Memory chip makers are entering a supercycle driven by insatiable AI demand, with SK Hynix fielding investment offers from big tech firms for dedicated production pipelines and Micron completing its Taiwan plant acquisition from PSMC in March. The Roundhill Memory ETF surged more than 30% for the week, reflecting investor conviction that the DRAM and NAND boom will deliver windfall gains. AI processors require high-bandwidth memory (HBM), a variant of DRAM, and the supply-demand imbalance is reshaping the competitive landscape across the $160 billion memory industry. Samsung Electronics, which recently joined the trillion-dollar valuation club, is accelerating construction of a new mega-fab by six months, with its P5 Fab 2 expected to start in July. The supercycle will extend beyond 2027, making this a structural shift rather than a cyclical spike. Why this matters now: the memory supercycle is creating a once-in-a-decade capital allocation opportunity, where the winners will be determined not just by who makes the most chips, but by who locks in long-term, customer-funded production capacity.

Customer-funded fabs reshape the merchant model

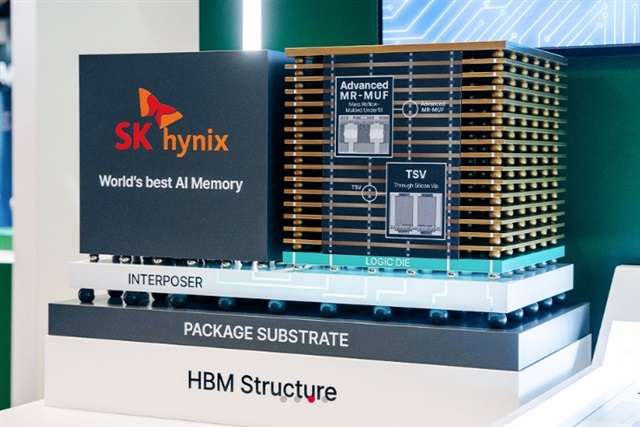

The supercycle is not a vague market narrative. It is a concrete financial phenomenon driven by a structural mismatch between HBM supply and AI accelerator demand. Nvidia, AMD, and other chip designers need HBM3E and next-generation HBM4 memory to feed their GPU clusters, and the memory makers are the sole suppliers. SK Hynix, which dominates the HBM market with an estimated 50% share, is now receiving direct investment offers from big tech firms. These offers are not equity stakes in the company. They are commitments to fund specific production pipelines in exchange for guaranteed allocation. This is a departure from the traditional merchant model, where memory makers build capacity on spec and sell into a spot market. The shift to customer-funded fabs reduces SK Hynix's capital expenditure risk while locking in multi-year revenue streams. Micron's Taiwan plant acquisition from PSMC, completed in March, adds immediate DRAM wafer capacity without the three-year lead time of a greenfield fab. The plant is likely to be converted to produce HBM base dies or advanced DRAM, giving Micron a faster route to capture supercycle pricing. Samsung's decision to pull its P5 Fab 2 construction start forward to July, from an earlier timeline, signals that it will not cede market share. The capital intensity is enormous. A single mega-fab costs $15 billion to $20 billion, but the returns are equally outsized when pricing power is this strong.

Pricing power flows through the P&L

The financial mechanics of the supercycle are straightforward but powerful: supply constraints plus surging demand equals pricing power that flows directly to gross margins and free cash flow. For SK Hynix, operating margins in the HBM segment are estimated to be above 50%, compared to 20%–30% for legacy DRAM. The company's overall profitability is now tied to its ability to shift wafer capacity from commodity DRAM to HBM, a process that requires specialized packaging and through-silicon via (TSV) technology. Micron, which reported record quarterly revenue in its most recent fiscal quarter, is seeing similar margin expansion as its HBM ramp accelerates. The Taiwan plant acquisition gives Micron a low-cost path to add DRAM capacity without the depreciation drag of a new fab. Samsung, despite its trillion-dollar market cap, faces a profitability gap in HBM. It is still qualifying its HBM3E products with Nvidia, and its margin profile lags SK Hynix's by 10 to 15 percentage points. The Roundhill Memory ETF's 30% weekly gain reflects the market's forward-looking assessment: the supercycle is not yet priced in for all players. Free cash flow yields for the memory makers are expected to rise sharply as capital intensity peaks and revenue growth outpaces capex. For investors, the key metric to watch is not revenue growth but the mix shift toward HBM. Each percentage point of HBM share adds disproportionate value to the bottom line. The Roundhill Memory ETF's 30% weekly gain is a rough proxy for the market's forward earnings revision: analysts are repricing the memory sector on the assumption that HBM will constitute more than 40% of SK Hynix's DRAM revenue by end-2026, a level that would sustain the company's margin profile well into 2027 and beyond.

