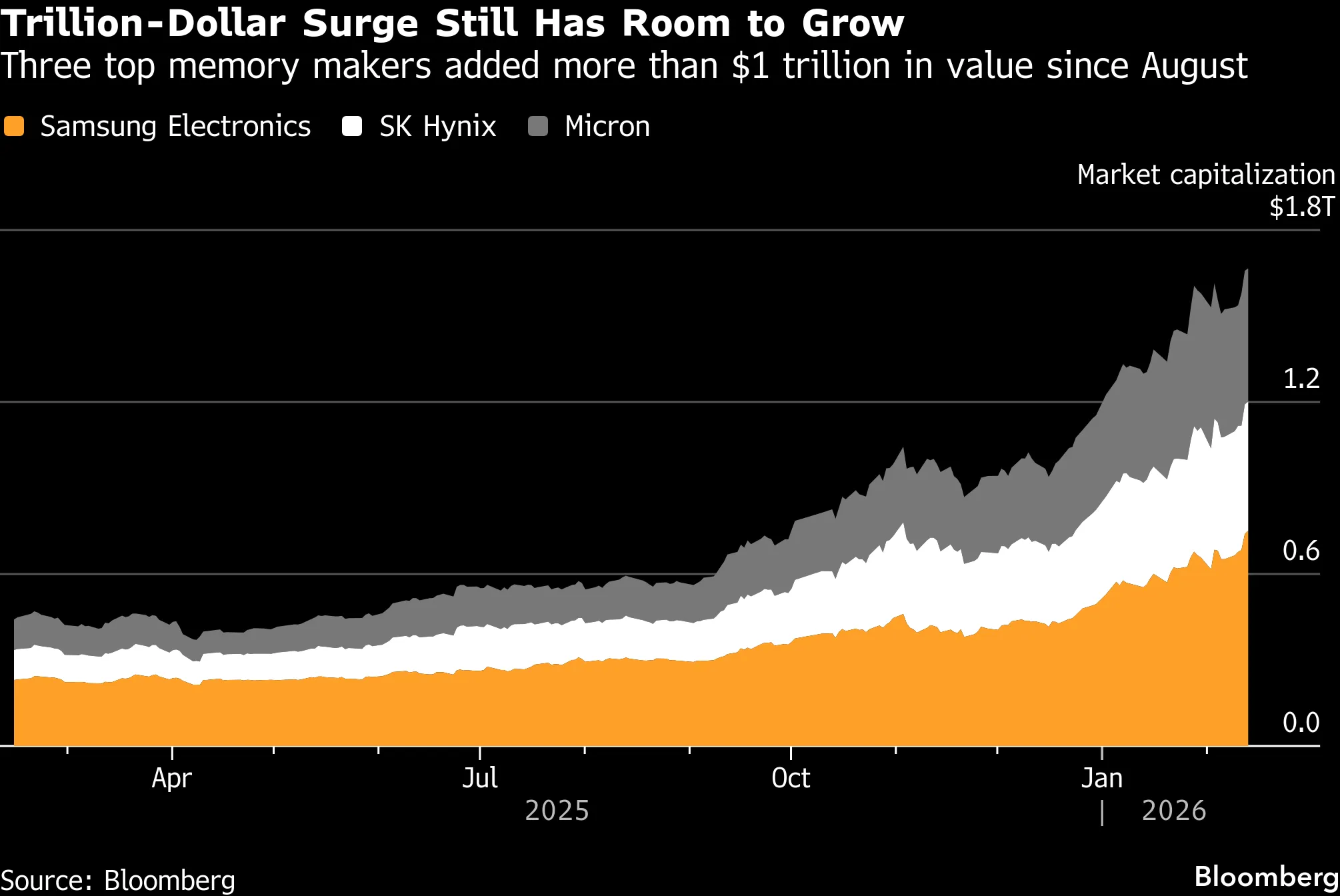

Memory chip makers are experiencing a historic "supercycle" as artificial intelligence demand drives an unprecedented surge for high-bandwidth memory. The Roundhill Memory ETF gained more than 30% in a single week, reflecting investor conviction that the three dominant players (SK Hynix, Micron, and Samsung Electronics) are positioned for windfall gains. AI processors require high-bandwidth memory solutions like DRAM and NAND, and the current supply-demand imbalance is pushing these chipmakers into territory previously reserved for hyperscaler platforms. SK Hynix is now fielding offers from big tech firms to invest directly in specific production pipelines to accelerate memory chip output. Micron recently completed the acquisition of a plant in Taiwan from Powerchip Semiconductor Manufacturing Corporation (PSMC), giving it additional flexibility for future DRAM and HBM nodes. Samsung Electronics, which recently joined the trillion-dollar valuation club, is advancing construction of a new mega-fab by six months, with P5 Fab 2 at its Pyeongtaek campus expected to break ground in July. This is not a cyclical uptick; it is a structural shift in how the semiconductor industry allocates capital, and the supercycle will extend beyond 2027. The investment community has taken notice: semiconductor analysts are revising price targets upward, and institutional money is rotating into memory names at a pace not seen since the last major upcycle. The implications extend beyond quarterly earnings, touching on national industrial policy, AI infrastructure investment, and the future architecture of data center hardware.

The 30% ETF Surge Reflects a Fundamental Repricing

The Roundhill Memory ETF's 30% weekly gain is not a speculative fluke; it reflects a fundamental repricing of memory chip earnings power. The ETF aggregates exposure to SK Hynix, Micron, and Samsung Electronics, all of which have seen their forward multiples expand as AI-driven demand for high-bandwidth memory tightens supply. The surge began after multiple big tech firms approached SK Hynix with offers to co-invest in dedicated production lines, a move that signals long-term demand visibility rather than spot-market