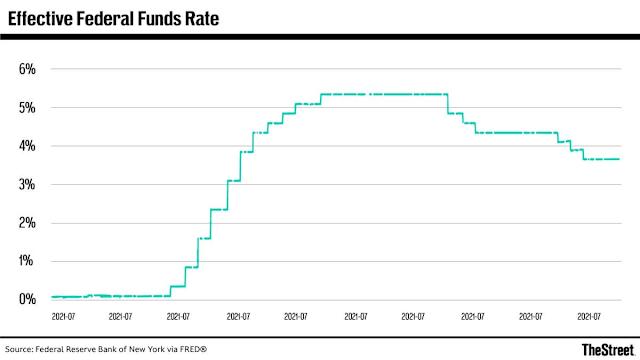

Goldman Sachs has pushed back its forecast for the next two Federal Reserve rate cuts to December 2026 and March 2027, a hawkish revision that signals the central bank will keep borrowing costs elevated for at least another 18 months. The bank's economists now expect inflation in 2026 to run above the Fed's 2% target, with energy cost pass-through likely keeping core PCE near 3% throughout the year. The revised timeline comes after the Federal Open Market Committee held the federal funds rate at 3.50% to 3.75% on April 29, a decision that drew four dissents, the most since 1992. CME FedWatch data places a 93.4% probability on the Fed holding rates steady at the June 17 meeting. Goldman Sachs Asset Management's Lindsay Rosner said hawks will gain ground at that June FOMC meeting, a dynamic that directly pressures risk assets like Bitcoin and Ethereum as hopes for near-term rate cuts evaporate. The delay matters because every month the Fed stays on hold tightens financial conditions for speculative assets, corporate borrowing, and emerging-market debt, creating a liquidity vacuum that will define portfolio strategy through 2026.

The 3.50%–3.75% rate floor and its origins

The FOMC's April 29 decision to hold the federal funds rate at 3.50% to 3.75% marks the latest extension of a pause that began when the Fed halted its aggressive rate-cut campaign last September. At that time, the key overnight benchmark funds rate stood at 2%. The central bank has since raised rates in a series of moves that brought the target range to its current level, but the April meeting revealed deep internal division. Four dissents, the highest count in 34 years, signal that the hawkish faction within the committee believes the Fed should have raised rates further, not held steady. The dissents reflect a growing concern that inflation is not merely sticky but structurally embedded, driven by energy cost pass-through that Goldman Sachs now expects to keep core PCE near 3% through the end of 2026. The 93.4% probability assigned by CME FedWatch to a hold at the June 17 meeting indicates that markets have fully priced in no change. The mechanism at work is straightforward: the Fed's dual mandate prioritizes price stability over maximum employment when inflation exceeds 2%, and the current data gives the hawks ammunition to argue for a longer hold. The April meeting marked the first time since 1992 that four FOMC members dissented from a rate decision, underscoring the depth of internal disagreement over the appropriate policy path.

How the delay reshapes capital flows

The delayed rate cut timeline directly alters the cost of capital for every asset class that trades on forward rate expectations. For Bitcoin and Ethereum, which have rallied in past cycles on the prospect of lower rates, the Goldman Sachs revision removes the near-term catalyst for speculative inflows. Crypto markets had priced in at least one cut by mid-2026; the December 2027 timeline eliminates that thesis. The International Monetary Fund has warned that persistent rate differentials between the U.S. and other major economies trigger capital flight from emerging markets, as investors chase higher yields in dollar-denominated assets. On corporate balance sheets, the delay means companies that refinanced floating-rate debt at the 3.50%–3.75% level will face another 18 months of elevated interest expense. Goldman Sachs's own asset management unit, through Lindsay Rosner, has signaled that the hawks' influence will only grow if core PCE remains near 3%. The CME FedWatch data reinforces the market's acceptance of this reality: a 93.4% probability of a hold at June 17 leaves only a 6.6% chance of a cut, a spread that compresses risk premiums across equities, credit, and crypto. The shift forces portfolio managers to reassess allocations built on the assumption that rate relief would arrive by mid-2026.

A stronger dollar, which appreciates when the Fed holds rates above global peers, adds a second layer of pressure on Bitcoin and Ethereum. Both assets are priced in dollars, meaning dollar appreciation directly erodes returns for non-dollar investors. The Goldman Sachs forecast implies that U.S. short-term yields will remain above 3.50% through most of 2026, a spread that makes dollar-denominated cash equivalents (money market funds, T-bills, and short-duration bonds) structurally attractive relative to risk assets. The CME FedWatch 93.4% hold probability at June 17 reflects this calculus: the market has concluded that the risk-free rate will not decline before the fourth quarter of 2026, removing the opportunity-cost argument for holding zero-yield assets. Goldman Sachs's December 2026 cut forecast effectively sets the floor for how long portfolio managers must hold that view.

