JPMorgan has issued a stark warning for Tether: the world's largest stablecoin issuer will be forced to liquidate its bitcoin holdings if the United States enacts new stablecoin legislation. The prediction comes as the SEC and CFTC intensify discussions on a regulatory framework that would impose stricter reserve requirements on stablecoin issuers. Tether, which holds billions of dollars in bitcoin as part of its reserve portfolio, will face a direct conflict with proposed rules requiring that stablecoin reserves be composed entirely of cash, cash equivalents, or short-duration Treasuries. The JPMorgan note argues that Tether's bitcoin stash, accumulated over years of aggressive buying, is a strategic asset that also creates a regulatory liability. If the legislation passes, Tether will need to unwind those positions or restructure its business to avoid violating the new rules. This matters now because the stablecoin market, with a total supply exceeding $200 billion, sits at the center of the US regulatory debate, and any forced selling by Tether will ripple through both the crypto and traditional finance systems.

Where the $570M bitcoin reserve becomes a regulatory liability

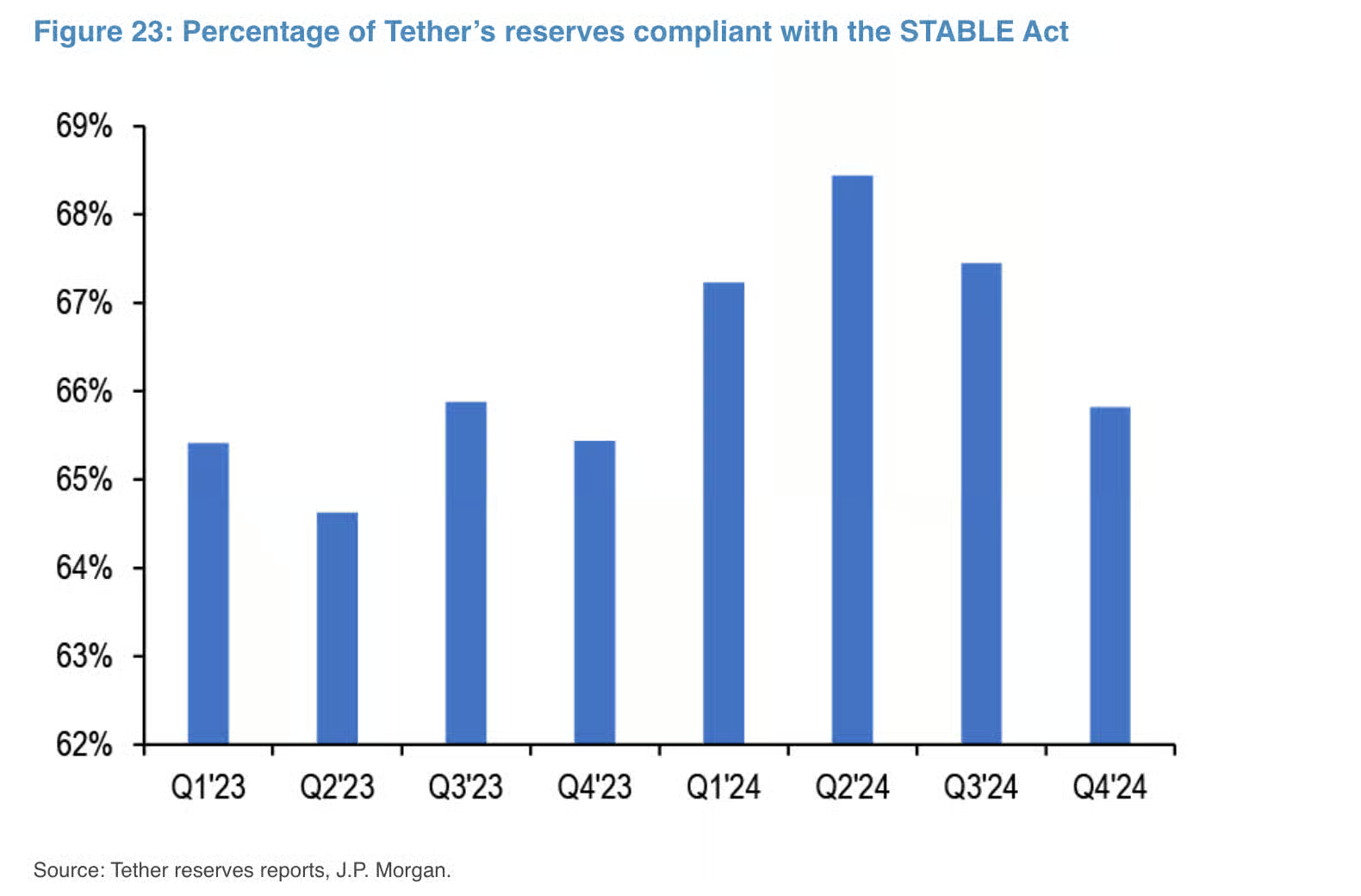

Tether's balance sheet has long been a source of controversy, but the JPMorgan analysis zeroes in on a specific structural tension: the company's bitcoin holdings, valued at approximately $570 million as of the most recent public attestation, are not cash equivalents under any standard accounting definition. The proposed US stablecoin legislation, which the SEC and CFTC are actively shaping, will require that every dollar of stablecoins in circulation be backed by assets that can be redeemed at par within one business day. Bitcoin, with its 24/7 trading but extreme price volatility, fails that test entirely. JPMorgan's analysts calculate that Tether will need to either sell its entire bitcoin position or carve it into a separate investment vehicle not commingled with the stablecoin reserve. The mechanism is straightforward: the legislation will mandate that stablecoin issuers maintain a 1:1 reserve ratio with only highly liquid, low-risk assets. Tether's current reserve composition, which includes bitcoin, commercial paper, and secured loans, will not meet that standard. The company will need to divest roughly $570 million in bitcoin. A sale of that size, if executed in a short window, will exert significant downward pressure on the market. Tether's bitcoin holdings represent roughly 0.7% of its total $86 billion reserve pool, yet the regulatory risk they carry is disproportionate to their size.

How the forced sale flows through Tether's profit and loss

