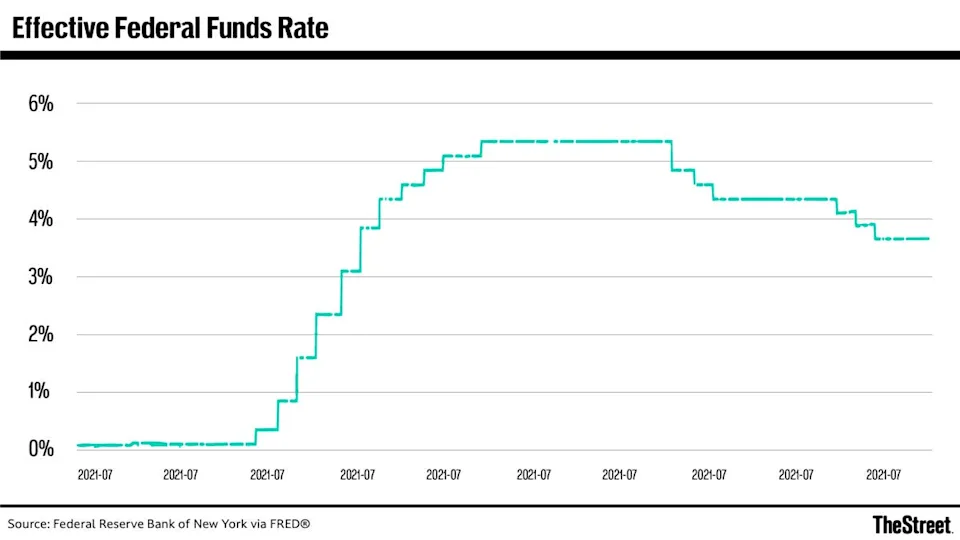

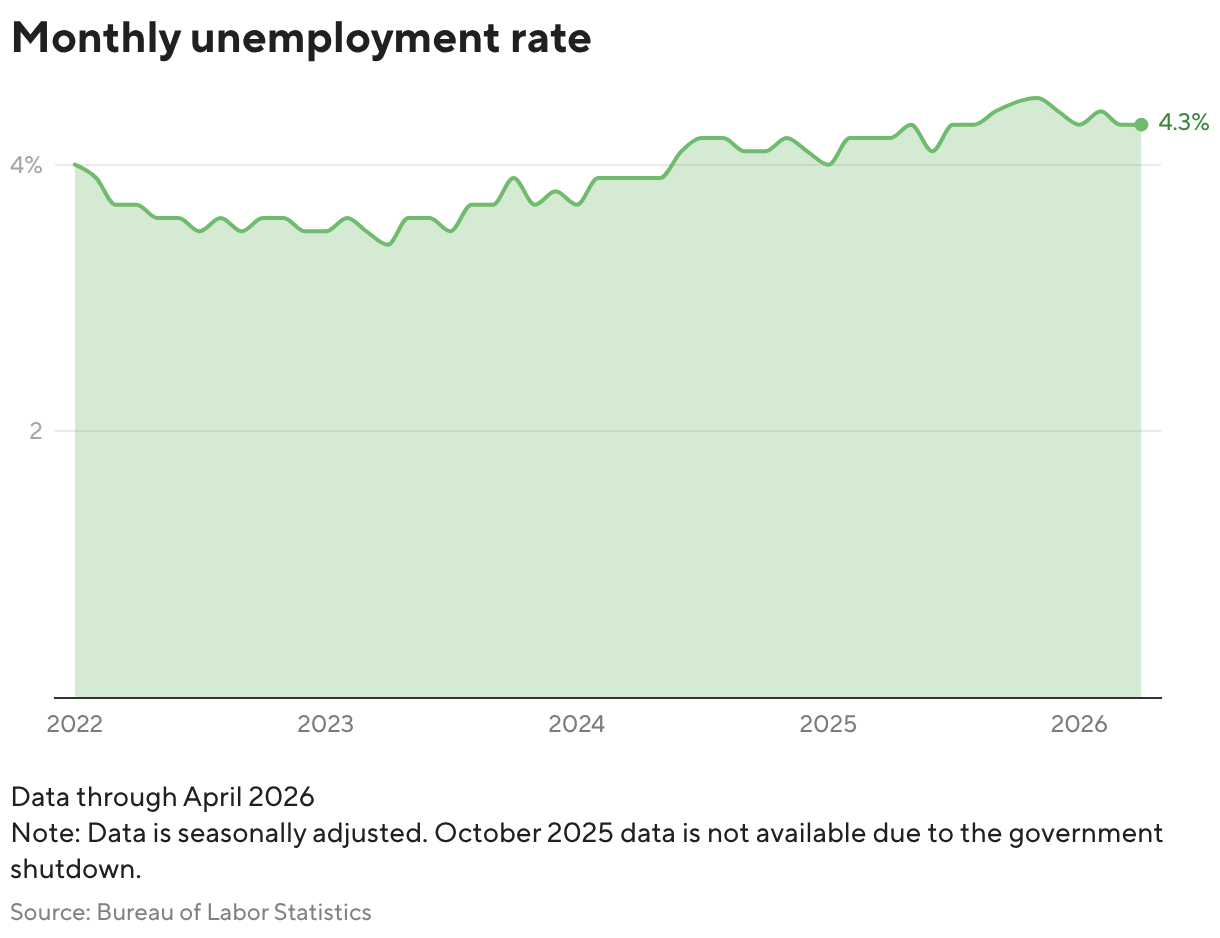

Bank of America has scrapped its forecast for Federal Reserve rate cuts in 2026, now predicting the central bank will hold rates steady until the second half of 2027. The revision, driven by persistent inflation and a resilient labor market, follows the April jobs report showing 115,000 new nonfarm payrolls, a figure that signals stabilization rather than weakness. The bank had previously expected two quarter-point cuts in September and October of this year. That timeline collapsed as inflation data failed to cool and the labor market absorbed the payrolls increase without triggering wage disinflation. Chicago Fed President Austan Goolsbee said all interest-rate options remain on the table, explicitly refusing to frame cuts as the only path forward. St. Louis Fed President William Poole described current U.S. interest rates as "well positioned," reinforcing the view that the central bank sees no urgency to ease. The shift matters because it redefines the macro baseline for every asset class: equity valuations built on a 2026 easing cycle now face a 12-to-18-month delay, while bond markets must reprice term premiums and corporate borrowing costs. The 115,000 payrolls number, while moderate by historical standards, removes the labor-market weakness argument that some doves had hoped would force the Fed's hand. With inflation still above target and job growth steady, the Fed has run out of reasons to cut, and Bank of America has become the first major bank to formalize a 2027 timeline.

The 115,000 Payrolls Threshold That Killed the 2026 Easing Narrative

The April nonfarm payrolls increase of 115,000 landed squarely in the Fed's "no action required" zone. The number is high enough to dismiss recession fears but low enough to avoid triggering new wage-inflation alarms. This Goldilocks outcome is precisely the kind of data that allows the Federal Open Market Committee to maintain its current stance without political or market pressure to move. For Bank of America's economists, the 115,000 figure was the final data point that invalidated their previous two-cut forecast for September and October 2026. The labor market is not cracking; it is