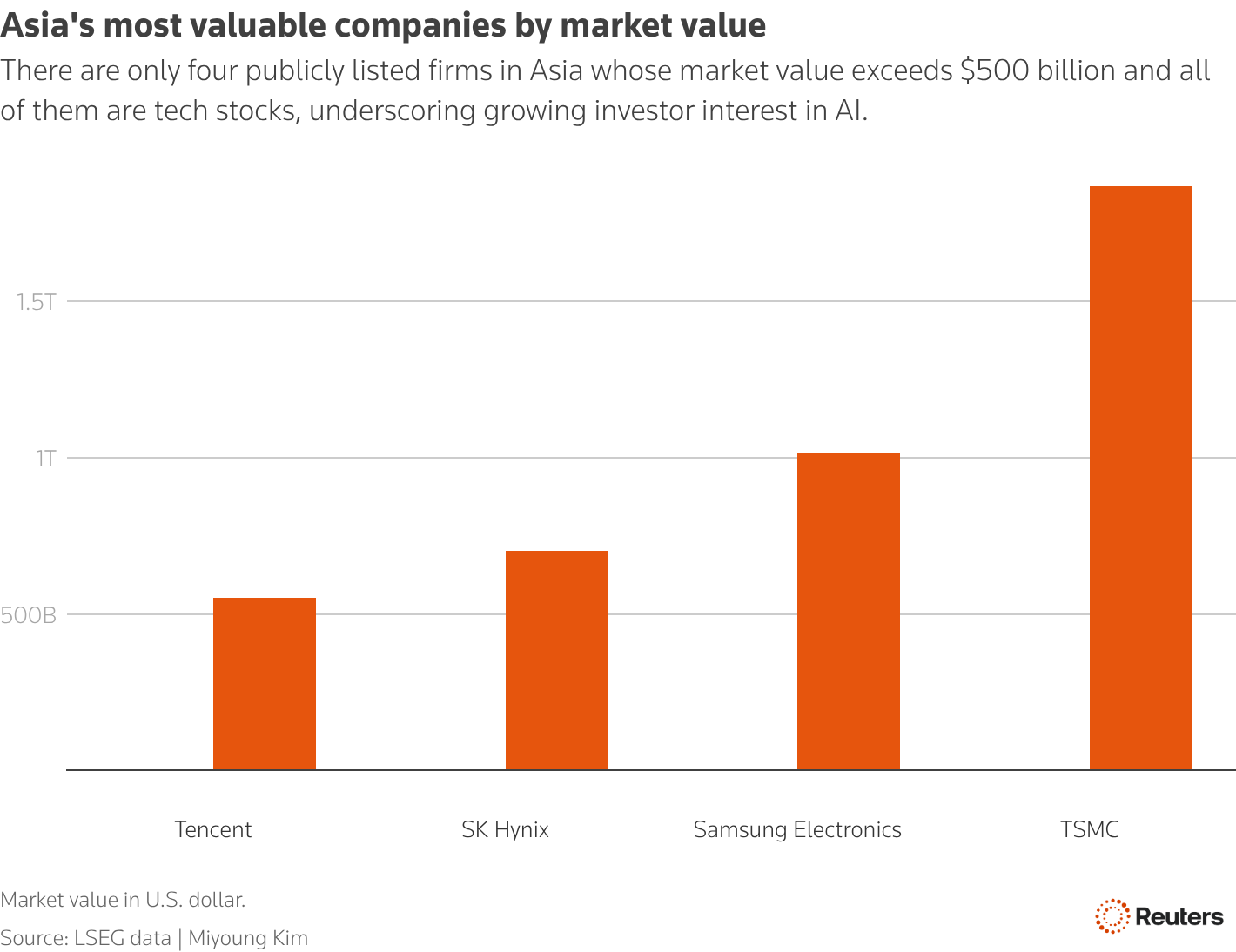

Taiwan is now "well over 80%" exposed to AI-related revenue streams, while South Korea sits at roughly 60%, according to UOB and Manulife Investment Management. TSMC alone accounts for more than 40% of Taiwan's Taiex index, with a market capitalization of approximately 58 trillion Taiwan dollars ($1.85 trillion). In South Korea, Samsung Electronics and SK Hynix together made up a record 42.2% of the Kospi in May, after Samsung's market cap surpassed $1 trillion last week. These three companies (TSMC, Samsung Electronics, and SK Hynix) now dominate their home markets to an extent that is distorting index performance, masking underlying economic weakness, and creating acute concentration risk for passive investors. The AI chip boom is not just reshaping global supply chains; it is rewiring the financial architecture of Asia's two most important technology economies. Why this matters now: as AI capital expenditure continues to accelerate, the feedback loop between chipmaker earnings and index returns is tightening, meaning any slowdown in AI demand would hit these markets far harder than any previous tech cycle.

