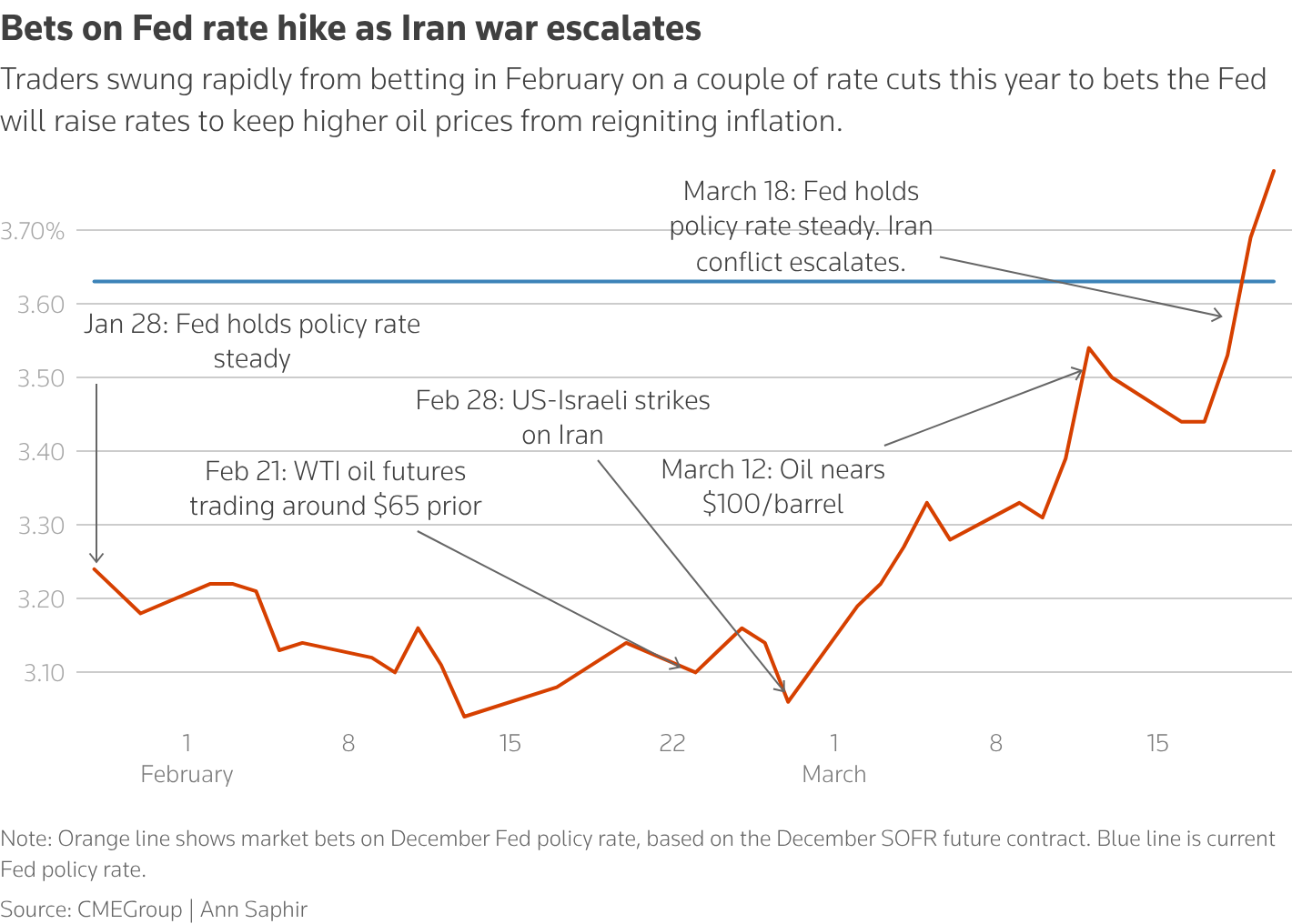

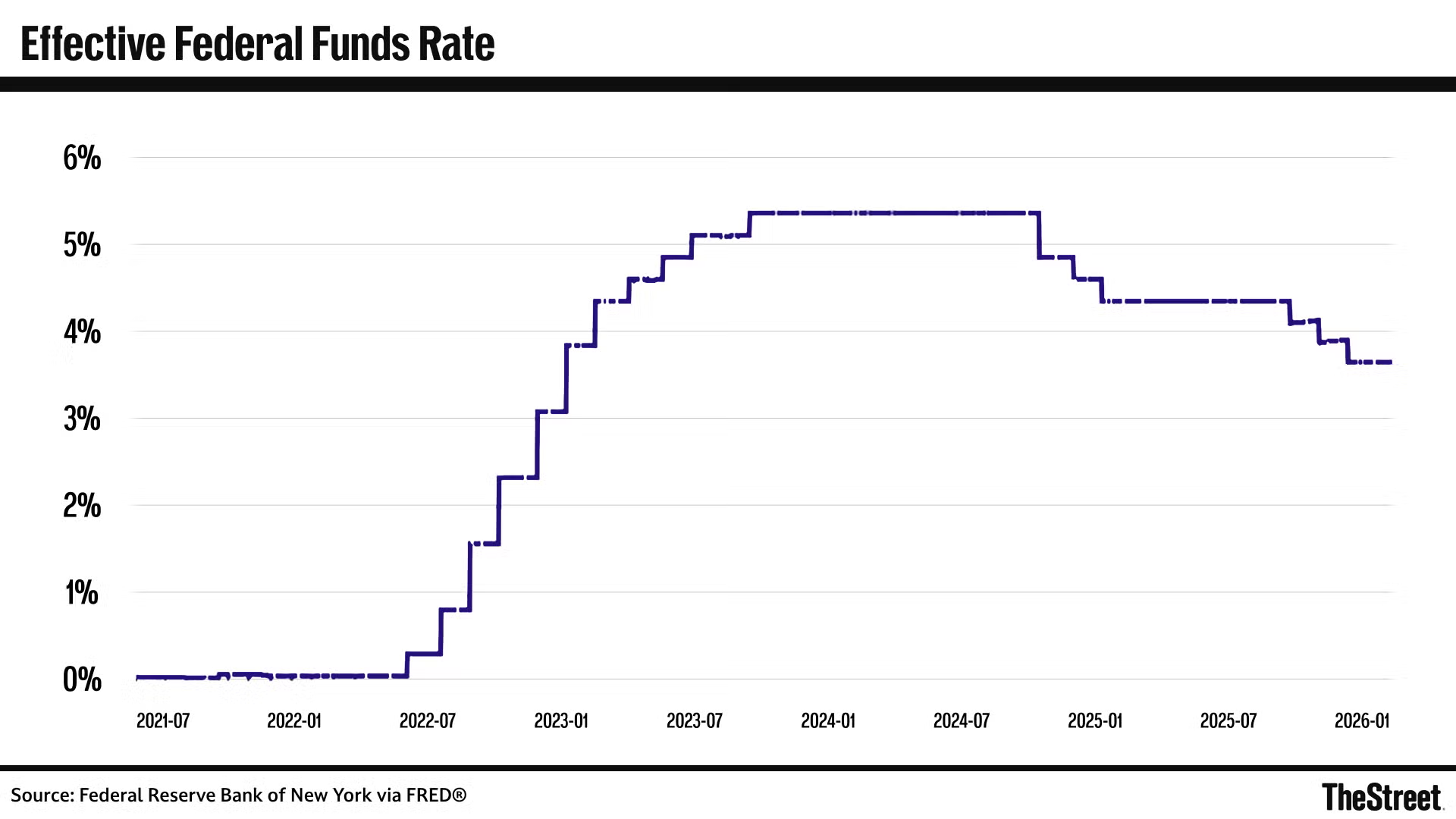

The probability of a Federal Reserve rate hike in 2026 jumped to 10% from 0% in a single day following Jerome Powell's April press conference, as markets recalibrated their inflation outlook in the wake of the Iran war and a sharp oil price spike. The Fed held its target rate steady at 3.50%–3.75% at the April meeting, but the shift in market pricing signals a dramatic reversal from the rate-cut consensus that dominated Wall Street just weeks earlier. JPMorgan analysts flagged that a key bond yield indicator turned positive for the first time since 2022, a technical signal that historically precedes tightening cycles. The catalyst is straightforward: the Iran conflict has pushed crude prices higher, feeding into broader goods and transportation costs, and threatening to undo the progress the Fed made on inflation during 2025. Markets are now pricing in a non-trivial chance that the next move from the Fed is a hike, not a cut, upending the dovish narrative that drove asset prices higher over the past year. This matters now because it rewrites the playbook for every rate-sensitive asset class, from high-yield savings accounts to corporate bonds to equities, and forces investors to hedge against a scenario that was considered impossible just 48 hours ago.

The Market-Implied Probability Shift from Zero to Double Digits

The 10% probability figure is not a forecast from the Fed, but a market-implied reading derived from fed funds futures and options pricing. A day before Powell's press conference, that probability sat at exactly 0%, meaning the market assigned no chance to a rate increase within the next 12 months. The shift reflects a rapid repricing of inflation expectations, driven primarily by the Iran war's impact on global oil supply. Crude prices have risen sharply since the conflict escalated, and the pass-through to consumer prices is already visible in gasoline and shipping