ASML, Europe's most valuable company at a $530 billion market cap, faces its first credible challenge in a decade as startup Substrate, backed by Peter Thiel and valued at over $1 billion, races to build a rival extreme ultraviolet lithography (EUV) machine. ASML currently holds an unbroken monopoly on the $200 million–$400 million machines that produce the world's most advanced semiconductors, a position CEO Christophe Fouquet recently declared impregnable, telling TechCrunch that "no one is coming for us." Yet Substrate has raised over $100 million to prove him wrong, targeting the same nanometer-shrinking technology that powers every leading AI chip from Nvidia, AMD, and others. The timing is no coincidence. Microsoft, Meta, Amazon, and Google have collectively committed over $600 billion in AI infrastructure spending in 2026, with total Big Tech capital expenditures expected to top $1 trillion by 2027. This spending wave is already reshaping the semiconductor supply chain: AMD reported Q1 2026 revenue of $10.3 billion, up 38% year-over-year, driven entirely by data center demand, while Marvell Technology saw its price target raised to $195 from $120 at UBS on the back of its data infrastructure solutions. The convergence of a lithography monopoly challenge and a trillion-dollar capex cycle means the stakes for chip manufacturing have never been higher.

Where the $570M per machine profit lives

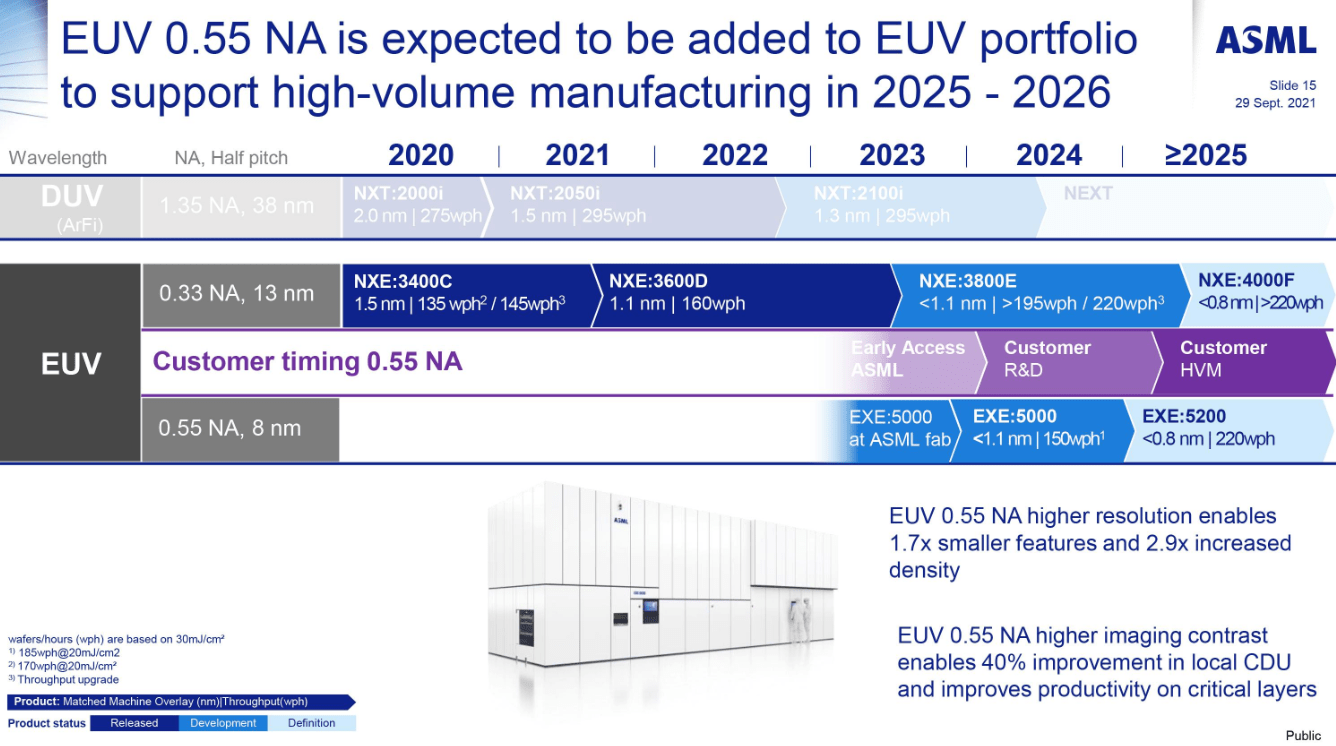

ASML's monopoly on EUV lithography machines is not just a technological feat. It is a pricing fortress. Each machine sells for between $200 million and $400 million, with gross margins estimated above 60%, meaning ASML captures roughly $120 million to $240 million in gross profit per unit. The company ships dozens of these machines annually to a handful of customers, primarily TSMC, Samsung, and Intel, generating the bulk of its $530 billion market capitalization. The economics are simple: no other company on earth can produce the 13.5-nanometer wavelength light required to etch the smallest features on advanced chips, a process that requires bouncing laser-generated plasma off a series of mirrors so precise they would be smooth to an atom if scaled to the size of Germany. Substrate's challenge is therefore not just technical but economic. To displace ASML, it must not only replicate this physics but also convince chipmakers to qualify an untested tool for fabs that cost $20 billion to build. ASML's installed base and decades of process integration knowledge create switching costs that far exceed the machine's price tag. The monopoly has allowed ASML to dictate terms, collect prepayments, and maintain R&D spending of over $2 billion annually. This is a moat Substrate must cross with just $100 million in funding. ASML ships roughly 50 EUV machines per year, each generating between $120 million and $240 million in gross profit, which means the company earns an estimated $6 billion to $12 billion in gross profit annually from EUV alone.

How $600B in Big Tech capex flows through AMD's P&L