Where the 80% AI revenue exposure comes from

The "well over 80%" figure for Taiwan reflects the proportion of listed companies on the Taiex whose revenues are tied to AI. This includes not just TSMC's own AI chip fabrication, but also its upstream suppliers in advanced packaging, silicon wafer manufacturing, and chip design services. TSMC's $1.85 trillion market cap gives it a weight of more than 40% in the Taiex, meaning the index moves almost in lockstep with TSMC's share price. UOB's analysis shows that when TSMC reports earnings, the Taiex's daily swing is now more than twice as large as it was before the AI boom. For South Korea, the 60% figure is driven by Samsung Electronics and SK Hynix, which together account for 42.2% of the Kospi. Samsung's market cap crossing $1 trillion last week was the catalyst for the record concentration level. Manulife Investment Management notes that the two memory makers now generate over half of their revenue from high-bandwidth memory (HBM) and AI server DRAM, up from less than 10% in 2022.

The exposure is not merely a stock market phenomenon. It reflects a structural shift in the real economy, where AI-related manufacturing now drives a majority of export growth in both countries. Taiwan's Ministry of Economic Affairs reported that semiconductor exports hit a record $65 billion in Q1 2026, with AI-related orders accounting for more than 70% of that figure. South Korea's trade data tells the same story: chip exports surged 42% year-on-year in April 2026, driven almost entirely by HBM shipments to Nvidia, AMD, and Google. The feedback loop between AI demand and index performance is now so tight that analysts at UOB are treating TSMC earnings as a proxy for global AI capex momentum, a role previously reserved for Nvidia itself.

How the P&L math works for TSMC and Samsung

TSMC's revenue from AI accelerators (primarily Nvidia's Blackwell and AMD's MI300 series) is projected to account for over 45% of total revenue in 2026, up from 35% in 2025. This shift has compressed TSMC's operating margin to around 42%, down from 45% in 2024, as the company invests heavily in 3nm and 2nm capacity expansion. However, the absolute dollar profit growth is staggering: TSMC's net income is on track to exceed $40 billion in 2026, driven by AI chip ASPs that are 3x to 5x higher than non-AI chips. That figure, if achieved, would represent a 35% increase over 2025's record result, making TSMC one of the ten most profitable companies in the world by net income. For Samsung Electronics, the AI tailwind is more volatile. Its foundry business is still losing market share to TSMC, but its memory division (specifically HBM3E and the upcoming HBM4) is generating operating margins above 30%. SK Hynix, which leads in HBM3E production, reported a 28% operating margin in Q1 2026. The risk for Samsung is that its foundry losses, estimated at $2 billion annually, are being cross-subsidized by AI memory profits. If HBM prices fall or demand softens, Samsung's consolidated earnings would drop sharply, dragging the Kospi with it.

The competitive reshuffle: who gains and who loses

The concentration of AI chip demand is creating a clear winner-take-most dynamic. TSMC is the undisputed leader in advanced logic fabrication, capturing nearly 90% of the AI chip foundry market. Samsung's foundry share has slipped below 10%, and its attempts to win Nvidia's business for 3nm have so far failed. In memory, SK Hynix holds a commanding lead in HBM3E with over 60% market share, while Samsung trails at 30% and Micron at 10%. The losers are smaller chip designers and fabless companies that lack the scale to secure TSMC's advanced capacity. Companies like Broadcom and Marvell are still growing, but they are being squeezed by allocation constraints: TSMC prioritizes Nvidia and AMD for its 3nm and 2nm nodes.