Tether generates the bulk of its revenue from the interest income on its reserve assets, primarily US Treasuries. Bitcoin, by contrast, produces no yield and carries a holding cost in the form of price risk and custody fees. JPMorgan's analysis shows that Tether's bitcoin position, while a small fraction of its total $86 billion reserve pool, has historically been a drag on the company's earnings relative to a pure Treasury portfolio. If Tether sells its bitcoin, the immediate P&L impact depends on the sale price relative to its cost basis. Tether has not disclosed its average purchase price for bitcoin, but public on-chain data indicates the company accumulated the position during the 2023–2024 bull market, when bitcoin traded between $25,000 and $70,000. A forced sale at current levels around $65,000 will likely result in a modest gain or loss, but the opportunity cost is significant. Tether will lose the optionality of bitcoin appreciation, which has been a key narrative for the company's supporters. More importantly, the sale will free up capital that Tether can redeploy into Treasuries, generating a predictable 4–5% yield. JPMorgan estimates that shifting $570 million from bitcoin to Treasuries will add roughly $25 million in annual interest income to Tether's bottom line. That is a small but meaningful boost to a company that reported $6.2 billion in profits in 2024. The net effect is a cleaner balance sheet that yields a higher, more predictable return.

The competitive reshuffle: Circle, Paxos, and the new regulatory moat

The JPMorgan note positions Tether's potential bitcoin sale as a competitive inflection point for the stablecoin market. Circle, the issuer of USDC, has long maintained a reserve policy that aligns closely with the proposed US legislation. Its reserves are 100% cash and short-duration Treasuries, with no exposure to bitcoin, commercial paper, or corporate bonds. If the new rules pass, Circle's compliance burden will be near zero, while Tether faces a costly restructuring. Paxos, which issues the Binance-backed BUSD and its own USDP, similarly operates with a conservative reserve policy. JPMorgan argues that the legislation will effectively codify Circle's and Paxos's existing practices as the industry standard, creating a regulatory moat that disadvantages Tether. The competitive dynamics extend beyond reserve composition: Tether's dominance in the stablecoin market, with a 60% market share versus USDC's 25%, has been built on its willingness to accept higher risk and offer less transparency. The new rules will force Tether to match Circle's transparency and reserve standards, erasing one of its key competitive advantages. Smaller issuers like Cryptex Finance, which operates in the DeFi space, will also face compliance costs, but their smaller scale and more limited reserve pools make adaptation easier. Unlike Tether, which must liquidate a multi-hundred-million-dollar bitcoin position, smaller DeFi-native issuers can restructure their collateral baskets within weeks rather than months, giving them a tactical speed advantage during the transition period. The net effect is a market that favors incumbents with clean balance sheets and punishes those with opaque or risky reserve assets.

