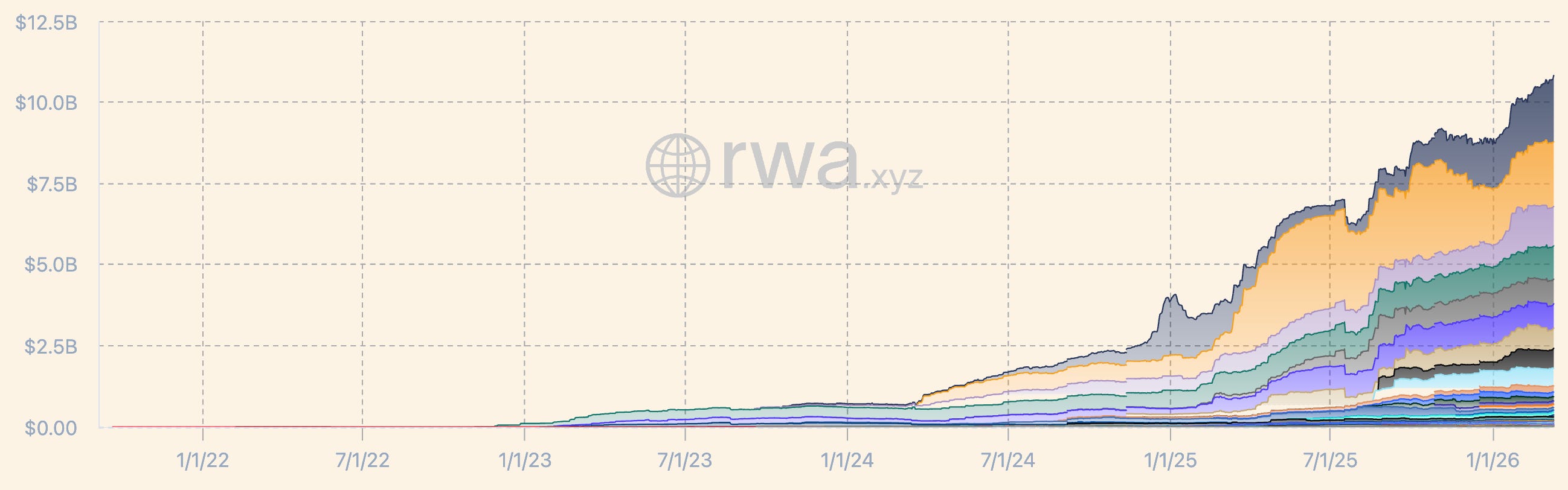

Standard Chartered projects that tokenized real-world assets will reach $2 trillion by 2028, a forecast that underscores the structural shift underway in global finance even as the broader decentralized finance sector contends with a $55 billion decline in total value locked since October. The bank’s prediction, driven by the stablecoin boom and institutional appetite for on-chain credit products, arrives as the US Senate Banking Committee prepares to vote Thursday on the Clarity Act, a bill that would impose stablecoin reward restrictions and attach the Blockchain Regulatory Certainty Act clarifying that non-custodial developers are not money transmitters. Meanwhile, the UK is proposing a “no gain, no loss” tax rule for DeFi, a major policy win for users. The convergence of these forces (a bullish tokenization forecast, regulatory clarity in two major jurisdictions, and a DeFi sector that is deleveraging but not retreating) signals that the crypto credit cycle is maturing into something more durable than the speculative frenzy of prior years. This matters because the infrastructure being built now, from tokenized Treasuries to decentralized lending protocols, will determine whether the next bull run is built on real economic activity or another round of leveraged speculation.

