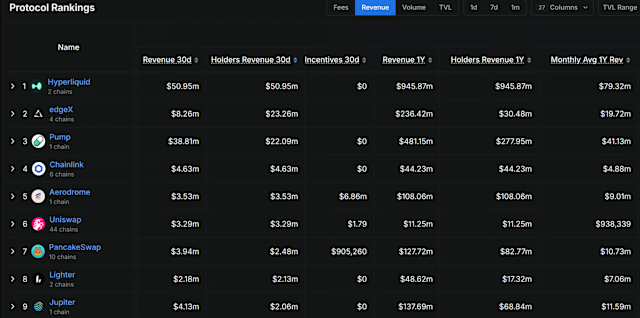

Three decentralized finance platforms, Hyperliquid, EdgeX, and Pump.fun, returned a combined $96.3 million to token holders over the past 30 days, a sum that underscores how quickly DeFi is transitioning from a speculative sideshow into a revenue-generating financial layer. Hyperliquid alone distributed $50.95 million, every dollar of its gross revenue, with zero incentives or token inflation. Pump.fun returned $22.09 million of its $38.81 million in total revenue. The numbers are not theoretical. They represent real fee income from users trading perpetuals, swapping tokens, and minting memecoins. Across the broader ecosystem, stablecoins now command a $320 billion market cap, decentralized exchanges process $160 billion in monthly spot volume, perpetual DEXs handle $540 billion, and lending protocols carry $28 billion in active loans. DeFi is no longer a niche experiment. It is becoming the backend for the onchain economy, and the revenue numbers prove that the business model works.

Hyperliquid Leads with $50.95M in Distributions

Hyperliquid accounted for more than half of the total distributions, returning $50.95 million in revenue to its token holders over the 30-day window. The platform operates a perpetual futures exchange that competes directly with centralized venues like Binance and Bybit, but does so entirely onchain. Its revenue is generated from trading fees, and the protocol returns every dollar of that fee income to holders of its native token. No portion is reserved for team compensation, marketing, or protocol reserves. That zero-retention model is rare in crypto, where most protocols keep a substantial share of revenue for operations or treasury accumulation. Pump.fun, the memecoin launchpad, returned $22.09 million of its $38.81 million in revenue, retaining roughly 43% for platform costs. EdgeX, a smaller perpetual DEX, contributed the remainder. The combined $96.3 million figure is not a one-off quarter. It is a monthly run rate. If sustained, these three platforms alone would return over $1.15 billion to holders annually, a scale that begins to rival the dividend payouts of mid-cap fintech companies. The revenue distribution model is attracting attention from institutional investors who previously dismissed DeFi as a zero-sum game of token speculation.

Revenue Mechanics: Fees, Buybacks, and Staking Rewards

The revenue mechanics are straightforward but powerful. Each platform charges fees on user activity: Hyperliquid on perpetual trades, Pump.fun on token launches and swaps, EdgeX on its own perpetual order book. Those fees accumulate in protocol treasuries, and the protocols then distribute the cash directly to token holders, typically through buybacks or direct staking rewards. For Hyperliquid, the $50.95 million monthly revenue implies an annualized run rate of roughly $611 million. At a conservative 20x multiple on revenue, the standard benchmark for high-growth fintech, that would imply a token valuation north of $12 billion, though token prices rarely track traditional equity multiples cleanly. The key insight is that these distributions create a genuine yield for holders, unlike the inflationary staking rewards that dominated the 2021 bull market. Andre Cronje, the Fantom founder, recently described DeFi as "becoming the backend for the onchain economy," and the revenue data supports that framing. These are not subsidized protocols burning venture capital. They are self-sustaining businesses generating real fee income from real user activity. The transparency of onchain accounting allows anyone to verify the revenue figures in real time, eliminating the trust assumptions that plague traditional finance.

Competitive Reshuffle: Hyperliquid Gains on dYdX and GMX

Hyperliquid's dominance in perpetual DEX revenue is reshaping the competitive landscape. Traditional decentralized perp platforms like dYdX and GMX now face a clear challenger that is capturing both volume and mindshare. Hyperliquid's zero-retention model creates a powerful incentive for token holders to accumulate and stake, which in turn drives liquidity and trading volume on the platform. Pump.fun's $22.09 million in returned revenue places it ahead of established DEXs like PancakeSwap and Yearn.Finance in terms of direct holder distributions, at least on a monthly basis. The memecoin launchpad has effectively commoditized token creation, and its fee revenue reflects the sheer volume of activity on its platform. EdgeX, while smaller, benefits from the same structural tailwind: users want exposure to perpetual trading without leaving the onchain environment. The losers in this reshuffle are centralized exchanges that rely on opaque fee structures and zero revenue sharing with users. Binance, Bybit, and OKX generate billions in quarterly trading fees but return none of that to their token holders. As DeFi protocols demonstrate that onchain revenue sharing works at scale, the pressure on centralized incumbents to adopt similar models will intensify. The competitive dynamics are forcing centralized exchanges to reconsider their fee structures and tokenomics.