Downstream effects on exchanges, DeFi, and the bitcoin market

A Tether bitcoin sale of $570 million will not occur in a vacuum. It will cascade through multiple layers of the crypto ecosystem. The most immediate downstream effect will be on centralized exchanges that rely on Tether as their primary quote currency. Binance, OKX, and Kraken all list USDT as their dominant trading pair, and a forced sale will likely trigger a temporary liquidity crunch in the USDT-BTC market. JPMorgan's trading desk estimates that a $570 million sell order, if executed over a week, will push bitcoin prices down by 3–5%, assuming normal market depth. The DeFi ecosystem will also feel the impact: Tether is the largest collateral asset in lending protocols like Aave and Compound, with over $3 billion in USDT deposited across Ethereum-based DeFi. If Tether's reserve quality is called into question, depositors may withdraw USDT en masse, creating a liquidity crisis in those protocols. The downstream effect on enterprise buyers is more nuanced. Companies like MicroStrategy and Tesla, which hold bitcoin on their balance sheets, will see the value of their holdings decline temporarily, but the forced sale will also create a buying opportunity for institutional investors who have been waiting for a dip. LMAX Digital, the institutional crypto exchange, has reported increased interest from hedge funds and asset managers in buying bitcoin at discounted prices, showing that the sell-side pressure from Tether will be met by strong buy-side demand. The SEC's DeFi roundtable discussions, which Chris Perkins attended as a CFTC advisory committee member, signal that DeFi protocols themselves will face similar reserve requirements in a future regulatory iteration, potentially within the next 18 to 24 months. That forward-looking risk has already prompted major DeFi lending platforms to begin contingency planning for a world where USDT is no longer the default collateral of choice, with protocols that have diversified toward USDC and fully-backed alternatives better positioned to absorb the shift.

The policy signal: what Tether's bitcoin sale says about the future of crypto regulation

JPMorgan's prediction is not just a financial analysis. It is a reading of the regulatory trajectory in Washington. The SEC and CFTC have been engaged in a turf war over crypto oversight, but the stablecoin legislation represents a rare area of bipartisan agreement. Both agencies recognize that stablecoins, if properly regulated, can strengthen the dollar's dominance in digital payments. The proposed rules are designed to eliminate the risk of a stablecoin run, which could destabilize the broader financial system. Tether's bitcoin sale, if it occurs, will be a signal that the US is serious about enforcing reserve standards and that no company, regardless of size, is exempt. CoinFund President Chris Perkins, a member of the CFTC's Global Market Advisory Committee, has noted that the inter-agency cooperation on stablecoins is unprecedented and signals a shift toward comprehensive regulation. The policy signal extends beyond stablecoins: if the US can successfully regulate the $200 billion stablecoin market, it will set a precedent for regulating other crypto assets, including bitcoin and ether. The JPMorgan note concludes that Tether's bitcoin sale will be a watershed moment, marking the end of the unregulated stablecoin era and the beginning of a new phase where compliance is the primary competitive differentiator.

The broader implication is that Tether's bitcoin holdings, once seen as a bold bet on crypto's future, have become a liability in a world where regulators demand clarity and safety. The company's CEO, Paolo Ardoino, has publicly resisted calls to divest, arguing that bitcoin is a legitimate reserve asset. But the JPMorgan analysis shows that resistance is futile: the legislative momentum is too strong, and the political will to act is too deep. If the bill passes, Tether will have no choice but to sell. The question is not whether the sale will happen, but when and at what price. For the crypto market, the answer will determine whether the transition to a regulated stablecoin regime is orderly or chaotic. For Tether, it will determine whether the company can survive the transition as the market leader or cede ground to more compliant competitors. The next six months will be decisive, as the SEC and CFTC finalize their proposals and Congress prepares to vote. Investors should watch the legislative calendar closely. The date of the vote will be the date the bitcoin market reprices Tether's exposure.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.