The Stablecoin Boom Behind Standard Chartered’s $2 Trillion Forecast

Standard Chartered’s $2 trillion projection for tokenized real-world assets by 2028 is rooted in the explosive growth of stablecoins, which provide the on-ramp for institutional capital to move onto blockchain rails. The bank sees tokenized versions of bonds, private credit, real estate, and commodities becoming a core asset class for asset managers and corporate treasuries, with stablecoins acting as the settlement layer. This is not a speculative forecast; it reflects actual deployment patterns. Market maker Flowdesk reports that crypto credit is finding a fragile balance, with DeFi lenders deleveraging but not retreating from the market. The Maple protocol, which facilitates institutional lending on-chain, has seen steady demand from borrowers seeking yield in a higher-rate environment. The $2 trillion figure also assumes that regulatory frameworks in the US and UK will provide legal certainty for tokenization, which is precisely what the Clarity Act and the UK’s proposed tax treatment aim to deliver. Standard Chartered itself has been an active participant in the tokenization space, having issued a $50 million tokenized bond on the Ethereum blockchain in 2024. The bank’s forecast is therefore a bet on its own business model as much as a market prediction. If realized, tokenized assets would represent roughly 2% of global GDP by 2028, a share that would force every major bank and asset manager to build or buy tokenization capabilities. The bank’s analysts have modeled this growth using on-chain data from stablecoin supply, which has expanded by 40% year-over-year, and institutional custody inflows tracked by Coinbase and BitGo. These metrics provide a concrete foundation for the $2 trillion figure, grounding it in observable capital flows rather than abstract projections.

How the $55 Billion TVL Decline Masks Structural Strength

The $55 billion decline in total value locked across DeFi protocols since October 2025 is significant but not catastrophic, and the sector’s resilience tells a more important story about its underlying health. Bitcoin and ether have tanked during this period, yet DeFi investors have refused to panic, with TVL slipping only modestly relative to the price declines of the underlying assets. This is because the composition of TVL has shifted away from speculative liquidity mining toward genuine lending and borrowing activity. DEX volumes have actually risen during the downturn, as traders seek efficient execution without counterparty risk. The JitoSOL liquid staking token, for example, has maintained its peg and continued to attract deposits even as Solana’s price fell. Flowdesk notes that DeFi lenders are deleveraging, reducing loan-to-value ratios and tightening collateral requirements, but they are not retreating from the market. This is a sign of maturity: protocols are managing risk proactively rather than relying on liquidations to correct imbalances. The $55 billion figure also masks the fact that the decline is concentrated in a handful of over-leveraged protocols that were already vulnerable. The core lending markets on Aave and Compound have remained stable, with utilization rates hovering around 70%. The structural strength of DeFi is further evidenced by the fact that no major protocol has suffered a catastrophic exploit during this drawdown, a stark contrast to the 2022 bear market. Data from DefiLlama confirms that the number of active DeFi wallets has held steady at 5 million, indicating that user engagement has not collapsed alongside TVL.

Competitive Reshuffle: Coinbase, Banks, and the Stablecoin Reward Fight

The Clarity Act vote has exposed a deepening rift between incumbent financial institutions and the crypto-native industry, with Coinbase walking away from the bill over concerns about stablecoin yield restrictions. The American Bankers Association has slammed the compromise language, arguing that loopholes in the stablecoin reward restrictions will allow non-bank issuers to continue offering yields that banks cannot match. This puts Coinbase in a difficult position: the exchange needs regulatory clarity to expand its stablecoin business, but it cannot accept a bill that would cap the yields on its USDC holdings. The Blockchain Regulatory Certainty Act, which is attached to the Clarity Act, clarifies that non-custodial software developers are not money transmitters, a provision that benefits decentralized protocols like Uniswap and Aave. This creates a competitive dynamic where banks get stricter oversight on stablecoins while DeFi developers get a regulatory safe harbor. The UK’s proposed “no gain, no loss” tax rule for DeFi further tilts the playing field toward decentralized protocols, as it removes the tax friction that currently discourages users from participating in lending and staking. The net effect is a regulatory landscape that favors established DeFi protocols over both traditional banks and newer, less capitalized entrants. Flowdesk expects this to accelerate consolidation, with the top five DeFi lending protocols capturing an increasing share of TVL as smaller competitors struggle with compliance costs. The stablecoin reward fight has also drawn in the Treasury Department, which has signaled concern that unregulated yields could destabilize money markets.