dYdX recently adjusted its fee schedule after Hyperliquid's volume growth became impossible to ignore, and GMX, which pioneered the model of directing 70% of protocol fees to liquidity providers, has seen its market share erode as Hyperliquid's fully onchain order book offers tighter spreads and near-instant settlement. The distinction matters for institutional participants: a platform that distributes 100% of revenue eliminates the principal-agent conflict inherent in centralized fee retention. Volume follows liquidity, and liquidity follows yield. The $540 billion in monthly perpetual DEX volume is not concentrated on a single venue, but Hyperliquid's share is growing quarter over quarter, and its zero-retention model is the primary driver. Centralized venues that have historically competed on brand, fiat on-ramps, and customer support now face a structural disadvantage against a protocol with a transparent, verifiable revenue-sharing track record.

Infrastructure Ripple Effects: Stablecoins, Lending, and Blockspace

The revenue numbers ripple through the broader DeFi infrastructure stack. Stablecoin issuers Tether and Circle benefit directly because Hyperliquid, Pump.fun, and EdgeX all settle trades in USDC and USDT. The $320 billion stablecoin market cap provides the liquidity backbone for these platforms, and every dollar of trading volume generates fee income for the stablecoin issuers as well. Lending protocols like Aave, Morpho, and Maple Finance also benefit indirectly. Traders on Hyperliquid often borrow stablecoins against ETH or BTC collateral to fund their perpetual positions, driving demand for lending markets. Aave and Morpho currently carry $28 billion in active loans, and a portion of that borrowing is directly attributable to perp trading activity. The supply chain extends to Ethereum and Layer-2 networks that process the underlying transactions. Each swap, liquidation, or deposit generates gas fees for validators and sequencers. If Hyperliquid and its peers continue to grow at their current pace, the demand for blockspace on Ethereum and its L2s will increase accordingly, potentially driving up base fees and benefiting ETH holders through EIP-1559 burn mechanisms. The infrastructure flywheel is self-reinforcing: more trading volume drives more lending demand, which drives more blockspace consumption, which generates more fee revenue for the entire stack.

Regulatory Implications: Revenue Sharing Triggers Howey Test Debate

The $96.3 million in monthly distributions sends a clear signal to regulators that DeFi is no longer a theoretical construct. It is a functioning financial system with measurable revenue, real users, and tangible economic output. Summer Mersinger, a CFTC commissioner, has previously argued that DeFi protocols should be treated as technology platforms rather than unregistered securities exchanges. The revenue numbers strengthen that argument by demonstrating that these protocols are not simply gambling venues but fee-generating businesses with transparent onchain accounting. Ji Hun Kim, a former SEC official, has noted that protocols returning revenue to token holders could trigger securities classification under the Howey Test, since holders are receiving profits from the efforts of others. The tension between these two regulatory frameworks will define the next phase of DeFi adoption. Betsy Farber, a partner at a major crypto law firm, recently advised clients that revenue-sharing protocols should proactively engage with regulators to establish clear compliance frameworks. The $96.3 million figure makes that engagement unavoidable. Regulators cannot ignore a system that is returning over a billion dollars annually to participants. The disclosure standards of onchain accounting give regulators better visibility into DeFi activity than the opaque books of most centralized exchanges. That transparency may be DeFi's strongest regulatory argument: a system where every distribution is verifiable on a public ledger is harder to accuse of fraud than one relying on audited but private financial statements. The regulatory outcome will determine whether these revenue-sharing models become the standard for DeFi or face legal challenges that force structural changes.

The trajectory is clear. DeFi is generating real revenue, returning it to holders, and building the infrastructure for the onchain economy. The $96.3 million monthly figure will likely grow as more users migrate from centralized exchanges to perpetual DEXs, as stablecoin adoption expands in emerging markets like Latin America, and as lending protocols deepen their liquidity pools. Serrano, a Latin American fintech founder, recently noted that users in Argentina and Brazil are already using Aave and Morpho to deposit BTC and ETH as collateral to borrow stablecoins, accessing dollar-denominated liquidity without selling their crypto. That use case alone could drive another wave of demand for Hyperliquid and its peers. A pending U.S. stablecoin bill, which would formally recognize dollar-backed stablecoins as payment instruments, could remove a key regulatory obstacle and accelerate institutional deployment into DeFi collateral markets. If passed, the legislation would provide legal clarity for banks and asset managers who currently hold back from using stablecoins as collateral for DeFi lending, unlocking a new demand channel for Aave, Morpho, and Maple Finance. The next 12 months will determine whether these revenue numbers are a cyclical peak or the beginning of a sustained shift. If Hyperliquid maintains its $50 million monthly run rate and Pump.fun continues to capture memecoin volume, the combined annual distributions could exceed $1.5 billion by mid-2027. That is not a speculative forecast. It is a linear extrapolation of current data. DeFi has crossed the threshold from experiment to infrastructure. The $96.3 million monthly distribution figure is not a ceiling. It is a floor, and the current revenue numbers already prove that point conclusively.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.