Wall Street’s two most influential rate forecasters have thrown in the towel on near-term easing. Goldman Sachs and Bank of America now expect the Federal Reserve to hold its federal funds rate at 3.50%-3.75% until at least late 2026, with BofA pushing its first projected cut all the way to July 2027. The catalyst was the April 29 FOMC meeting, where the vote split 8-4, the widest dissent margin since 1992. Four regional bank presidents voted against the hold, with some arguing for a rate hike. The doves, led by Chicago Fed President Austan Goolsbee, have not ruled out tightening either. Inflation is the culprit: headline PCE hit 3.5% in March, up from 2.8% in February, while core PCE rose to 3.2% from 2.9%. Energy costs from the Iran war are passing through to core goods and services, keeping core PCE near 3% through 2026, according to Goldman. Meanwhile, the April jobs report showed 115,000 nonfarm payrolls and unemployment at 4.3%, giving the Fed cover to hold. The CME FedWatch tool now places a 93.4% probability on no change at the June 17 meeting. For markets, the message is clear: the era of cheap money is not returning anytime soon, and risk assets from Bitcoin to growth stocks will feel the liquidity squeeze.

The 8-4 Vote Reshapes the Fed's Reaction Function

The April FOMC decision was not just a hold. It was a signal of institutional fracture. The 8-4 vote is the closest since 1992, a year when the Fed was navigating the aftermath of the savings and loan crisis. Four dissenting voters wanted a rate hike, not a hold. That is a hawkish tilt that goes beyond the usual dove-hawk spectrum. It tells markets that the median FOMC member is now closer to tightening than easing, even if the headline decision was to stand pat. Aditya Bhave, BofA’s senior U.S. economist, put it bluntly: "The data simply don’t warrant cuts this year." The dissenters’ argument rests on the March PCE prints: headline 3.5% and core 3.2% are both well above the Fed’s 2% target, and the trajectory is worsening. Energy pass-through from the Iran conflict is adding 0.2-0.3 percentage points to core inflation each quarter, according to Goldman’s models. The labor market adds another layer: 115,000 April payrolls and 4.3% unemployment are consistent with a job market that is not softening enough to justify easing. Goolsbee, a noted dove, acknowledged that a rate hike is possible if inflation does not moderate. The 8-4 vote effectively raises the bar for any cut: the Fed now needs not just one good inflation print but a sustained series of disinflationary data to overcome the internal hawkish pressure. The dissent margin itself functions as a forward guidance tool, signaling to markets that any future easing will require a decisive shift in the data.

How $570 Billion in Rate-Sensitive Cash Gets Trapped

The delayed cuts directly impact the flow of capital through the financial system. At 3.50%-3.75%, the fed funds rate is high enough to keep money market funds and short-term Treasury bills attractive relative to risk assets. The total U.S. money market fund assets stand at roughly $5.7 trillion, according to the Investment Company Institute. A hold through 2026 means those funds will continue to earn 3.5%+ yields with zero duration risk, reducing the incentive to rotate into equities, credit, or crypto. Goldman’s revised forecast of cuts in December 2026 and March 2027 implies the first easing is 19 months away. BofA’s July 2027 call pushes that to 26 months. For every month the Fed holds, an estimated $15 billion to $20 billion in incremental cash stays in money markets rather than flowing into risk assets, based on historical flow patterns. The opportunity cost for growth companies is substantial: a 26-month delay in cuts means roughly 200 basis points of additional discount rate applied to future cash flows, compressing valuation multiples for unprofitable tech and biotech names. The IMF has flagged that prolonged high rates increase the risk of corporate defaults, particularly among leveraged borrowers who refinanced at low rates in 2020-2021 and now face maturities in 2027-2028.

The sector breakdown reveals where the pain is most concentrated. High-yield issuers carrying floating-rate debt face quarterly interest resets that now track a 3.50%-3.75% benchmark, squeezing margins in sectors like commercial real estate, mid-tier retail, and leveraged buyouts from the 2021-2022 vintage. For private credit funds, the higher carry is attractive in the short term, but deal flow is thinning as sponsors delay exits waiting for a more favorable rate environment. BofA’s Bhave warned that the adjustment from a previously forecast September 2026 cut to July 2027 represents one of the most aggressive consensus shifts since the 2022 tightening cycle began, and the re-rating across leveraged loan indices has been swift.