costs. JPMorgan's quantitative team noted that a key bond yield indicator, the spread between the 2-year and 10-year Treasury, turned positive for the first time since 2022, a move that historically signals the market is pricing in tighter monetary policy ahead. The Fed's own dot plot from the March meeting showed no rate hikes, but Powell's April press conference language was more hawkish than expected, leaving the door open to action if inflation re-accelerates. The market took that as a signal to reprice risk. Importantly, the 10% probability is still low, but the direction of change from zero to double digits is what matters for positioning. It forces traders to consider tail risks that were previously ignored, and it raises the cost of being caught short volatility. The fed funds futures market now reflects a non-zero chance of a hike at the June or July meeting, a scenario that was unthinkable before the Iran conflict escalated.

How the Fed's Stance Reshapes the High-Yield Savings Market

High-yield savings account (HYSA) rates are directly tied to the federal funds rate, and the sudden shift in rate expectations has immediate implications for savers. The Fed cut rates by 75 basis points in 2025, which pushed HYSA yields down from their 2024 peaks, but the best accounts still offer up to 5.00% APY as of May 2026. If the Fed holds rates steady at 3.50%–3.75% for the rest of the year, those yields will likely remain elevated compared to the pre-2024 era. However, if the 10% probability of a hike materializes, HYSA rates will rise further, extending the high-rate environment that has been a boon for retail savers. The average savings account pays just 0.38% according to FDIC data, so the gap between the best HYSA and the average account remains wide at roughly 4.62 percentage points. Banks that aggressively compete for deposits, particularly online-only institutions, will keep their rates high to retain customers. The Fed's hawkish tilt also means that banks