AMD's Q1 2026 results offer the clearest signal yet that AI infrastructure spending is translating directly into semiconductor revenue. The company reported $10.3 billion in revenue, a 38% year-over-year increase, with non-GAAP operating income of $2.5 billion, up 43% from the prior year. The data center segment, which includes AMD's Instinct MI-series AI accelerators and EPYC server CPUs, is the primary driver of both revenue and earnings growth. GAAP gross margin stood at 53%, while non-GAAP gross margin reached 55%, reflecting the favorable mix shift toward higher-margin data center products. CEO Lisa Su has positioned AMD as the primary alternative to Nvidia in AI training and inference, a strategy that gains credibility with every hyperscaler commitment. Microsoft, Meta, Amazon, and Google have collectively pledged over $600 billion in 2026 AI infrastructure spending, a figure that includes data center construction, networking equipment, and the chips that power AI workloads. AMD's revenue growth of 38% outpaces the broader semiconductor market, suggesting it is capturing share within that spending envelope. The operating income growth of 43% further indicates operating leverage as fixed costs are spread over a larger revenue base. For investors, the question is whether AMD can sustain this trajectory as Nvidia launches its next-generation architecture and as custom ASIC designs from Broadcom and Marvell gain traction with hyperscalers.

Marvell and Nvidia reshape the data infrastructure pecking order

Marvell Technology, a supplier of data infrastructure semiconductor solutions, is emerging as a direct beneficiary of the AI capex surge, with UBS raising its price target to $195 from $120, a 62.5% increase. The upgrade reflects Marvell's position in the networking and data movement layer of AI infrastructure, a segment that grows in importance as AI clusters scale to tens of thousands of accelerators. Marvell's custom ASIC designs for hyperscalers, combined with its networking silicon, place it at the intersection of two powerful trends: the need for higher-bandwidth interconnects and the push for purpose-built AI chips. Nvidia's decision to invest up to $3.2 billion in Corning for optical fiber technology underscores the same dynamic: AI data centers require entirely new physical infrastructure to move data between GPUs at speeds that copper cannot support. Marvell competes directly with Broadcom in the custom ASIC market and with Intel in networking, but its focus on data infrastructure gives it a narrower, more defensible position. The raised price target from UBS signals that analysts see Marvell capturing a disproportionate share of the $1 trillion in Big Tech capex expected by 2027. The competitive reshuffle is clear: Nvidia dominates training, AMD challenges in inference, and Marvell owns the pipes that connect them. The stakes extend beyond valuation. Marvell's PAM4 DSPs and 800G networking ICs are embedded in nearly every hyperscaler AI cluster deployed in 2025 and 2026. Each additional 10,000-GPU cluster that Meta or Google brings online requires tens of millions in switching and optical interface silicon, a market where Marvell has few direct competitors at scale. The UBS upgrade is therefore less a discovery call and more a catch-up to a structural shift in how AI capex flows through the data infrastructure stack, one that Marvell is positioned to compound as Big Tech's 2027 spending crosses the trillion-dollar threshold.