The competitive reshuffle: who gains, who loses

The supercycle is widening the gap between the memory makers that have HBM-ready capacity and those that do not. SK Hynix is the clear leader, with a multi-year head start in HBM3E mass production and a customer-funded capacity model that de-risks its capex. The investment offers from big tech firms, likely including Nvidia and possibly cloud hyperscalers, give SK Hynix a structural advantage: it can build dedicated HBM lines without diluting shareholders or taking on excessive debt. Micron, historically the third player in DRAM behind Samsung and SK Hynix, is using the Taiwan plant acquisition to leapfrog its own capacity constraints. The PSMC plant, located in Taichung, gives Micron a Taiwan foothold that complements its Boise, Idaho, and Hiroshima, Japan, fabs. Samsung, despite its immense financial resources, is playing catch-up in HBM. Its decision to accelerate P5 Fab 2 construction by six months is a defensive move. It needs the capacity to close the HBM gap and defend its DRAM market share. The losers in this reshuffle are the memory makers without HBM capability, such as Chinese DRAM producer CXMT, which lacks access to advanced packaging and TSV technology. The supercycle also pressures NAND flash makers, as AI data centers consume increasing amounts of enterprise SSDs, but the pricing dynamics are less extreme than in DRAM. The competitive outcome will be determined by who can execute the HBM ramp fastest, and SK Hynix has a two-year lead.

Downstream effects on hyperscalers, fabs, and enterprise buyers

The memory supercycle creates second-order effects that ripple through the entire AI supply chain. Hyperscalers, Amazon Web Services, Microsoft Azure, and Google Cloud, are the ultimate consumers of HBM, as it is embedded in the GPU servers that power their AI workloads. The memory shortage is driving these companies to consider direct investments in SK Hynix's production pipelines, a move that mirrors their earlier investments in GPU supply through Nvidia. For the fab equipment industry, the supercycle is a windfall: Applied Materials, ASML, and Tokyo Electron will see orders surge as Samsung, SK Hynix, and Micron ramp HBM-specific capacity. The equipment needed for HBM, including TSV etchers, hybrid bonding tools, and advanced testers, has higher margins than standard DRAM equipment. Enterprise buyers of traditional servers face a different problem: DRAM supply is being diverted to HBM, tightening the market for commodity DDR5 memory and pushing up prices for data center operators that are not building AI clusters. The supercycle also affects the foundry market, as TSMC's CoWoS packaging capacity is a bottleneck for HBM integration. Demand for CoWoS substrates is outpacing supply, with lead times stretching to 12 months for some customers, adding another constraint layer to an already tight AI supply chain. Memory makers are now competing with logic fabs for packaging equipment and substrate supply. The Taiwan plant acquisition by Micron underscores the strategic importance of Taiwan's semiconductor ecosystem. Even as geopolitical risks persist, the island's concentration of DRAM and packaging capacity makes it indispensable for the AI memory supply chain.

What the supercycle signals about market structure

The memory supercycle is not just a pricing event. It is a structural signal that the semiconductor industry is shifting from a commodity model to a partnership model. SK Hynix's willingness to accept customer investment in production pipelines marks a fundamental change: memory is no longer a spot-market product but a strategic input that hyperscalers and AI chip designers must secure through long-term commitments. This mirrors the evolution of the foundry industry, where Apple and Nvidia pre-pay for TSMC capacity. The supercycle also signals that the memory industry's consolidation into three players, Samsung, SK Hynix, and Micron, has created an oligopoly with pricing power that was absent during the boom-bust cycles of the 2000s and 2010s. Samsung's trillion-dollar valuation is a bet that it can maintain its dominance, but the market is already pricing in a premium for SK Hynix's HBM leadership. The policy signal is equally important: governments in South Korea, Taiwan, and the United States are treating memory manufacturing as a national security priority. South Korea's K-Chips Act provides tax credits for HBM investment, while the U.S. CHIPS Act has allocated funding for Micron's domestic fabs. The supercycle validates the thesis that AI demand is not a temporary spike but a permanent shift in computing architecture, and the memory makers that secure customer-funded capacity will be the long-term winners.

The supercycle will extend beyond 2027, but the inflection point will come when HBM supply catches up to demand, likely in late 2027 or early 2028. At that point, pricing power will shift back to buyers, and the memory makers with the lowest cost structure, likely Samsung given its scale, will regain the advantage. SK Hynix's customer-funded model creates a buffer: even if HBM prices normalize, its revenue is partially locked in through multi-year agreements. Micron's Taiwan plant gives it a cost advantage over greenfield fabs, but it must prove it can match SK Hynix's HBM yield and performance. The wild card is Samsung: if it can close the HBM gap within 12 months, its trillion-dollar balance sheet will allow it to outspend both rivals and reclaim share across the entire DRAM spectrum. The Roundhill Memory ETF's 30% weekly gain may be just the beginning, but investors should watch for the moment when hyperscalers stop committing capital to dedicated HBM production lines. That decisive signal will mark the inflection point of the supercycle. For now, the memory makers hold the leverage, and the AI industry is paying the premium that comes with structural scarcity.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.