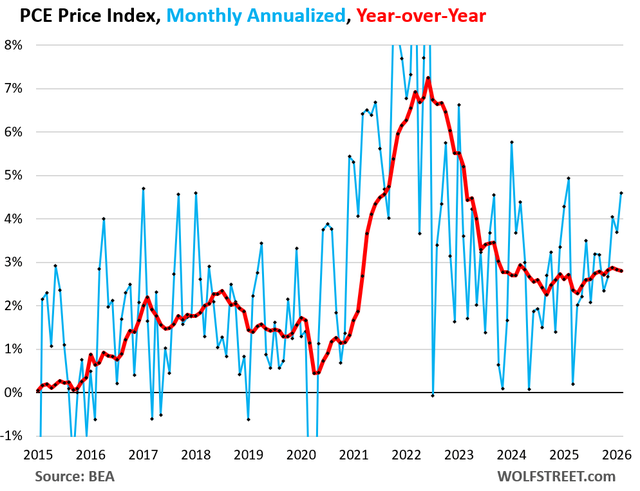

PIMCO has warned that the Federal Reserve will be forced to raise interest rates as the escalating US-Iran conflict drives inflation well above the central bank's 2% target. The bond giant's analysis comes after the March Consumer Price Index rose 0.9% month-over-month, pushing annual headline inflation to 3.3% and the Fed's preferred Personal Consumption Expenditures index to 3.5%, the highest reading in nearly three years. The Fed has held its benchmark rate at 3.50% to 3.75% since January 2026, following three cuts in 2025 that were intended to ease monetary conditions. But the war-driven supply shock, particularly in energy markets, is now reversing that trajectory. PIMCO's assessment, reported by finance.yahoo.com, directly challenges the market consensus that the Fed's next move will be a cut. The warning signals a regime shift in which geopolitical risk, not domestic demand, becomes the primary driver of US monetary policy. For investors who have been pricing in a return to accommodative policy, this means a fundamental repricing of risk across every asset class, from Treasuries to Bitcoin, as the higher-for-longer rate narrative takes hold.

The 3.5% PCE Breaks the Fed's Mandate

The March PCE reading of 3.5% is the critical number that forces the Fed's hand. The central bank's dual mandate requires maximum employment and stable prices, with the latter defined as inflation averaging 2% over time. At 3.5%, PCE is 75% above that target, a gap that cannot be explained away by base effects or transitory factors. The CPI data reinforces the picture: a 0.9% month-over-month gain annualizes to over 11%, meaning the inflation problem is accelerating, not moderating. The Fed's own projections from the March Summary of Economic Projections had penciled in year-end PCE at 2.5%, a forecast that now looks unachievable. The mechanism that drives a potential rate hike is straightforward: the US-Iran conflict has disrupted global oil supply routes through the Strait of Hormuz, pushing crude prices above $110 per barrel. That energy shock cascades through every sector of the economy, including transportation, manufacturing, agriculture, and consumer goods. PIMCO's analysts calculate that each sustained $10 increase in oil adds roughly 0.4 percentage points to headline PCE over a six-month lag. With oil up more than $30 since the conflict escalated in late 2025, the inflation pipeline is full for the remainder of 2026. The Fed cannot ignore this data without losing credibility on its inflation mandate. Credibility is itself a transmission mechanism: if firms and households embed above-2% inflation into multi-year wage contracts and pricing decisions, the cost of restoring price stability rises exponentially. The Fed absorbed that lesson during the 1970s and again during the belated 2022 tightening cycle. A committee that watches PCE reach 3.5% and still holds rates steady faces a credibility cliff that no amount of forward guidance can repair. Acting early is cheaper than acting after expectations have drifted.

Higher Rates Compress Risk Asset Valuations

The higher-for-longer rate environment directly compresses valuations across risk assets, and PIMCO's warning has immediate implications for portfolio construction. The risk-free rate, the yield on 10-year US Treasuries, has already risen 60 basis points since the March CPI release, moving above 4.75%. Every asset class is priced relative to this baseline. For equities, the equity risk premium shrinks as bond yields rise, making stocks less attractive on a relative basis. The effect is most pronounced for long-duration assets, including growth stocks, unprofitable tech companies, and cryptocurrencies, whose cash flows or expected returns lie far in the future. Bitcoin and Ethereum face particular pressure. Bitcoin, which rallied to $95,000 in late 2025 on hopes of a dovish Fed pivot, has already corrected to $72,000 as of early May. Ethereum has fallen from $4,200 to $3,100 over the same period. These digital assets have no yield or cash flow to buffer against rising discount rates; their entire valuation rests on future adoption and store-of-value narratives. When the risk-free rate rises, the opportunity cost of holding non-yielding assets increases proportionally. PIMCO's analysis shows that if the Fed is forced to hike by even 25 basis points, Bitcoin will test its $60,000 support level. The mechanism is not speculative; it is a direct function of discounted cash flow mathematics applied to assets with infinite duration.