volatility. These offers effectively de-risk capital expenditure for SK Hynix, allowing it to ramp capacity without absorbing the full financial burden. Micron's Taiwan plant acquisition from PSMC adds further supply-side credibility, giving the company a ready-made facility to convert into DRAM and HBM production nodes. The ETF's performance also reflects Samsung's trillion-dollar valuation milestone, which embeds expectations that its mega-fab expansion will capture a larger share of the AI memory market. Investors are pricing in a multi-year supercycle, not a quarterly spike. The 30% move compresses months of anticipated earnings upgrades into a single week, and the underlying fundamentals, notably direct customer investments, plant acquisitions, and accelerated construction timelines, all of which support the re-rating.

How the Money Flows Through P&L and Valuation

The financial mechanics of this supercycle are straightforward but powerful. SK Hynix, Micron, and Samsung are all seeing average selling prices for HBM rise as AI chipmakers bid up supply. The direct investment offers that SK Hynix is receiving from big tech firms effectively convert customer demand into pre-funded capital expenditure, improving free cash flow profiles. For Micron, the PSMC plant acquisition in Taiwan provides a lower-cost path to expand DRAM and HBM capacity compared to greenfield construction, which typically takes 18-24 months. The acquisition shortens the time to revenue and reduces the capital intensity per wafer. Samsung's decision to accelerate P5 Fab 2 construction by six months means it will bring new capacity online sooner, capturing higher prices before the market potentially normalizes. The valuation impact is already visible: Samsung's trillion-dollar market capitalization embeds a forward price-to-earnings multiple that reflects sustained HBM margins. For the Roundhill Memory ETF, the 30% weekly gain translates into a re-rating of the entire memory sector, with analysts now projecting that the supercycle will extend beyond 2027. The cash flow generation from HBM sales is also enabling these companies to self-fund further expansions, creating a virtuous cycle where rising profits finance even more capacity.