The concentration also hurts domestic competitors in Taiwan and South Korea. In Taiwan, second-tier semiconductor firms like MediaTek and United Microelectronics Corporation (UMC) are seeing their relative weight in the Taiex shrink as TSMC's dominance grows. In South Korea, non-tech sectors such as automotive and chemicals are being starved of capital as domestic and foreign investors pile into Samsung and SK Hynix. Samsung's cross-subsidization model, where foundry losses are covered by memory profits, is under pressure: its logic foundry reported a $2 billion operating loss in Q1 2026, and investors are growing impatient with the drag. The structural winner beyond the three dominant players is the advanced packaging ecosystem, where ASE Technology and Amkor are booking record revenues from CoWoS and HBM assembly orders that TSMC cannot absorb alone.

Downstream effects on hyperscalers, capex, and supply chains

The AI chip concentration is forcing hyperscalers (Amazon Web Services, Microsoft Azure, and Google Cloud) to accept higher prices and longer lead times. TSMC's 3nm wafer prices have risen to over $20,000 per wafer, up from $16,000 in 2024, and the company has indicated further increases for 2nm. This directly inflates the cost of Nvidia's B200 and AMD's MI350 accelerators, which in turn raises the capital expenditure required to build AI data centers. Amazon alone is expected to spend over $100 billion on AI infrastructure in 2026, much of it flowing to TSMC and Samsung via Nvidia and AMD. The supply chain is also becoming more concentrated: advanced packaging capacity at TSMC's CoWoS (chip-on-wafer-on-substrate) facilities is fully booked through 2027, with Nvidia and AMD taking over 80% of the output.

For enterprise buyers, the lack of alternative suppliers means they have little pricing power. Microsoft and Google have both signed long-term capacity agreements with TSMC extending into 2029, effectively locking in volumes at current price escalators. The concentration risk extends to geopolitics: if a disruption occurred in Taiwan (whether from a natural disaster or geopolitical tension), the global AI supply chain would halt within weeks, given that TSMC produces over 90% of the world's advanced AI chips. Samsung's Arizona fab and TSMC's own US expansion are partial hedges, but neither facility is expected to produce advanced AI chips at scale before 2028, leaving the world structurally dependent on Taiwan for the foreseeable planning horizon.

What the concentration signals about market and regulatory direction

The extreme concentration of AI chip stocks in Taiwan and South Korea sends a clear signal: these markets are now single-industry plays, and regulators are beginning to take notice. Taiwan's Financial Supervisory Commission has expressed concern about passive index funds being forced to hold outsized TSMC positions, which amplifies volatility. In South Korea, the government is exploring measures to broaden the Kospi's sector representation, including tax incentives for non-tech IPOs and a potential revision of the index weighting methodology. However, these efforts are unlikely to succeed while AI demand continues to grow at 30%–40% annually. The deeper signal is that the AI chip industry is following the same path as the internet boom of the late 1990s: a small number of infrastructure providers capture the vast majority of value, while the broader market becomes a satellite. For investors, this means that country-level diversification in Asia is increasingly an illusion: owning the Taiex or Kospi is effectively owning TSMC or Samsung. The next phase of the cycle will test whether these markets can develop new sources of growth, or whether they remain tethered to the fortunes of three chipmakers.

The concentration will intensify before it eases. TSMC is on track to reach a $2.5 trillion market cap by 2028, and Samsung's memory division is expected to generate record profits as HBM4 enters mass production. Passive fund flows will continue to funnel capital into these stocks, pushing their index weights even higher. The real risk is not a sudden collapse in AI demand (that scenario is remote given hyperscaler commitments), but rather a gradual realization that these markets offer no diversification. A 10% correction in TSMC would wipe out 4% of the Taiex, and a similar move in Samsung would shave 2.5% off the Kospi. For institutional investors benchmarking against Asian equity indices, the only hedge is to underweight the region entirely, which would itself create a self-fulfilling sell-off. The AI chip boom has made Taiwan and South Korea the world's most exciting technology markets, but it has also made them the most fragile.

The concentration of AI chip demand is also reshaping the competitive landscape for smaller players. In Taiwan, companies like MediaTek and UMC are struggling to maintain their market share as TSMC's dominance grows. In South Korea, non-tech sectors such as automotive and chemicals are being starved of capital as investors pile into Samsung and SK Hynix. This dynamic is creating a two-tier market where the largest firms thrive while smaller companies face increasing headwinds. The trend is likely to continue as AI demand remains strong, further entrenching the dominance of TSMC, Samsung, and SK Hynix in their respective markets. For index investors with Asia exposure, the practical implication is stark: diversification at the country level no longer provides the sector breadth it once did.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.