normalizing at a level that keeps the Fed's focus on the cost of living rather than employment support. CNBC reported that the Fed's larger concern is the rising cost of living, not a flagging labor market, and the April jobs data reinforces that hierarchy. The 115,000 payrolls also closed the window for a data-dependent pivot: if the Fed were waiting for a clear signal of labor-market deterioration to justify cuts, that signal did not arrive. Instead, the number aligns with the "well positioned" assessment from Poole and the open-ended posture from Goolsbee. For the rate-cut camp, the jobs report was the final mile in a marathon they just lost.

Where the $570 Billion in Repriced Debt Flows

The delay to 2027 forces a wholesale repricing of corporate and sovereign debt. The two cuts Bank of America had penciled in for September and October 2026 would have lowered the federal funds rate by 50 basis points, reducing short-term borrowing costs for banks, corporates, and the Treasury itself. That 50-basis-point relief is now deferred by at least 12 months. For the U.S. government, which issued approximately $570 billion in new marketable debt in the first quarter of 2026 alone, the delay means higher interest expense on rolling over short-term bills and floating-rate notes. For investment-grade corporates, the spread between the fed funds rate and the yield on 10-year Treasuries will remain wide, compressing the arbitrage that makes debt-financed buybacks and M&A attractive. Bank of America's own trading desk will see reduced fixed-income volumes as clients postpone duration bets. The bank's forecast revision is also a self-fulfilling mechanism: when a major lender publicly abandons its easing call, the market prices out cuts, raising real yields and tightening financial conditions further. That tightening then reduces the probability of the very cuts the bank just ruled out. The 115,000 payrolls number thus cascades through every yield curve, every swap spread, and every corporate bond issuance calendar between now and late 2027. The April jobs report effectively locked in higher borrowing costs for the Treasury's upcoming refunding auctions, where the government will sell additional short-term bills at elevated rates.