The Competitive Reshuffle Among SK Hynix, Micron, and Samsung

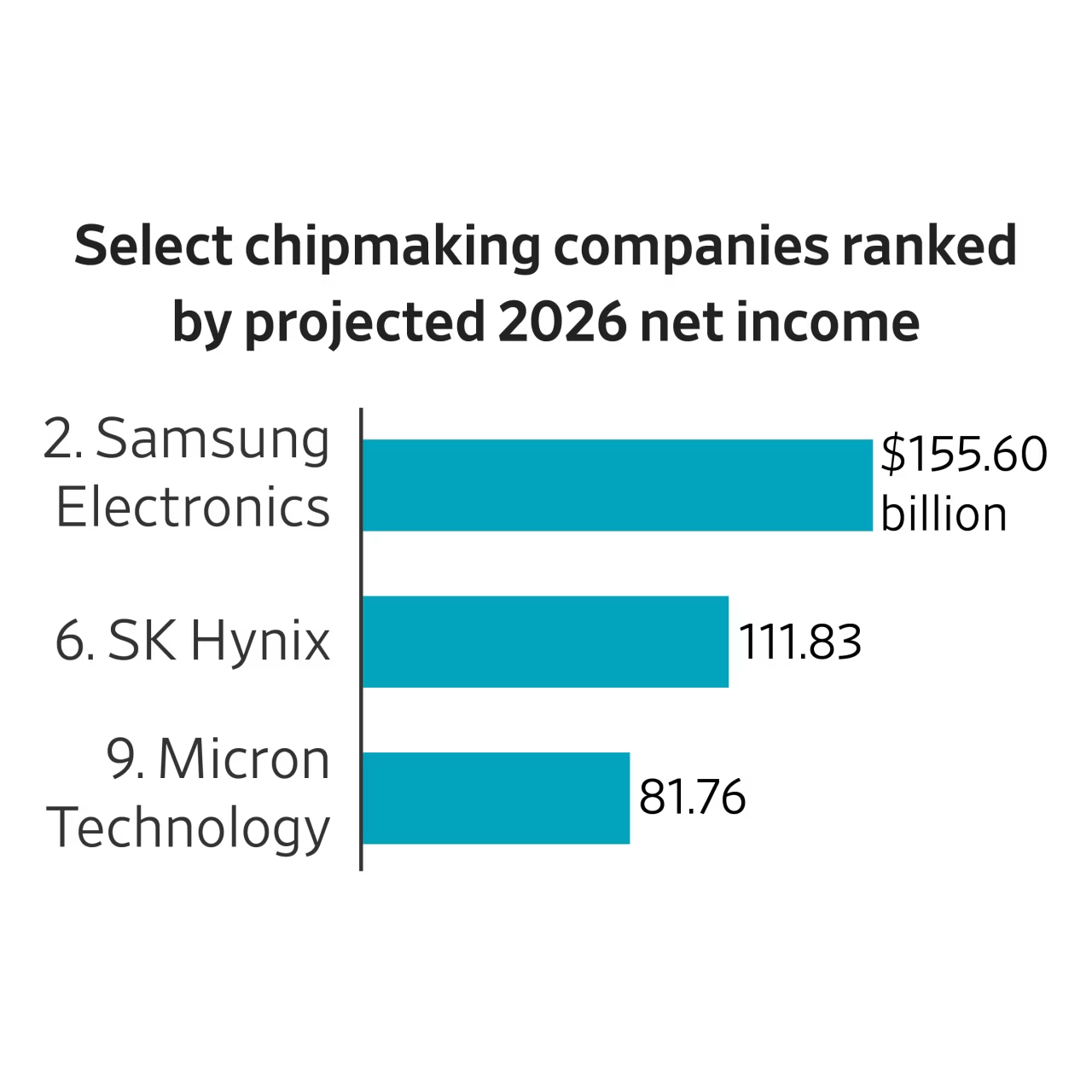

The AI memory supercycle is reshaping the competitive dynamics among the three major players. SK Hynix currently holds the lead in HBM technology and is the primary supplier to Nvidia, giving it pricing power and customer relationships that translate into direct investment offers from big tech. This co-investment model creates a competitive moat; customers who fund production lines are unlikely to switch suppliers mid-cycle. Micron's acquisition of the PSMC plant in Taiwan is a direct response to SK Hynix's lead, providing a faster path to scale DRAM and HBM production without building from scratch. The plant gives Micron geographic diversification and additional capacity for future nodes, narrowing the gap with SK Hynix. Samsung Electronics is playing catch-up but has the deepest pockets and the broadest product portfolio. Its trillion-dollar valuation and accelerated P5 Fab 2 construction signal that it intends to close the HBM technology gap within two to three years. Samsung's advantage lies in its ability to cross-subsidize memory investments with profits from its foundry and logic businesses. The competitive outcome will depend on execution speed: SK Hynix has the technology lead, Micron has the acquisition-driven capacity boost, and Samsung has the financial firepower. The Roundhill Memory ETF's 30% gain reflects the market's view that all three will benefit, but the relative winners will be determined by who can deliver HBM volume fastest.