Which institutions gain and lose from the hold

The winners in this extended rate environment are large-cap banks like Goldman Sachs itself, which benefit from wider net interest margins when the yield curve steepens. The losers include highly leveraged crypto lenders, venture capital firms that depend on low-rate liquidity for exits, and regional banks still carrying underwater bond portfolios from the 2022–2023 rate hikes. Thomas Hoenig, the former Fed president, has warned that the central bank should not wait too long to raise rates further, a view that aligns with the four April dissents and confirms the hawkish camp will push for a hike rather than a hold at future meetings. For asset managers, the delay forces a rotation out of duration-sensitive plays, such as long-duration Treasuries, growth stocks, and crypto, into short-duration instruments and commodities that benefit from persistent inflation. The CME FedWatch data shows that the probability of a rate cut at the September 2026 meeting has fallen below 30%, meaning the market now expects the Fed to remain on hold through the second half of 2026. This competitive reshuffling favors institutions with strong deposit franchises and punishes those reliant on wholesale funding or speculative asset appreciation.

The net interest margin expansion for large banks follows a direct mechanism: when the Fed holds the short end of the yield curve at 3.50%–3.75% and longer-duration assets reprice gradually, banks that fund themselves with deposits below the policy rate collect a spread that widens with each quarter the hold persists. Goldman Sachs, JPMorgan Chase, and other major deposit-funded institutions benefit from this dynamic in commercial and industrial lending, where floating-rate loans reset to the higher policy rate automatically. The four April dissents, leaning hawkish, indicate the committee's direction of travel favors a higher rate floor, not a lower one, extending the margin expansion window for deposit-funded institutions through at least the first quarter of 2027.

Downstream effects on hyperscalers, fabs, and enterprise buyers

The extended rate hold creates a second-order drag on capital-intensive sectors that depend on cheap debt to finance long-duration projects. Hyperscalers like Amazon Web Services, Microsoft Azure, and Google Cloud face higher financing costs for their data center buildouts, which typically require $1 billion to $3 billion per facility and have payback periods of five to seven years. Semiconductor fabs, which cost $10 billion to $20 billion to construct, become less attractive when the risk-free rate sits at 3.50%–3.75% and shows no sign of declining until late 2026. Enterprise buyers of cloud services and AI hardware will see their procurement budgets squeezed as CFOs allocate more capital to interest expense and less to technology investment. The energy cost pass-through that Goldman Sachs expects to keep core PCE near 3% also raises operating costs for data centers, which consume 50 to 100 megawatts each and face rising electricity prices. For the crypto mining industry, which is energy-intensive and highly sensitive to both power costs and Bitcoin prices, the delay compounds margin pressure. The CME FedWatch probability of a hold at June 17 reinforces the message that the Fed will not ease financial conditions for these capital-intensive sectors anytime soon. Data center operators now face the dual challenge of higher construction financing costs and rising electricity bills, compressing margins across the infrastructure layer.

The policy signal behind the four dissents

The four dissents at the April FOMC meeting, the most since 1992, send a clear policy signal: the Fed's hawkish wing believes the central bank has already waited too long to tighten further. Thomas Hoenig's warning that the Fed should not wait too long to raise rates captures the sentiment of this faction, which views the current 3.50%–3.75% rate as insufficient to bring inflation back to 2%. The dissents also indicate that Chair Jerome Powell faces a credibility challenge in maintaining the current pause, as the hawkish members will force a rate hike at a future meeting if inflation data does not improve. Goldman Sachs's revised forecast, which pushes the first cut to December 2026 and the second to March 2027, effectively endorses the hawkish view that the Fed will need to hold rates at or above current levels for an extended period. The International Monetary Fund has flagged that prolonged U.S. rate elevation destabilizes global capital flows, but the domestic policy calculus prioritizes inflation control over international spillovers. The signal for markets is unambiguous: the era of easy money is not returning in 2026, and any portfolio constructed on the assumption of near-term rate cuts must be rebuilt.

The Goldman Sachs revision is not a forecast. It is a recognition that the Fed's reaction function has shifted permanently. The four dissents, the 93.4% hold probability at June 17, and the expectation that core PCE will remain near 3% through 2026 all point to a regime where the federal funds rate stays at 3.50%–3.75% for at least 18 more months. Asset managers should prepare for a world where the cost of capital does not decline, where crypto and growth stocks trade without a rate-cut tailwind, and where the only easing comes from fiscal policy or a recession that forces the Fed's hand. The next catalyst will be the June 17 FOMC meeting, where Lindsay Rosner expects hawks to gain ground, and where the market will see whether the four dissents become five or six. Until then, the liquidity that markets crave will remain locked behind a 2% inflation target that shows no sign of being met.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.