Goldman and BofA Force a Competitive Repricing Across Wall Street

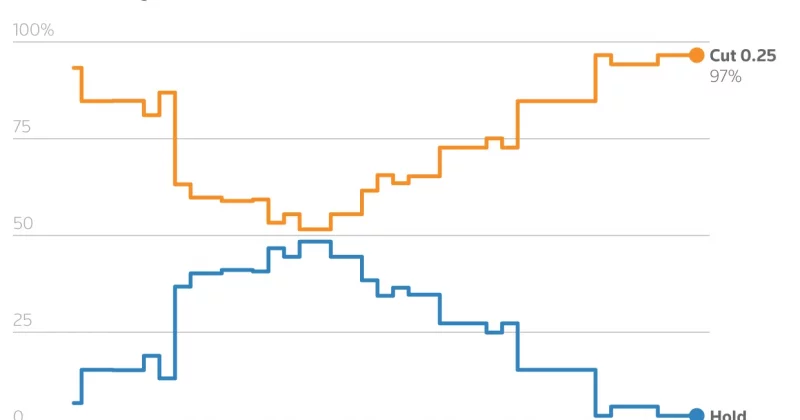

Goldman and BofA are not just forecasting. They are setting the consensus. When the two largest U.S. investment banks by trading revenue both push rate cuts to 2026-2027, it forces every other sell-side desk to reprice their models. Morgan Stanley and JPMorgan had been forecasting cuts in early 2026; both will likely revise in the coming weeks. The divergence matters because rate expectations drive everything from mortgage-backed securities pricing to leveraged loan underwriting. Goldman’s call is based on core PCE staying near 3% through 2026, driven by energy pass-through. BofA’s call is even more hawkish, citing the labor market’s resilience. The CME FedWatch tool, which aggregates fed funds futures pricing, now shows a 93.4% probability of a hold at the June 17 meeting. That is up from 78% before the April jobs report. The repricing is already visible in the Treasury market: the 2-year yield rose 12 basis points on the day of the BofA note, and the 10-year yield climbed 8 basis points. For active managers, the window for duration positioning has narrowed. Hedge funds that had been shorting the front end of the curve are now covering, while those betting on a steepener are being rewarded. The competitive dynamic is also playing out in FX: the dollar index strengthened 0.6% on the week as rate differentials favor the U.S. over the eurozone and Japan.

Downstream Effects on Crypto, Housing, and Corporate Capex

The delayed cuts create a cascade of second-order effects. For crypto, the liquidity squeeze is acute. Bitcoin and Ethereum have historically rallied on expectations of Fed easing; a 19-26 month delay removes that catalyst. Bitcoin is down 14% since the April FOMC meeting, and Ethereum has fallen 18%. The CME FedWatch data shows that risk assets are now pricing in a higher probability of a recession than a cut. For housing, the 30-year fixed mortgage rate has remained above 6.5% despite the Fed’s hold, as the spread between mortgage rates and Treasuries stays elevated due to prepayment risk and bank balance sheet constraints. The National Association of Realtors reported existing home sales at a 4.1 million annualized pace in April, down 8% year-over-year. For corporate capex, the cost of capital remains high. Investment-grade bond yields are at 5.2%, up from 4.8% in January. Companies like Intel and TSMC, which are building new fabs, now face a higher discount rate on their long-term capital expenditures. The Chicago Fed’s National Activity Index, which tracks economic growth, has been trending below zero for three consecutive months, signaling that the economy is growing below trend. If that persists, the Fed’s hold becomes a tightening in real terms, as the neutral rate, estimated at 2.5% to 3.0% by the Fed’s own staff, is now below the policy rate.

The Policy Signal: A Fed That Will Not Cut Until It Sees White Smoke

The April 8-4 vote is a policy statement in itself. It tells markets that the Fed is willing to tolerate a period of below-trend growth and financial market stress to bring inflation down. The four dissents for a hike are a warning that the next move could be up, not down. Goolsbee’s comment that a rate hike is possible reinforces that message. The Fed is effectively saying that the 2% target is non-negotiable, even if it takes until 2027. That is a shift from the 2023-2024 narrative, when markets assumed the Fed would cut at the first sign of economic weakness. Now, the labor market is the key variable: as long as payrolls stay above 100,000 and unemployment remains below 4.5%, the Fed has cover to hold. The Iran war energy shock adds a layer of complexity: the Fed cannot cut into rising energy prices without risking a wage-price spiral. The IMF has warned that central banks should not ease prematurely in the face of supply-driven inflation. The Fed is listening. For investors, the implication is that the risk-free rate will stay elevated for longer, compressing equity risk premiums and forcing a rotation into value, dividends, and short-duration bonds. The era of "lower for longer" is over; "higher for longer" is the new regime.

The next major test comes at the June 17 FOMC meeting, where the dot plot will be updated. If the median dot shifts to one cut in 2026 or none at all, the market will have to fully absorb the 2027 timeline. That would likely trigger another leg higher in real yields and a further sell-off in growth stocks and crypto. The wildcard is the labor market: if payrolls slip below 100,000 for two consecutive months, the Fed could be forced to cut sooner, but that would require a recessionary scenario that the current data does not support. For now, the path of least resistance is higher rates for longer, and the smart money is positioning accordingly. The consensus has shifted decisively, and with Goldman and BofA both anchoring the market's rate expectations in late 2026 at the earliest, any surprise dovish pivot would require a combination of disinflationary shocks that no forecaster is currently modeling. Investors who have been waiting for a rate-cut rally will need to recalibrate their timelines.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.