Downstream Effects on Hyperscalers, Fabs, and Enterprise Buyers

The memory supercycle is creating second-order effects across the AI supply chain. Hyperscalers like Microsoft, Amazon, and Google are the ultimate consumers of HBM-equipped AI processors, and their willingness to co-invest with SK Hynix indicates that memory supply has become a bottleneck for AI infrastructure deployment. This dynamic gives memory makers unusual leverage in pricing negotiations, as hyperscalers cannot afford to wait for additional capacity. For fab equipment suppliers, the accelerated construction of Samsung's P5 Fab 2 and the conversion of Micron's Taiwan plant mean increased orders for deposition, etching, and test equipment. The capex cycle for memory is now decoupled from the broader semiconductor cycle, driven by AI-specific demand rather than consumer electronics. Enterprise buyers of AI servers are facing longer lead times and higher costs as memory components become constrained. The supercycle also affects the NAND market, as AI data centers require high-density storage for training datasets. NAND pricing has historically been more volatile than DRAM, but AI-driven demand for large-scale storage is providing a new demand floor. The combination of rising NAND and DRAM prices is compressing margins for AI server integrators, who must absorb higher bill-of-materials costs or pass them along to enterprise cloud customers. Powerchip Semiconductor Manufacturing Corporation, which sold the Taiwan plant to Micron, is now freed to focus on its specialty foundry business, potentially easing supply in other segments. The Roundhill Memory ETF's 30% surge is therefore not just a memory story; it is a signal that the entire AI infrastructure buildout faces a memory bottleneck that will persist through 2027.

Market and Policy Signals from the Supercycle

The memory supercycle is a clear statement about where the semiconductor market is heading. The willingness of big tech firms to invest directly in SK Hynix's production lines represents a structural shift in how the industry finances capacity — moving from speculative buildouts to demand-backed commitments. This model reduces the risk of overcapacity that has historically plagued memory makers and enables more aggressive expansion. Samsung's trillion-dollar valuation and accelerated mega-fab construction signal that the company views AI memory demand as durable enough to justify front-loading billions in capex. For regulators, the concentration of HBM supply among three Korean and American companies raises questions about supply chain resilience, particularly given geopolitical tensions with China. The supercycle also pressures governments to accelerate semiconductor subsidy programs, as memory capacity becomes a strategic asset. The fact that the supercycle will extend beyond 2027 suggests that AI adoption is still in its early stages, and memory demand will grow as AI moves from training to inference at scale. Inference workloads require persistent memory bandwidth to serve billions of queries in real time, creating a demand floor that is fundamentally different from the batch-processing patterns of earlier AI deployments. Governments in South Korea, Japan, and the United States are all monitoring HBM supply chains closely, with potential subsidy programs aimed at securing domestic memory capacity for strategic AI initiatives. The Roundhill Memory ETF's 30% weekly gain is the market's way of pricing in this multi-year visibility. Investors should watch for further co-investment announcements from SK Hynix, capacity conversion updates from Micron, and construction milestones from Samsung as leading indicators of whether the supercycle accelerates or plateaus.

The memory supercycle is rewriting the rules of semiconductor finance, with big tech firms now acting as de facto equity partners in production capacity. SK Hynix's co-investment offers, Micron's plant acquisition, and Samsung's accelerated fab construction all point to a market where demand visibility is high enough to justify unprecedented capital commitments. The Roundhill Memory ETF's 30% surge is the opening act, not the finale. As AI workloads scale from training clusters to inference at the edge, the demand for high-bandwidth memory will only intensify. The supercycle extending beyond 2027 means that the current capacity additions will be absorbed, and further expansions will be needed. The key risk is execution; if any of the three players fails to ramp production on schedule, the supply crunch will worsen, driving memory prices even higher. For investors, the supercycle offers a rare combination of volume growth and pricing power, but the window to capture these gains at current valuations is narrowing. The next 12 months will determine whether this is a sustainable structural shift or a peak that fades as new capacity comes online. Tracking capacity utilization rates across SK Hynix, Micron, and Samsung each quarter will be the clearest signal of whether the supercycle holds.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.