Chancellor Reeves announced plans to sever the long-standing link between wholesale gas and electricity prices in the UK, a structural reform that would fundamentally rewire how household and industrial power is priced. Under the current system, the marginal cost of gas sets the wholesale electricity price across the entire market, even when the power is generated by cheaper renewables or nuclear plants. Reeves aims to replace that mechanism with a system that reflects the actual generation mix, effectively lowering the price paid for electricity produced by low-carbon sources. The Treasury estimates the change will reduce the average annual household electricity bill by £150 to £200, though the precise savings depend on how quickly the new pricing model is implemented and how generators respond. This is the most significant intervention in UK electricity market design since the 2013 Electricity Market Reform, and it arrives as energy costs remain a top voter concern heading into the next general election. The move matters now because it directly challenges a core assumption of the UK's deregulated power market: that gas sets the price. If executed, it will create a new pricing regime that other European countries are watching closely.

How the gas-price link inflates every electricity bill

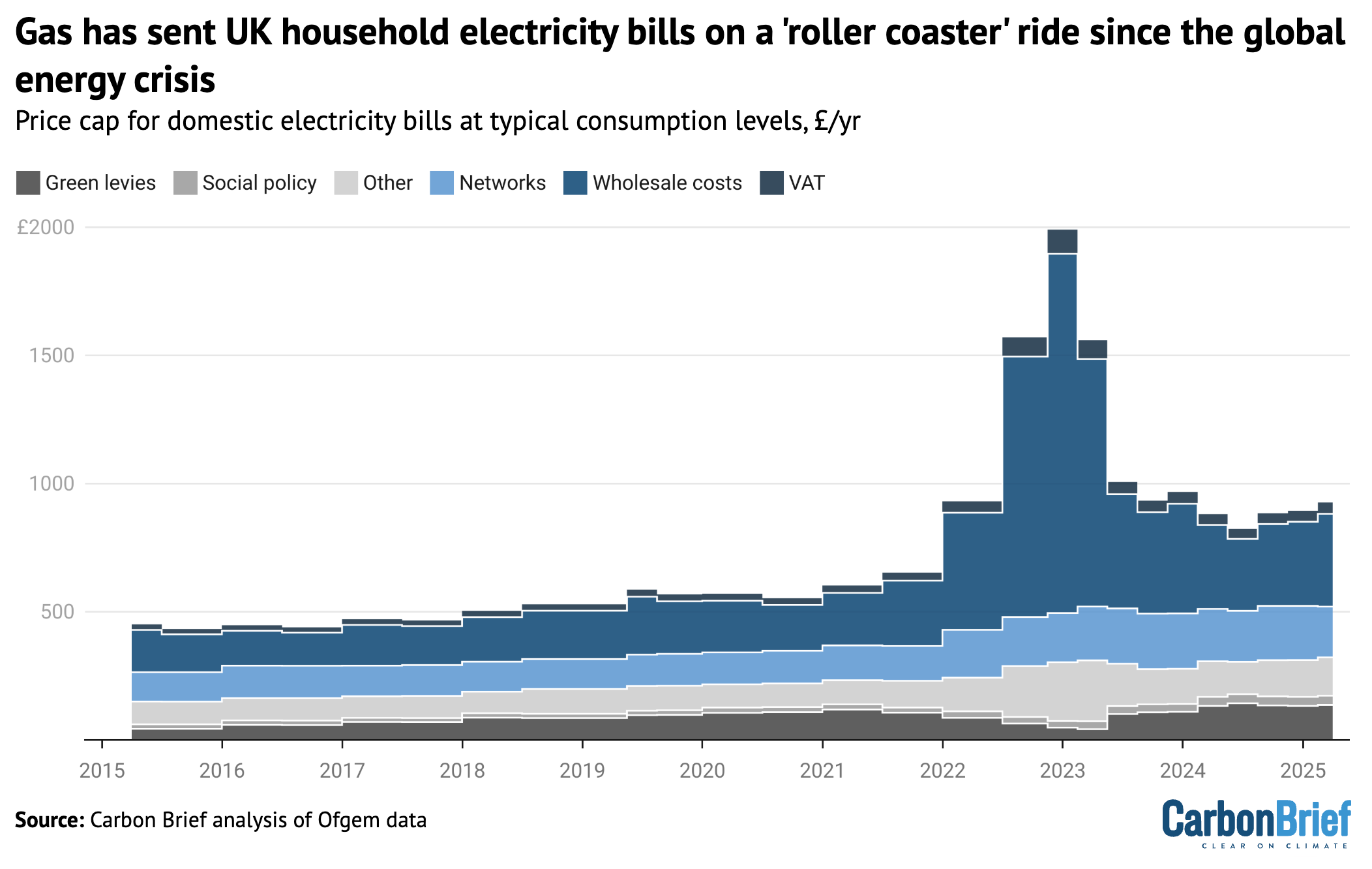

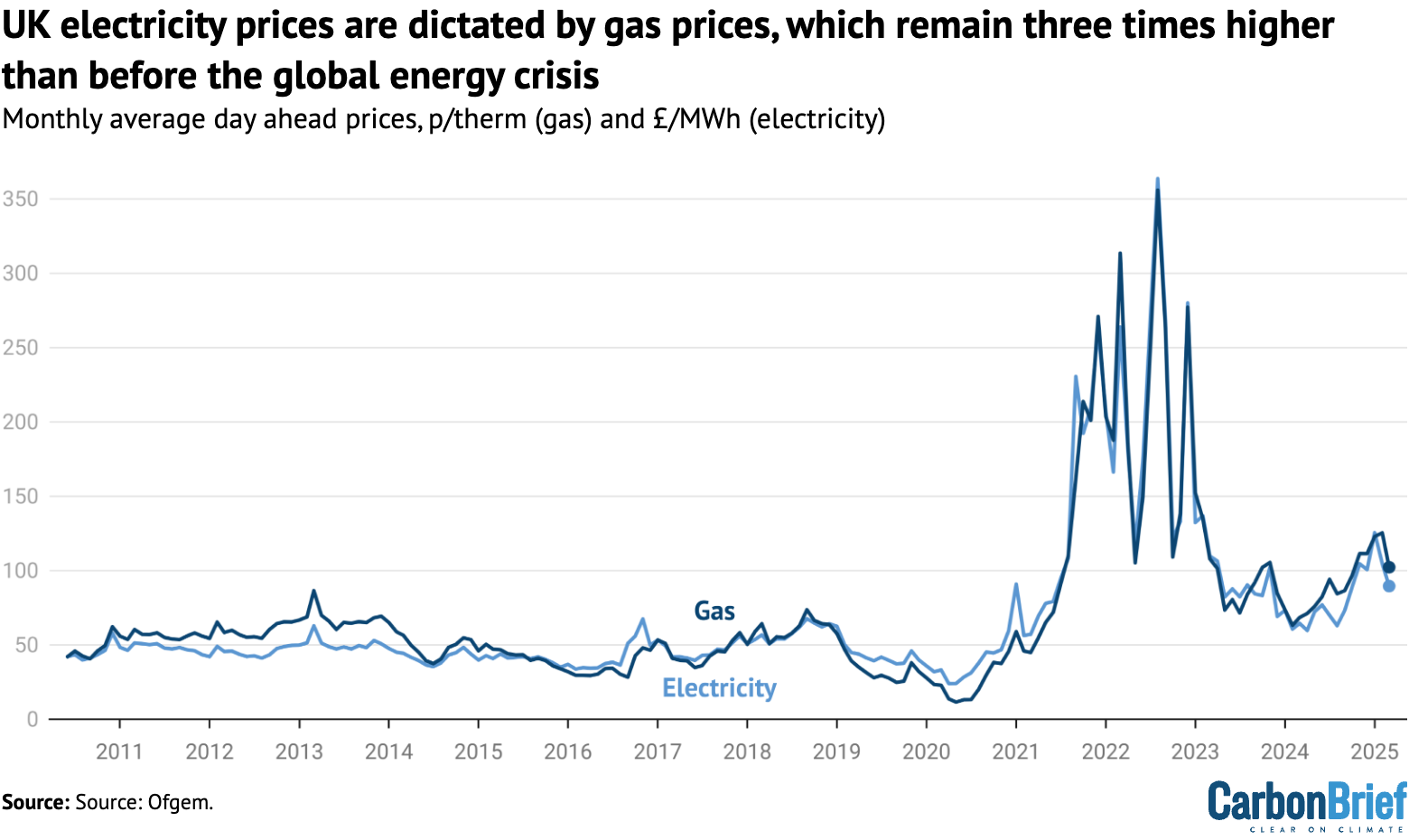

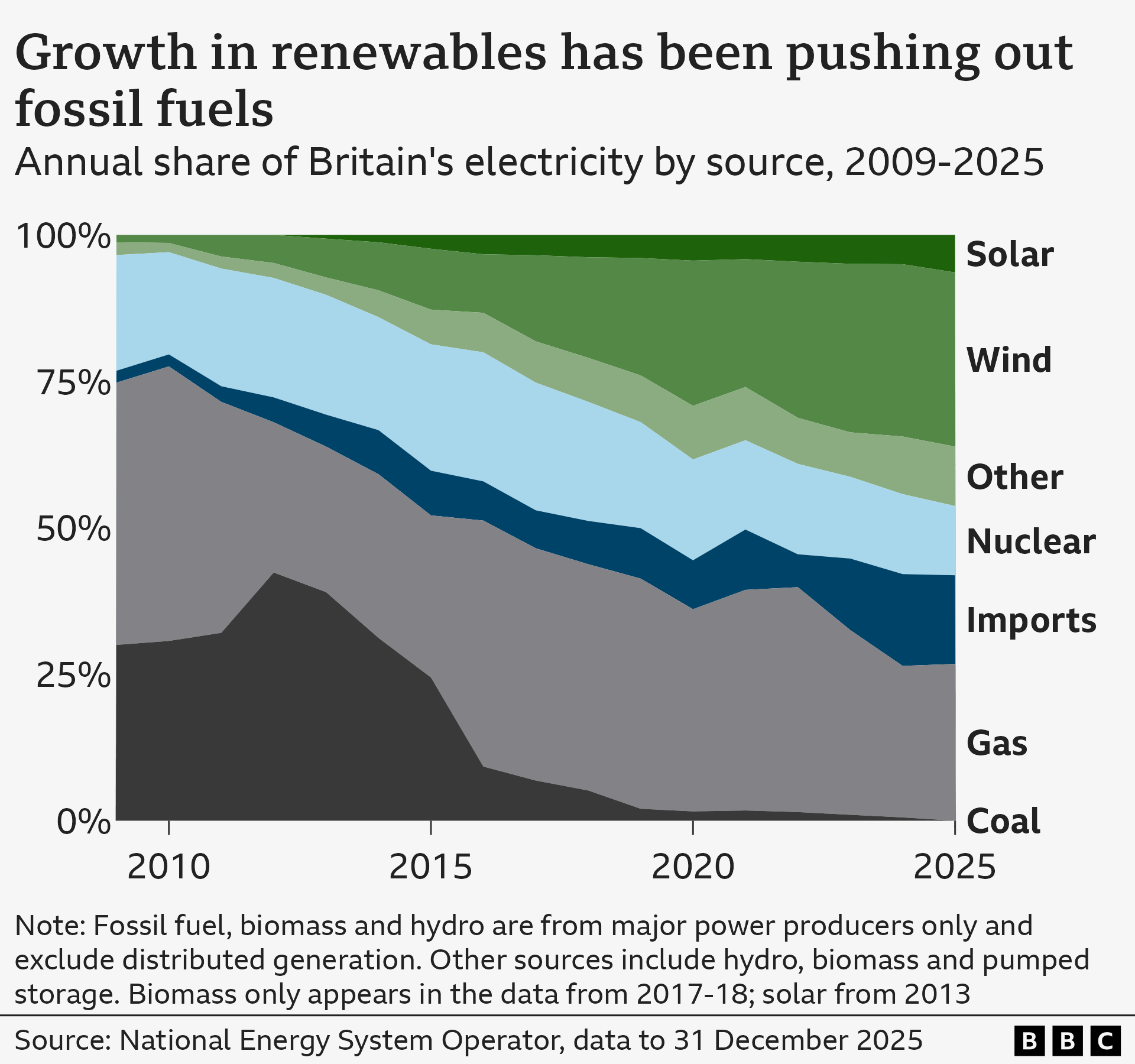

