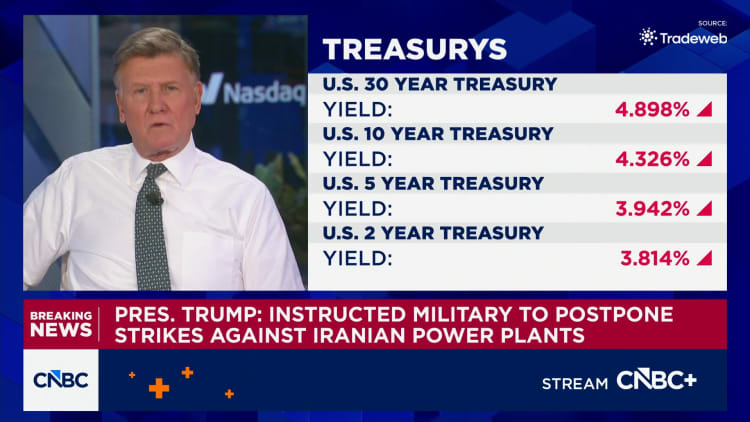

Pimco, one of the world's largest bond managers, has issued a stark warning that a military conflict with Iran could force the Federal Reserve to raise interest rates, a scenario most investors still consider unthinkable. The asset manager's call stands in sharp contrast to the prevailing market consensus: futures markets show investors betting against any rate hikes, and the Fed's own Richard Fisher has expressed comfort with current policy. Yet the bond market is already sending a contradictory signal. Since mid-2024, the Fed has cut its benchmark rate by 175 basis points, but the 10-year Treasury yield has barely dipped, only about 35 basis points, while the 30-year yield has touched 5%. That disconnect, combined with the U.S. government's need to issue far more debt than expected after the Supreme Court struck down Trump's tariffs and the One Big Beautiful Bill Act created new tax breaks, means the bond market is effectively shouting at the Fed. The question now is whether the central bank can hold its course, or whether geopolitical and fiscal pressures will force it into a tightening cycle that would upend everything from mortgage rates to corporate borrowing costs.

Where the $570M Debt Surge Comes From

The U.S. government must issue significantly more debt than previously anticipated as cash flow weakens under the weight of new fiscal obligations. The Supreme Court's decision to strike down Trump's tariffs triggered refunds that total up to $166 billion, while the One Big Beautiful Bill Act introduced new tax breaks that further depress federal revenue. These twin shocks have blown a hole in the Treasury's near-term financing plan. The result is a larger-than-expected auction calendar for Treasury bills and longer-dated bonds, just as the Fed is shrinking its balance sheet through quantitative tightening. This supply-demand imbalance is the mechanical reason long-term yields are rising even as the Fed cuts short-term rates. The 30-year yield touching 5% is not a reflection of strong economic growth; it is a risk premium demanded by investors who see a growing supply of government paper with no obvious buyer of last resort. The Treasury must now compete for capital in a market where foreign central banks are reducing their U.S. debt holdings and domestic banks are already stuffed with reserves. Every additional dollar of issuance pushes yields higher, creating a feedback loop that makes the government's own borrowing more expensive. The Treasury's borrowing needs have jumped by an estimated $570 billion relative to earlier projections, forcing the department to schedule larger auctions across the maturity spectrum. This wave of new supply hits a market already absorbing the Fed's quantitative tightening, where the central bank is letting bonds roll off its balance sheet rather than reinvesting proceeds.

How the 175bps Cut Failed to Bend the Curve

The Fed's 175 basis points of rate cuts since mid-2024 should have pulled down borrowing costs across the curve, but the 10-year yield has only dipped about 35 basis points. That is a stunning failure of monetary transmission. Normally, when the Fed cuts the federal funds rate, short-term yields fall and long-term yields follow, albeit with a lag. This time, the long end has refused to cooperate. The 30-year yield touching 5% is a clear signal that bond investors are pricing in higher inflation, larger fiscal deficits, or both. For corporate treasurers and CFOs, this means the cost of issuing 10-year or 30-year debt has barely budged despite the most aggressive easing cycle since 2020. The yield curve has steepened dramatically, compressing the profitability of banks that borrow short and lend long. Siebert Financial's Mark Malek has noted that the bond market is "shouting" at policymakers, and the message is unambiguous: the market does not believe the Fed's cuts are sustainable. If Pimco's Iran scenario materializes, the Fed would face the worst of both worlds: a spike in energy prices and supply-chain disruption that forces it to raise rates into a slowing economy, crushing the very borrowers the cuts were meant to help. The 30-year yield's breach of 5% represents a full percentage point above the 10-year yield, a steepness last seen during the taper tantrum of 2013. That steepness penalizes banks that fund long-term mortgages with short-term deposits, squeezing net interest margins across the regional banking sector.

