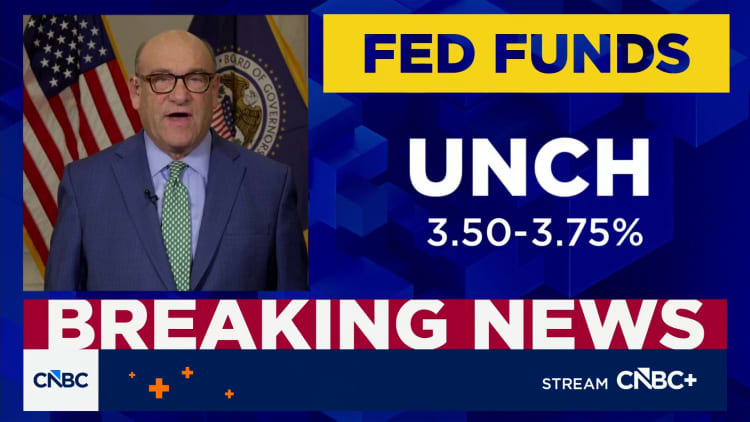

The Federal Reserve held its benchmark rate steady at 3.5% to 3.75% for the third consecutive meeting in April 2026, a decision that was widely expected but overshadowed by a rare public dissent. Cleveland Fed President Beth Hammack broke with the majority on the language of the statement, objecting to wording that implied the central bank's next policy move would be a rate cut. Hammack has publicly stated she expects rates to remain on hold "for quite some time," reflecting a hawkish faction within the Federal Open Market Committee that sees persistent inflation as a greater risk than slowing growth. The dissent marks the largest number of dissenting votes at a Fed meeting since 1992, underscoring an unusually deep division among policymakers. While the Fed cut rates by 75 basis points in 2025, the pace of easing has now stalled as inflation remains stubbornly above the 2% target. The decision to hold steady comes as loan demand is improving across the banking system, increasing competition for deposits and putting upward pressure on consumer savings rates. For investors and corporate treasurers managing cash positions, the message is clear: the era of rapid rate cuts is over, and the cost of holding cash is no longer falling.

Deposit Rate Competition Intensifies Despite Fed Pause

Despite the Fed's decision to hold rates flat, several banks have moved in the opposite direction on consumer deposit products. In April, a number of institutions raised yields on certificates of deposit, defying the typical pattern of deposit rates tracking the federal funds rate lower. According to data from Morgan Stanley, rates on CDs maturing in one year or less rose by 6 basis points to 3.71%, while rates on 13- to 36-month CDs edged up 1 basis point to 2.62%. The moves were concentrated among a subset of aggressive competitors: 8 of the 35 banks under Morgan Stanley coverage raised CD yields during the month. The divergence between Fed policy and deposit pricing reflects a structural shift in the banking landscape. Loan demand is improving, forcing lenders to compete more aggressively for funding. Banks that need to grow their deposit base to support lending are using CDs as a tool to lock in longer-term funding, even as the forward curve suggests rates will eventually fall. Morgan Stanley analyst Manan Gosalia expects CD rates to remain flat to slightly higher in the near term, a view that contradicts the typical relationship between Fed policy and deposit pricing. For savers, this creates a narrow window to lock in yields that will not be available once the Fed eventually resumes cutting. The 8 banks that raised CD yields in April are likely the first movers in a broader trend as loan demand continues to improve.

How the Fed's Hold Reshapes Bank Profitability

The Fed's extended pause at 3.5%–3.75% creates a specific profitability dynamic for the banking sector that differs from both a cutting and a hiking cycle. When the Fed is cutting, net interest margins typically compress as banks reprice loans faster than deposits. When the Fed is hiking, margins expand. In a prolonged hold, the outcome depends on deposit beta, the speed at which banks pass rate changes to depositors. With loan demand improving, banks face pressure to raise deposit rates to attract funding, which squeezes margins. The FDIC reports that the average savings account pays just 0.38%, a figure that highlights the gap between what banks pay the majority of depositors and what they offer on high-yield products. The best high-yield savings accounts currently offer up to 5.00%, a spread that creates a powerful incentive for depositors to move cash. Banks that rely heavily on low-cost core deposits, typically the largest institutions, benefit from the hold because they face less pressure to raise rates across their entire deposit base. Smaller and regional banks, which depend more on wholesale funding and brokered deposits, face a tighter squeeze. The Fed's hold effectively widens the competitive moat for large banks with sticky deposit franchises while punishing those that need to bid for marginal funding. This dynamic will drive consolidation pressure in the sector as smaller lenders struggle to maintain margins.