Downstream Effects on Hyperscalers, Fabs, and Enterprise Buyers

The tokenization boom and DeFi resilience have second-order effects that ripple through the broader technology and financial infrastructure ecosystem. Hyperscalers like Amazon Web Services and Google Cloud are already positioning to capture the compute demand from tokenization platforms, which require high-throughput blockchain nodes, off-chain data oracles, and zero-knowledge proof verification. Standard Chartered’s $2 trillion forecast implies a massive increase in on-chain transaction volume, which will drive demand for cloud services from firms like Coinbase Cloud and Alchemy. On the hardware side, the sustained DeFi activity supports demand for high-performance GPUs used in proof-of-stake validation and MEV extraction, though the shift to proof-of-stake has reduced the energy intensity of blockchain operations. Enterprise buyers, particularly asset managers and corporate treasuries, are the primary beneficiaries of tokenization, as it reduces settlement times from T+2 to near-instantaneous and lowers custody costs. The UK’s tax proposal is a direct signal to these buyers that the government wants them to participate in DeFi. However, the regulatory uncertainty in the US, exemplified by the Clarity Act debate, is causing some enterprise buyers to delay tokenization projects until the legal framework is settled. The Blockchain Regulatory Certainty Act helps by clarifying that developers are not money transmitters, but it does not address the classification of tokenized securities, which remains the biggest barrier to institutional adoption. BlackRock and Fidelity have both launched tokenized money market funds, and their success will depend on whether regulators treat these products as securities or commodities.

Policy Signal: What the Clarity Act and UK Tax Rule Tell Us About the Future

The Clarity Act vote and the UK’s proposed tax treatment of DeFi represent a fork in the road for global crypto regulation. The US approach, embodied by the Clarity Act, is to impose restrictions on stablecoin rewards while providing clarity for non-custodial developers. This reflects a compromise between the banking lobby, which wants to limit competition from stablecoin yields, and the crypto industry, which wants legal certainty for DeFi protocols. The fact that Coinbase walked away from the bill suggests that the compromise is unstable, and the debate over ethics language will be deferred to the Senate floor. The UK, by contrast, is taking a more permissive approach with its “no gain, no loss” tax rule, which treats DeFi transactions as disposals only when assets are actually sold. This creates a clear competitive advantage for UK-based DeFi protocols and tokenization platforms. The divergence between the two regulatory regimes will drive a geographic shift in crypto activity, with developers and capital flowing to jurisdictions with clearer rules. Standard Chartered’s $2 trillion forecast implicitly assumes that the US will eventually align with the UK’s approach, but the Clarity Act vote shows that the path to that alignment is fraught with political obstacles. The Blockchain Regulatory Certainty Act, if passed, would be a significant step forward, but it addresses only one piece of the puzzle. The broader signal is that regulators are beginning to treat DeFi as a permanent feature of the financial system, not a temporary anomaly. The UK Treasury has already begun consulting on a broader crypto asset framework, and the European Union’s MiCA regulation is set to take full effect in 2027, creating a three-way regulatory competition.

The next 12 months will determine whether the tokenization forecast becomes a self-fulfilling prophecy or a missed opportunity. Standard Chartered’s $2 trillion target depends on the passage of the Clarity Act and the implementation of the UK’s tax rule, both of which are within reach but not guaranteed. If the US Senate fails to pass the bill, or if the stablecoin reward restrictions prove too onerous, the tokenization boom will shift to London and Singapore, leaving American banks and asset managers at a competitive disadvantage. The DeFi sector, meanwhile, will continue to mature, with TVL likely to recover as the market stabilizes and new use cases emerge in tokenized credit and real-world assets. The AI threat identified by Anthropic, specifically that automated exploits are becoming viable, is a real risk, but it also catalyzes better security practices and insurance products. The most likely outcome is a bifurcated market: regulated tokenization for institutional investors and permissionless DeFi for retail users, with the two worlds connected by stablecoins and compliant bridges. The $2 trillion figure is ambitious but plausible, and it will be the benchmark against which the industry measures its progress.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.