face less pressure to cut deposit rates, which supports their net interest margins. For consumers, the window to lock in high yields is not closing yet, but the uncertainty around rate direction means that floating-rate accounts will become more attractive than fixed-term CDs. The key dynamic is that the Fed's inaction or potential action directly determines whether the 5.00% HYSA yield becomes a floor or a ceiling.

JPMorgan's Bond Signal and the Competitive Landscape for Banks

JPMorgan's identification of the bond yield indicator turning positive for the first time since 2022 is a critical signal for the banking sector. The 2-year/10-year spread moving into positive territory typically reflects expectations of stronger economic growth or tighter monetary policy, or both. For banks, a steeper yield curve is generally positive because it widens the spread between their short-term funding costs and long-term lending rates. This benefits large money-center banks like JPMorgan itself, which have large deposit bases and significant loan books. Regional banks, which were battered during the 2023 crisis, also stand to gain if the curve steepens further, as it improves their net interest margins. However, the competitive landscape is not uniform. Banks that relied on wholesale funding during the low-rate era will face higher costs if the Fed hikes, while those with sticky core deposits will benefit. The FDIC-insured average savings rate of 0.38% underscores how much pricing power the largest banks have: they can keep deposit rates low while still attracting customers through brand and convenience. Online banks and fintechs offering HYSA rates near 5.00% will need to maintain that spread to keep deposits from flowing back to traditional banks. JPMorgan's signal is not just a technical curiosity; it is a strategic input for every bank's asset-liability committee, and it will drive decisions on loan pricing, deposit rates, and capital allocation for the rest of 2026.