Winners and Losers Among Lenders and Savers

The rate hold creates a clear divide between winners and losers across the financial ecosystem. The biggest winners are the large money-center banks with deep, low-cost deposit bases. Institutions like JPMorgan Chase and Bank of America benefit from the status quo because their deposit costs are anchored to the 0.38% average savings rate, while they can lend at rates tied to the 3.5%–3.75% Fed funds rate. The spread remains wide without the margin compression that would accompany a cutting cycle. Regional banks that need to compete for deposits are relative losers, as they must raise CD and savings rates to attract funding in an environment where loan demand is improving but the Fed is not providing tailwinds. For savers, the winners are those who actively shop for yield. High-yield savings accounts offering up to 5.00% and short-term CDs yielding 3.71% provide real returns above inflation, even as the Fed holds steady. The losers are depositors who leave cash in traditional savings accounts earning 0.38%, effectively losing purchasing power. The FDIC data underscores this bifurcation: the average saver is being subsidized by the inactive depositor. The competitive dynamic will intensify as loan demand continues to improve, forcing more banks to raise deposit rates to fund growth.

Downstream Effects on Lending, Capex, and Corporate Cash Management

The Fed's hold at 3.5%–3.75% sends a specific signal to corporate treasurers and CFOs managing cash positions and capital expenditure plans. With the Fed signaling that rates will stay on hold for an extended period, the opportunity cost of holding cash is stable rather than declining. This removes the urgency to deploy cash into longer-duration assets or capital projects that was present during the 2025 cutting cycle. Corporate bond issuance is likely to remain elevated as companies lock in current yields before any potential future cuts. For banks, the improving loan demand environment creates a natural hedge against margin compression. As lending volumes grow, banks can offset the cost of higher deposit rates with increased interest income on the asset side. The 75 basis points of cuts delivered in 2025 have already flowed through to lower borrowing costs for variable-rate loans, but the hold means that new fixed-rate loans will be priced at current levels for the foreseeable future. This creates a stable environment for corporate borrowers to plan capex, but it also means that the refinancing wave that typically accompanies a cutting cycle will be delayed. For the housing market, mortgage rates are likely to remain elevated relative to the 2020-2021 period, constraining affordability. The Fed's hold effectively freezes the cost of capital at a level that is restrictive for rate-sensitive sectors but not restrictive enough to trigger a recession. Inventory-heavy manufacturers and commercial real-estate developers face the sharpest burden, as the cost of revolving credit facilities and bridge loans stays elevated. Treasury teams at large multinationals, by contrast, are earning 4.8%–5.0% on overnight repo and short-dated T-bills, a return that was unthinkable in the zero-rate era. The longer the hold persists, the wider this productivity gap grows between cash-rich companies and those dependent on cheap debt to fund expansion.

What the Hammack Dissent Signals About Fed Policy

Beth Hammack's dissent on the language suggesting the next move is a cut is the most significant signal from the April meeting. The last time the Fed saw this level of dissent was 1992, a period when the central bank was navigating the aftermath of a recession and an uncertain inflation outlook. Hammack's position — that rates will remain on hold "for quite some time," reflecting the view of a hawkish minority that believes the Fed should not pre-commit to easing until inflation is clearly defeated. The dissent matters because it constrains Chair Jerome Powell's ability to signal future cuts without risking further division. If the Fed's statement language is seen as a commitment to cut, Hammack's objection creates a credibility problem: the market will price in cuts that a significant faction of the FOMC does not support. This dynamic increases the probability that the Fed will remain on hold longer than the market currently expects. For investors, the dissent is a reminder that the Fed is not a monolith. The hawkish faction will grow if inflation data does not improve, making the next move a cut less certain. The 75 basis points of cuts in 2025 will prove to be the entirety of the easing cycle if inflation reaccelerates. The Hammack dissent effectively puts the market on notice that the path to lower rates is not guaranteed and that the Fed's next move could just as easily be a hike if inflation pressures persist.

The Fed's hold at 3.5%–3.75% with a prominent hawkish dissent creates a policy environment that will persist through the second half of 2026. The improving loan demand dynamic will continue to put upward pressure on deposit rates, creating a window for savers to lock in yields that will not survive a future cutting cycle. For banks, the extended hold favors large institutions with sticky deposit bases while squeezing regional lenders that must compete for marginal funding. The Hammack dissent signals that the Fed's next move is far from certain, and the market should not assume that the 2025 cuts will be followed by further easing. If inflation remains above target, the hawkish faction will grow, and the next rate change will be a hike rather than a cut. Corporate treasurers should plan for a stable cost of capital through year-end, while investors in bank stocks should favor large-cap franchises with low-cost deposit advantages. The era of easy monetary policy is not returning anytime soon, and savers who act now will lock in the best yields of this cycle before the next policy shift closes the window.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.