The UK's wholesale electricity market operates on a marginal pricing model, meaning the most expensive generator needed to meet demand at any given moment sets the price for all electricity sold in that half-hour period. Because gas-fired power plants are frequently the marginal generator, especially during peak demand or when wind output is low, the price of gas effectively dictates the price of electricity across the entire system. This creates a structural distortion: when gas prices spiked to over 300p per therm in 2022, electricity prices surged even for households with solar panels or wind farms on their grid. The mechanism means that approximately 40% of the average household electricity bill is directly tied to gas costs, even though gas accounts for only about 35% of the generation mix. Reeves's plan would replace this with a "split market" or "clearing price" model, where electricity from renewables and nuclear is priced at its own lower cost, while gas-fired generation is compensated separately. The Treasury is consulting on two design options: a "green power pool" that auctions low-carbon electricity at a fixed price, and a "decoupled marginal pricing" model that pays gas plants only their actual costs. Both approaches require significant changes to the balancing mechanism and settlement systems operated by National Grid ESO. The reform is the most direct challenge to the UK's marginal pricing orthodoxy since the 2013 Electricity Market Reform, and it arrives as energy costs remain a top voter concern heading into the next general election.

Where the £150–£200 in annual savings comes from

The projected household savings of £150 to £200 per year are derived from the difference between the current marginal price and the weighted average cost of the generation mix. Under the current system, when gas is the marginal generator at £100 per MWh, all electricity, including wind at £40 per MWh, is sold at £100 per MWh. Decoupling would mean wind and nuclear sell at their own lower prices, while gas plants receive only their actual cost. For a typical household consuming 2,900 kWh of electricity annually, the savings represent a reduction of roughly 15% to 18% on the electricity portion of the bill. The Treasury's modelling assumes that renewable generation will continue to grow, meaning the gap between the marginal gas price and the average low-carbon price will widen over time. However, the actual savings depend on the speed of the transition, the level of gas prices, and how generators adjust their bidding strategies. Critics argue that if gas plants are compensated for lost revenue through a capacity mechanism, the net savings will be lower. The Office for Budget Responsibility has not yet scored the policy, but the Treasury expects the reform to be fiscally neutral because lower consumer bills will reduce the need for the Energy Price Guarantee and other support schemes.

Which energy companies gain and lose in the reshuffle

The biggest winners from decoupling are renewable generators, including Ørsted, SSE, and RWE, which currently sell wind power at the gas-linked marginal price and capture windfall profits during high-gas periods. Under the new model, these companies would receive a lower price for their output, but they would gain long-term revenue certainty through the proposed green power pool contracts. The biggest losers are gas-fired generators such as Uniper, Drax, and Centrica's gas fleet, which would lose the infra-marginal rent they currently earn when gas is not the marginal generator. Drax's biomass units, which receive subsidies under the Renewables Obligation, face an uncertain future because the reform could alter the subsidy calculation. The big six retail suppliers, including British Gas, EDF, E.ON, Scottish Power, OVO, and Octopus Energy, face a transitional challenge: their hedging strategies and retail tariffs are built around the current marginal pricing model. Octopus, which has aggressively marketed smart tariffs and time-of-use pricing, is best positioned to adapt because its technology platform can handle dynamic pricing. The reform also creates an opening for new entrants offering fixed-price renewable tariffs backed by power purchase agreements, a model already common in the Nordic markets. The Competition and Markets Authority will need to approve the market design changes, and the Big Six are expected to lobby hard against any model that reduces their trading margins.

