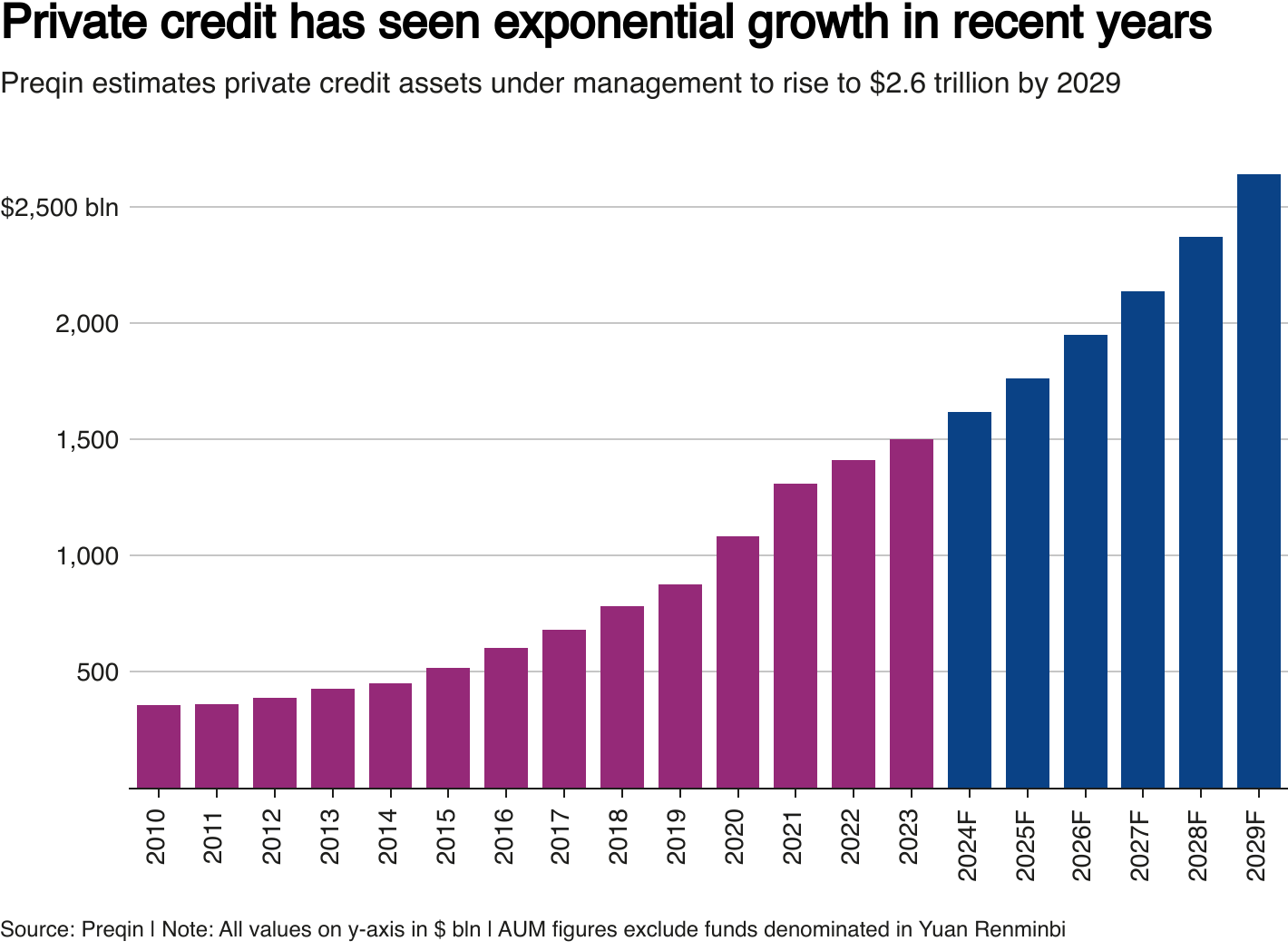

Wall Street has spent the better part of a decade helping private credit become respectable. Banks financed the lenders. Private equity sponsors fed them deals. Insurance groups and wealth platforms sold the income story to clients who wanted yield without daily volatility. The pitch worked because private credit seemed to offer the best part of leverage with fewer of the visual cues that usually frighten investors. Prices did not flash across a screen every second. Marks moved slowly. Defaults were manageable. Direct lenders could say, with some truth, that they were serving companies the syndicated market no longer wanted to handle. That framework is now under strain. Reuters reported eight days ago, citing the Financial Times, that Wall Street banks had started trading derivatives tied to private-credit risk. The Financial Times separately reported on March 11 that JPMorgan had marked down loan portfolios linked to private-credit groups. Reuters then reported on March 30 that Federal Reserve chair Jerome Powell said the central bank was watching private credit for signs of trouble, and Reuters added fifteen days ago that the Fed had asked major U.S. banks about their exposure to private-credit firms, according to Bloomberg. Put together, those are not random developments. They amount to a sequence: marks move first, supervisors ask second, and traders build protection third. The most important change is not that private credit has suddenly become fragile. It is that the biggest institutions in finance have stopped pretending the sector can remain opaque and systemically peripheral at the same time.

JPMorgan's Markdowns Turn a Private Asset Into a Daily Risk Question

The March 11 Financial Times report on JPMorgan's markdowns gave traders a visible stress signal inside an otherwise slow-marking market.

For years, private credit enjoyed a structural advantage over public markets: it looked calmer because it was measured less often. A broadly syndicated loan can trade down in real time when recession fears rise or an issuer disappoints. A private loan can sit at a value that changes only when a lender or financing counterparty is forced to confront new evidence. That difference helped the sector project stability, but it also meant that confidence depended on large institutions continuing to accept lagged marks as credible. Once JPMorgan marked down loan portfolios linked to private-credit firms, according to the Financial Times, the conversation changed. A markdown by a major bank does not just reduce the carrying value of one book. It tells the market that private-credit exposure has become something treasury desks, risk committees and financing teams need to debate in public-market terms.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.