Downstream Effects on Corporate Borrowing, Housing, and Consumer Credit

A Fed rate hike, or even the credible threat of one, cascades through the entire credit system. Corporate bond yields will rise, increasing borrowing costs for investment-grade and high-yield issuers. Companies that refinanced at lower rates in 2025 will be insulated, but those with floating-rate debt or upcoming maturities will face higher interest expenses. The housing market, which has already adjusted to the 3.50%–3.75% Fed funds rate, will see mortgage rates climb further if the yield curve steepens. The 30-year fixed mortgage rate, which tracks the 10-year Treasury yield, will move higher as the bond market reprices for tighter policy. This will further suppress home sales and refinancing activity, which have been sluggish since 2023. Consumer credit is another pressure point: credit card rates, which are already at elevated levels, will rise if the Fed hikes, squeezing households that carry balances. Auto loan rates will follow suit. The broader economic impact is that the Iran war is creating a supply-side inflation shock that the Fed cannot address with rate cuts, and a hike would deliberately slow demand to offset that shock. This is a painful trade-off for the Fed, but the market is now pricing it as a plausible outcome. For investors, the second-order effects include higher discount rates for equity valuations, lower duration bond prices, and a stronger dollar, which will weigh on emerging market assets and commodity prices outside of oil.

William Poole's Rate Positioning and the Fed's Policy Signal

St. Louis Fed President William Poole stated that U.S. interest rates appear well positioned, a comment that carries weight given his hawkish reputation and his historical focus on inflation control. Poole's assessment shows that the current 3.50%–3.75% rate is appropriate for the economic conditions the Fed sees today, but the market's 10% hike probability implies that conditions could change. Poole's comment is a signal that the Fed is not panicking, but it also leaves room for action if the Iran war drives inflation persistently higher. The broader policy signal from the Fed is one of caution: the central bank is unwilling to commit to cuts, and it is now unwilling to rule out hikes. This is a dramatic shift from the narrative that dominated 2025, when the Fed was cutting rates to support a slowing economy. The Iran war has upended that calculus by reintroducing supply-side inflation risks that the Fed cannot ignore. The market is reading this as a regime change: the Fed is no longer a reliable tailwind for risk assets, and the burden of proof has shifted to inflation data to justify further easing. For investors, the takeaway is that the Fed's reaction function has become asymmetric: it will hike if inflation persists, but it will not cut unless growth collapses. This is a more hawkish stance than the market had priced, and it will force a repricing of risk across every asset class. The 10% probability is a warning shot, not a certainty, but it changes the conversation from "when will the Fed cut" to "will the Fed hike."

What investors should track in the weeks ahead is the trajectory of oil prices and the monthly CPI releases. If crude stabilizes and headline inflation stays near the Fed's 2% target, the 10% hike probability will likely fade back toward zero and the dovish consensus will reassert itself. But if the Iran conflict disrupts global supply chains further, or if energy costs feed through to services inflation, the market will reprice that probability sharply higher. Fed Chair Powell has made clear that the central bank is data-dependent, meaning each CPI print now carries outsized market significance. The June Federal Open Market Committee meeting will be the first real test: if inflation data between now and then surprises to the upside, a hike becomes a live option rather than a tail risk. Treasury yields, particularly the 2-year and 10-year benchmarks that JPMorgan's analysts are watching, will serve as the real-time signal of how the market is pricing that probability. Savers, borrowers, and investors across every asset class should treat the current rate environment as conditionally stable rather than durably dovish, adjusting their positioning to account for a geopolitical risk premium that was absent just weeks ago.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.