Downstream effects on renewable investment, grid capacity, and industrial users

The decoupling plan sends a powerful signal to renewable project financiers: the days of selling wind power at gas-linked prices are numbered, which will force a recalibration of project economics. Offshore wind developers such as Orsted and Vattenfall, which bid into the Contracts for Difference auctions at strike prices around £40–£50 per MWh, will need to reassess their revenue models because the CfD reference price will no longer be the wholesale market price. This will push strike prices higher in future auctions, increasing the cost of the government's renewable subsidy scheme. On the grid side, the reform increases the value of battery storage and demand-side response, because these technologies profit from price arbitrage between high- and low-price periods. National Grid will need to upgrade its settlement systems to handle dual pricing, a multi-year IT project that the Treasury estimates will cost £200 million to £300 million. For industrial users, the reform is a double-edged sword: large electricity consumers like steelmakers and data centres will see lower power costs, but the loss of gas-price hedging opportunities will increase their exposure to gas price volatility. The British Steel industry, which pays some of the highest electricity prices in Europe, stands to benefit most. The reform also creates a new regulatory challenge for Ofgem, which must design a transition mechanism that prevents generators from gaming the system by withholding capacity to manipulate prices.

The policy signal and what it means for the UK's net zero trajectory

Reeves's announcement is as much a political statement as an economic reform: it signals that the Treasury is willing to override decades of market orthodoxy to deliver tangible consumer benefits. The marginal pricing model has been a sacred cow of UK energy policy since the 1990s, defended by economists who argue it ensures efficient dispatch. By breaking that link, Reeves is implicitly acknowledging that the model fails when gas prices are structurally high, and that the consumer burden of net zero must be redistributed. The reform aligns with Labour's broader strategy of using state intervention to lower the cost of decarbonisation, following the creation of Great British Energy and the national wealth fund. It also puts pressure on the European Commission, which is considering similar reforms to the EU's marginal pricing model under the Electricity Market Design review. The UK's move will accelerate that process, creating a de facto race between London and Brussels to deliver lower electricity prices. However, the reform carries execution risk: if the transition is poorly managed, it will deter investment in new gas peaking plants needed for grid reliability, forcing the government to extend the life of coal plants or pay higher capacity payments. The Treasury is targeting implementation by 2028, but the timeline depends on parliamentary time, Ofgem's capacity, and the outcome of the consultation. For investors, the message is clear: the UK energy market is entering a period of structural change that will reshape revenue models, asset valuations, and competitive dynamics for the next decade.

The decoupling plan is the most consequential energy market reform in a generation, but its success hinges on execution details that are yet to be written. The Treasury's consultation will need to resolve several thorny design questions: how to compensate gas plants for lost infra-marginal rent without creating a new subsidy regime; how to ensure renewable generators still have incentives to invest in new capacity; and how to prevent the reform from increasing system costs through higher balancing payments. The political calculus is equally delicate: if the reform delivers the promised £150–£200 savings, it will be a powerful electoral asset for Labour. If it fails to materialise or drives up costs for industrial users, it will become a liability. The City of London, which has been pushing for e-gate access for UK travellers at Swiss airports and other trade facilitation measures, will be watching closely because the reform signals a more interventionist Treasury approach to market design. For now, the direction of travel is clear: the UK is moving away from a gas-indexed electricity market toward a system that prices low-carbon power at its true cost. The next two years will determine whether that transition is smooth or chaotic, and whether the promised savings reach consumers or get absorbed by the complexities of implementation.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.