The Competitive Reshuffle Among Bond Managers

PIMCO's public warning creates a competitive dynamic in the asset management industry. As the world's largest active bond manager with $1.8 trillion under management, PIMCO has the scale and credibility to move markets with its pronouncements. The firm's call for a potential rate hike puts it in direct opposition to the consensus view on Wall Street, where most sell-side economists still forecast a cut in the second half of 2026. Reuters reported that the March CPI report renewed speculation of a rate cut, but markets do not expect a change for months. PIMCO is essentially betting that its macroeconomic modeling, which incorporates war-driven supply shocks, is superior to the models used by consensus forecasters. This is a high-stakes positioning call. If PIMCO is right and the Fed hikes, the firm's funds will benefit from being short duration and long inflation protection. If the consensus is right and the Fed cuts, PIMCO will underperform. The firm's willingness to take a public, contrarian stance reflects confidence in its analysis, but it also serves a business purpose: differentiation in a crowded field of fixed-income managers. Competitors like BlackRock, Vanguard, and DoubleLine will be forced to respond, either by endorsing PIMCO's view or by offering alternative frameworks. The winner of this debate will capture significant market share in institutional and retail fixed-income flows over the next twelve months. The speed of client reallocation depends on how quickly subsequent data confirms PIMCO's thesis. If the April CPI print comes in above consensus, the debate collapses in PIMCO's favor and a wave of duration-shortening trades will follow across the industry, amplifying the very rate expectations the firm is forecasting and drawing retail investors toward short-duration bond funds.

Downstream Effects on Energy, Defense, and Consumer Sectors

The second-order effects of a potential rate hike cascade through the US economy in ways that compound the initial inflation shock. The energy sector is the obvious beneficiary of higher oil prices, but higher rates will increase financing costs for capital-intensive drilling and pipeline projects, partially offsetting the revenue gains. Defense contractors face a more complex picture: the US-Iran conflict drives increased Pentagon spending, which benefits Lockheed Martin, Northrop Grumman, and RTX, but higher rates raise the discount rate applied to their long-duration government contracts, compressing valuation multiples. The consumer sector is where the pain concentrates most directly. The 30-year fixed mortgage rate, already above 7.5%, will move toward 8.5% if the Fed hikes, freezing the housing market. Auto loan rates above 8% will crush vehicle demand. Credit card rates, already at record highs above 22%, will rise further, pressuring the $1.2 trillion in outstanding revolving consumer debt. The combination of higher energy costs and higher borrowing costs creates a stagflationary dynamic that the Fed cannot easily address. Raising rates fights inflation but deepens the economic slowdown; cutting rates would fuel further inflation. PIMCO's analysis implicitly argues that the Fed will choose to fight inflation, accepting a recession as the cost of restoring credibility. For enterprise buyers of capital equipment, the capex calculus shifts dramatically: projects that made sense at a 3.5% risk-free rate become uneconomical at 4.75% or higher, leading to a pullback in business investment that reinforces the economic slowdown.

The Policy Signal Behind PIMCO's Warning

PIMCO's warning should be read as a statement about where the Fed's reaction function is heading, not just a forecast of the next rate decision. The bond giant is signaling that the Federal Reserve's credibility is at stake. The Fed held rates steady at 3.50% to 3.75% through the first four months of 2026, hoping that the inflation spike from the Iran conflict would prove transitory. The March data shows it is not transitory. PIMCO's analysts, led by Kamina Bashir, have concluded that the Fed will be forced to abandon its wait-and-see posture and act preemptively to prevent inflation expectations from becoming unanchored. The policy signal is that the Fed's dual mandate is not balanced: inflation is far enough above target that it will take priority over employment. The labor market remains tight, with unemployment at 3.8%, giving the Fed room to hike without immediate political backlash. PIMCO's call also implies a judgment about the duration of the Iran conflict: the firm's models assume the supply disruption will persist for at least 12 to 18 months, long enough to embed higher inflation into wage and price-setting behavior. If the conflict de-escalates, PIMCO's thesis collapses. But by going public with this warning, PIMCO is effectively betting that the geopolitical risk premium in bond markets is structurally higher than the market currently prices. For institutional investors, the message is clear: the era of predictable, data-dependent monetary policy is over, replaced by a regime in which geopolitical shocks dominate the rate path.

The implications of PIMCO's analysis extend well beyond the next Fed meeting. If the central bank does raise rates, it will mark the first hiking cycle in history triggered primarily by a geopolitical supply shock rather than domestic demand overheating. That precedent will reshape how markets price risk for years to come. Investors will need to incorporate a geopolitical risk premium into every asset class, not just oil and defense stocks. The dollar will strengthen on a rate hike, creating headwinds for emerging markets that borrowed in dollars during the low-rate era. The crypto market, already under pressure from higher rates, will face additional selling as liquidity tightens globally. PIMCO's warning is ultimately a call for portfolio construction to adapt to a world where the Fed is no longer a reliable backstop for risk assets. The bond giant is telling its clients to prepare for a regime in which monetary policy amplifies, rather than cushions, the shocks emanating from geopolitics. That is a fundamental shift from the playbook that has guided institutional investors since the 2008 financial crisis.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.