Pimco vs. the Consensus: Who Wins the Bet

Pimco's warning that an Iran war could force a rate hike puts it squarely against the majority of Fed watchers and the futures market, which still shows investors betting against any rate rises. The asset manager is essentially making a tail-risk call that most of the market has dismissed as too remote to hedge. But Pimco has form on these macro calls; its size and trading clout mean its positioning can move markets when it decides to act. The divergence between Pimco's view and the consensus creates a classic opportunity for volatility arbitrage. If the geopolitical situation deteriorates, the entire rate expectations curve would reprice violently, with short-term rates jumping and long-term rates following as inflation expectations reset higher. The winners would be those who bought protection against a rate hike through options on fed funds futures or short positions in Treasury bonds. The losers would be the leveraged players who have piled into carry trades funded at short-term rates, betting the Fed would keep cutting. For now, the market is giving Pimco's scenario a low probability, but the bond market's own pricing, with the 30-year at 5%, shows investors already demanding compensation for a risk they refuse to name explicitly. Pimco's track record on tail-risk calls includes its early warning on the 2020 pandemic dislocations and its correct bet against the 2022 "transitory inflation" narrative, giving its current warning extra weight among institutional allocators.

The Hyperscaler and Housing Market Fallout

A Fed rate hike driven by an Iran conflict would cascade through every asset class, but two sectors would feel it most acutely: hyperscale data-center builders and the housing market. The hyperscalers, Amazon, Microsoft, Google, Meta, have committed hundreds of billions of dollars to AI infrastructure, much of it financed with long-term debt. A 100-basis-point spike in the 10-year yield would add roughly $10 billion in annual interest costs across the four companies, forcing them to either slow capex or accept lower margins. The housing market, already struggling with affordability, would see mortgage rates surge past 8%, freezing transaction volumes and crushing homebuilder stocks. The regional banks that hold most of the mortgage servicing rights would face another wave of hedging losses. Meanwhile, the Treasury's need to issue more debt would crowd out private-sector borrowing, raising the cost of capital for every corporate borrower. The Fed would be caught between fighting inflation from energy prices and avoiding a financial accident in the bond market. Pimco's warning is not just about rates; it is about the real economy's vulnerability to a geopolitical shock that the market has decided to ignore. The four hyperscalers together have announced over $200 billion in combined AI capex for 2026, much of it funded through investment-grade bond issuance that would become prohibitively expensive if the 10-year yield climbs another 100 basis points.

What the Bond Market's Shout Means for Fed Strategy

The bond market's refusal to rally on 175 basis points of cuts is a strategic signal that the Fed's policy framework is broken. Normally, the central bank controls the long end through expectations: if the market believes the Fed will keep rates low, the yield curve stays flat. But the 30-year at 5% shows the market has lost faith in the Fed's ability to control inflation or fiscal discipline. The Supreme Court's tariff ruling and the One Big Beautiful Bill Act have injected a fiscal expansion that directly contradicts the Fed's tightening bias. The Fed's Richard Fisher has expressed comfort with current policy, but that comfort is misplaced if the bond market continues to sell off. The central bank faces a choice: it can either validate the market's fears by raising rates preemptively, or it can try to jawbone the long end lower by signaling a longer hold. Neither option is attractive. A rate hike would validate Pimco's thesis and risk a recession. A hold would risk a continued sell-off in bonds that will eventually force the Fed's hand. The bond market is shouting because it sees a central bank that has lost control of the narrative, and a fiscal authority that is actively working against it.

Barron's analysis reinforces this dynamic: investors holding Treasury bills benefit directly from a prolonged hold, as T-bill yields remain anchored to the fed funds rate. With the Fed frozen at current levels, the $166 billion in tariff refunds flowing back to businesses and consumers represents a fiscal pulse that the bond market interprets as inflationary, not deflationary. The Treasury's expanded auction calendar compounds the pressure: each new 10-year or 30-year issuance dilutes the value of existing bonds and forces institutional buyers, from pension funds to insurance companies, to mark down their portfolios. The net effect is a bond market that prices in deteriorating fiscal discipline regardless of what the Fed's statement says, and a central bank whose words carry less weight every time the long end refuses to follow. The Fed's balancing act between anchoring inflation expectations and averting a bond market accident has no clean exit path available.

The most likely outcome is that the Fed will hold rates steady for months, watching to see whether the fiscal stimulus from tax cuts and tariff refunds fades before the geopolitical risk from Iran materializes. But Pimco's scenario is not a black swan; it is a known risk that the market has chosen to underprice. If the conflict escalates, the Fed will have no choice but to raise rates, and the 10-year yield will test 6% before the year is out. For investors, the only safe haven is short-dated Treasury bills, which benefit from a hold or a hike, while long-dated bonds and risk assets face a repricing that will rival the 2022 sell-off. The bond market is shouting, and the Fed is pretending not to hear.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.