to 5.00% at some online banks, according to the Wall Street Journal. This creates a competitive dynamic where retail depositors can earn more than the Fed's policy rate, forcing banks to raise deposit costs even if the Fed does not hike. The result is that financial conditions are tightening across the board in government bonds, corporate credit, and retail deposits before the Fed has taken any action. This preemptive tightening is the bond market's way of doing the Fed's job, but it also risks overshooting if the central bank then adds its own tightening on top.

Downstream effects on corporate borrowing and capex

The rise in bond yields is already transmitting to corporate borrowing costs, with investment-grade credit spreads widening and high-yield issuance slowing. Companies that were planning to refinance debt in the second half of 2026 are now facing a 10-year yield above 4.5%, which translates to all-in borrowing costs of 5.5%–6.0% for investment-grade issuers and 8%–10% for high-yield. This will force CFOs to delay or cancel capex plans, particularly in interest-rate-sensitive sectors like housing, commercial real estate, and autos. The unemployment rate at 4.3% in April, while still low by historical standards, is up from the 3.4% trough in 2023, and further tightening from the Fed could push it higher. The geopolitical overlay (the Iran war and Strait of Hormuz disruption) adds a supply-side inflation component that the Fed cannot address with rate hikes. Higher energy prices reduce real household income, which in turn reduces consumer spending, creating a stagflationary dynamic that is the worst outcome for corporate earnings. The bond market's preemptive tightening is already doing the work of slowing the economy: mortgage rates are moving back toward 7%, auto loan rates are above 8%, and credit card rates are approaching 25%. The Fed, under Warsh, faces a dilemma: if it follows the market and hikes, it risks overtightening into a slowing economy; if it holds steady, it risks losing credibility on inflation. The downstream effects on corporate balance sheets will be felt in Q3 and Q4 earnings reports, as companies report higher interest expense and lower demand.

What the Warsh Fed signals about the policy regime

Kevin Warsh's confirmation as Fed Chair marks a regime change in monetary policy communication and strategy. Warsh, a former Fed governor, has been critical of the Powell Fed's forward guidance framework, arguing that it created market distortions and reduced the central bank's flexibility. His first major test is the market's repricing of rate hikes, which forces him to either validate or push back against the market's hawkish bets. The messaging challenge is acute: if Warsh signals that the Fed is open to a hike, he risks accelerating the bond market selloff and tightening financial conditions further; if he pushes back, he risks being seen as dovish in the face of rising inflation. The probability of a hike by January 2027 at 60% means the market expects Warsh to act quickly. The geopolitical factors driving inflation (the Iran war and Hormuz disruption) are outside the Fed's control, but they create a narrative that the central bank is behind the curve. Warsh's strategy will likely be to emphasize data dependence while signaling a willingness to act if inflation does not moderate. This is a departure from the Powell era, where the Fed was more explicit about its reaction function. The market is now pricing in a higher terminal rate than the Fed's own projections, which means Warsh will have to either raise the dot-plot or accept that the market is setting policy. The high-yield savings rate at 5.00% is a signal that the retail market is already pricing in a hike, and Warsh will have to decide whether to follow the market or lead it. The regime shift is from a Fed that cut rates aggressively in 2024 and 2025 to one that may need to hike in 2026 and 2027, a reversal that will define Warsh's legacy.

The market's repricing of rate hikes is not a temporary blip but the beginning of a structural shift in the monetary policy regime. The combination of geopolitical supply shocks, a tight labor market at 4.3% unemployment, and the bond market's preemptive tightening creates a self-reinforcing cycle that will force the Fed's hand. Kevin Warsh inherits a central bank that has lost control of the narrative, with the derivatives market setting policy expectations rather than the FOMC. The probability of a hike by January 2027 at 60% will likely rise further if the May CPI and PPI data, due in June, also come in hot. The Wells Fargo forecast for two rate cuts looks increasingly isolated, and the bank will face pressure to revise its outlook. The real question is not whether the Fed will hike, but whether it will hike by December 2026 or January 2027, and whether a single 25-basis-point move will be enough to restore credibility. If inflation continues to run above 3% and the unemployment rate stays below 4.5%, the market will begin pricing in a cycle of hikes, not just one. The bond market has already started that process, and the Warsh Fed will have to decide whether to join it or fight it.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.