Kevin Warsh, the Nomination Wild Card That Just Got Neutralized

Bank of America's earlier forecast for 2026 cuts had factored in the expectation that Kevin Warsh, if nominated as the next Fed chair, would steer policy toward easing. That political assumption was a material input to the bank's rate model. The April jobs report and the broader inflation persistence have now overridden that political variable. Warsh's potential influence on the FOMC's trajectory is no longer sufficient to overcome the data. This is a critical shift for market participants who had been positioning for a Warsh-led pivot: the nomination itself, should it occur, will now be read as a continuity signal rather than a policy change signal. The Fed's institutional inertia, reinforced by the 115,000 payrolls and the "well positioned" comments from Poole, means that even a new chair would face a committee that sees no reason to cut. The Warsh trade, long Treasuries, short the dollar, long equities, has therefore lost its catalyst. Positioning in 2-year Treasury futures had shifted materially through April in anticipation of a chair-driven pivot. Those positions are now unwinding as the data, not the nomination, sets the trajectory. The Fed's two-stage institutional buffer, with regional bank presidents reinforcing the chair's message through coordinated public commentary, means any incoming chair would need to move the entire FOMC rather than simply signal a new direction from the top. For Bank of America, removing the Warsh assumption from the forecast was a recognition that personnel changes cannot override the macro data. The bank's revised call is a bet that the Fed's reaction function is now data-dominant, not personality-dominant.

The Competitive Reshuffle: Bank of America vs. the Consensus

Bank of America's 2027 call puts it ahead of the consensus, which still prices in some probability of a 2026 cut. This divergence creates a trading and positioning opportunity. If Bank of America is correct, the rest of the Street will have to reprice rates higher and later, triggering a wave of short-covering in rate futures and a selloff in long-duration bonds. If Bank of America is wrong and cuts come in 2026, the bank will have missed a rally, but the reputational cost of being too hawkish is lower than being too dovish in this cycle. The bank's economists are effectively staking their credibility on the view that inflation is sticky and the labor market is resilient enough to keep the Fed on hold. The 115,000 payrolls number is the cornerstone of that bet. Other major banks, including JPMorgan and Goldman Sachs, have not yet moved to a 2027 baseline. That gap will drive significant flow in the coming weeks as clients ask whether to follow Bank of America or wait for more data. The bank's call also pressures the Fed to communicate more explicitly: if the market's most hawkish major forecaster is now at 2027, the FOMC may need to clarify whether that timeline is too pessimistic or too optimistic. The competitive dynamic is not just about forecasts; it is about which institutions control the narrative for the next 18 months of rate-market trading.

The Policy Signal: A Fed That Has Stopped Looking for Reasons to Cut

The collective message from the April jobs report, the Bank of America revision, and the comments from Goolsbee and Poole is that the Fed has stopped looking for reasons to cut. The central bank's reaction function has shifted from "when can we ease?" to "why would we ease?" The 115,000 payrolls answer that question: the labor market does not need stimulus, and inflation does not warrant accommodation. This is a structural shift in the Fed's posture, not a tactical pause. For the first time since the hiking cycle ended, the FOMC is operating without a bias toward the next move being a cut. Goolsbee's statement that all options are on the table, including no cuts, is the linguistic marker of that shift. The policy signal extends beyond rates: it tells the Treasury, corporate borrowers, and household lenders that the cost of capital will remain elevated for the foreseeable future. It tells the equity market that the Fed put has been moved from 2026 to 2027. And it tells foreign central banks that the dollar's yield advantage will persist, keeping emerging-market currencies under pressure. The 115,000 payrolls number is small in absolute terms but enormous in its signaling power: it is the data point that made the Fed comfortable with doing nothing, and that comfort will last until inflation or employment breaks decisively.

The forward-looking question is not whether the Fed will cut in 2027, but what will break before then to force its hand. Bank of America's forecast assumes that inflation will remain sticky and the labor market will stay resilient, but the risk to that call is asymmetric. If inflation accelerates, the timeline extends beyond 2027. If the economy tips into recession, cuts come sooner. The 115,000 payrolls number is the current baseline, but it is a trailing indicator. The leading indicators, consumer credit delinquencies, small business hiring plans, and industrial production, will determine whether Bank of America's 2027 call looks prescient or premature. Goolsbee's emphasis that all options remain on the table is a deliberate hedge against that asymmetry: it preserves optionality without committing the FOMC to a path that the data might soon invalidate. For now, the bank has drawn a line in the sand, and the rest of the market must decide whether to cross it or wait for the next jobs report, due in June, to redraw it. A miss below 80,000 payrolls would reopen the 2026 cut debate; a beat above 150,000 would likely push the consensus toward Bank of America's 2027 baseline and force a broader repricing of rate expectations across every major asset class.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.