The $1 trillion capex bottleneck in fabs, packaging, and HBM

The downstream effects of Big Tech's $600 billion 2026 spending commitment, and the $1 trillion projected for 2027, are cascading through every layer of the semiconductor supply chain. Foundry capacity at TSMC and Samsung is sold out through 2027 for advanced nodes, with EUV lithography machines as the gating factor. ASML ships only about 50 EUV machines per year, each capable of producing roughly 100,000 wafers annually. At $200 million to $400 million per machine, the capital required to expand capacity is staggering, and any disruption to ASML's supply, whether from Substrate's challenge or export controls, would ripple through the entire AI chip ecosystem. Advanced packaging, particularly TSMC's CoWoS (chip-on-wafer-on-substrate) technology, is another bottleneck, with lead times extending beyond 12 months. High-bandwidth memory (HBM) from Samsung and SK Hynix is similarly constrained, as each AI accelerator requires multiple HBM stacks. Enterprise buyers face a different kind of bottleneck: allocation. Hyperscalers with $600 billion in collective spending power are pre-purchasing capacity, squeezing out smaller cloud providers and enterprise customers. The result is a two-tier market where only the largest buyers can secure leading-edge chips, while everyone else waits. Regulators in the US, EU, and Japan are watching closely, with export controls on EUV technology to China already in place and potential antitrust scrutiny of ASML's monopoly looming.

What the Substrate challenge says about ASML's strategic vulnerability

ASML CEO Christophe Fouquet's public dismissal of Substrate, "no one is coming for us," is precisely the kind of statement that invites scrutiny. The startup, founded by a protégé of Peter Thiel, has raised over $100 million and achieved a $1 billion valuation without shipping a single production tool. That valuation reflects investor belief that ASML's monopoly is vulnerable not because its technology is weak, but because the geopolitical and market dynamics that sustain it are shifting. The US and EU are both pursuing semiconductor self-sufficiency, with the CHIPS Act and the European Chips Act funding alternative lithography research. Substrate is the first credible private-sector attempt to commercialize that research, but it will not be the last. The strategic signal is clear: the era of single-source dependency for critical chipmaking equipment is ending, whether through competition, regulation, or both. For ASML, the risk is not that Substrate ships a machine tomorrow, but that the mere possibility of competition erodes its pricing power and forces it to invest more heavily in R&D and customer support, compressing margins. For the broader semiconductor industry, a second EUV supplier would reduce lead times, lower costs, and accelerate the pace of innovation, a win for hyperscalers spending $1 trillion on AI infrastructure. The monopoly is intact today, but the seeds of its disruption have been planted. ASML's response will reveal whether Fouquet's confidence is strategic posturing or genuine conviction. The company spends over $2 billion annually on R&D, a figure that dwarfs Substrate's total funding, but incumbency rarely protects a single-product monopoly against a well-capitalised challenger with geopolitical wind at its back. The CHIPS Act's $52 billion in semiconductor incentives and Europe's Chips Act both include alternative lithography research provisions that could compress the decade-long runway ASML currently assumes separates it from credible competition.

The next twelve months will determine whether Substrate's $1 billion valuation is a speculative bet or the beginning of a genuine technological shift. If the startup demonstrates a working prototype, ASML's stock and its $530 billion market cap will face the first real test of its monopoly premium. Meanwhile, the $600 billion in Big Tech AI spending for 2026 is already locked in, flowing through AMD's data center revenue, Marvell's networking silicon, and Nvidia's optical fiber investments. The trillion-dollar question is whether the supply chain can keep up. ASML's EUV machines, TSMC's CoWoS packaging, and HBM production are all operating at maximum capacity, and any disruption from a rival lithography machine, export controls, or a natural disaster would create a bottleneck that delays AI deployment for years. The smart money is betting that the monopoly breaks before the spending stops.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.