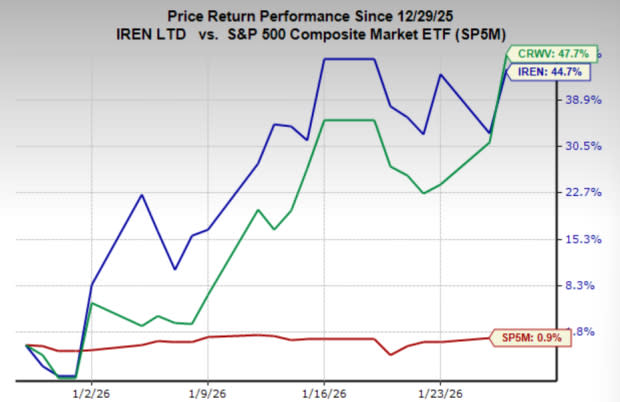

The AI infrastructure arms race accelerated sharply on Friday as Compal Electronics announced a partnership with European AI cloud provider Verda to supply next-generation GPU server systems, DeepSeek raised more than $7 billion in new funding, and Akamai Technologies surged 20% after securing a $1.8 billion commitment from a leading U.S. frontier model provider. The flurry of deals and capital raises, spanning hardware manufacturing, neocloud operators, and AI startups, underscores a market that is doubling down on compute capacity even as some players face investor skepticism. CoreWeave slid 13% after issuing Q2 revenue guidance of $2.45 billion to $2.6 billion, below the consensus estimate of $2.69 billion, while IREN Limited jumped 4% on a deal with Nvidia to deploy up to 5 gigawatts of AI infrastructure backed by a $2.1 billion investment from the chip giant. The divergence in market reactions is instructive: Akamai was rewarded for locking in a long-term anchor customer, while CoreWeave was punished for a guidance miss. This signals that investors are now scrutinizing execution and pricing power as the AI build-out enters a new phase of capital intensity. Here is why this matters now: the convergence of hardware supply deals, startup funding, and hyperscale cloud commitments is creating a winner-take-most dynamic where companies with locked-in demand and manufacturing scale are pulling ahead of pure-play capacity resellers.

Akamai's $1.8B Cloud Commitment Reshapes the CDN Giant

Akamai Technologies surged 20% after a leading U.S. frontier model provider committed $1.8 billion over seven years for its Cloud Infrastructure Services. The deal transforms Akamai from a content delivery network stalwart into a credible AI cloud contender, validating its edge-compute strategy against centralized hyperscalers. The seven-year commitment provides revenue visibility that most neocloud operators lack, and the 20% single-day stock move reflects investor recognition that long-duration contracts with frontier AI labs command premium valuations. Akamai's existing edge network, spanning thousands of points of presence, offers lower latency for inference workloads compared to centralized data centers. This structural advantage is what the $1.8 billion deal monetizes. For the frontier model provider, the commitment locks in compute capacity at a time when GPU availability remains constrained and hyperscaler pricing is volatile. The deal also pressures CoreWeave and other neocloud operators to demonstrate similar contract durability. Akamai's pivot from CDN to AI cloud infrastructure represents a strategic bet that inference, not just training, will drive the next wave of GPU demand. The $1.8 billion figure, spread over seven years, implies annual revenue of roughly $257 million from this single customer alone. That is a material addition to Akamai's cloud services segment, which had previously been a smaller, lower-margin component of its overall business mix. The deal is now the clearest proof point that Akamai's infrastructure pivot is generating bankable enterprise commitments.

DeepSeek's $7B Raise and the Startup Funding Paradox

DeepSeek is raising more than $7 billion as the Chinese AI startup plots its revenue efforts, according to The Information. The massive funding round, one of the largest for an AI startup this year, signals that investors remain willing to write enormous checks for companies that demonstrate a path to monetization. DeepSeek's raise comes at a time when the AI funding environment is bifurcated: frontier labs with proprietary models and clear enterprise use cases command premium valuations, while generic chatbot startups struggle to close rounds. The $7 billion-plus figure positions DeepSeek among the best-capitalized AI startups globally, rivaling the war chests of U.S. peers like Anthropic and xAI. The funding will be deployed primarily on compute infrastructure, including GPU clusters, data center capacity, and networking. This directly benefits hardware suppliers like Compal and Nvidia. DeepSeek's revenue planning efforts suggest the company is moving beyond research and toward commercial deployment, a shift that will increase competition in the enterprise AI market. The raise also highlights the global nature of the AI infrastructure boom: Chinese startups are raising enormous sums despite export controls on advanced chips, forcing them to optimize for available hardware. DeepSeek's $7 billion round will ripple through the supply chain, driving demand for server systems, cooling infrastructure, and data center construction across Asia.

CoreWeave's Guidance Miss and the Neocloud Reckoning

CoreWeave slid 13% after issuing Q2 revenue guidance of $2.45 billion to $2.6 billion, missing the consensus estimate of $2.69 billion. The miss, while narrow in absolute terms at roughly $90 million to $240 million below expectations, triggered a sharp sell-off because CoreWeave trades at a valuation that assumes flawless execution and accelerating growth. The neocloud operator has been a bellwether for the AI infrastructure trade, and its guidance miss raises questions about capacity utilization, pricing power, and customer concentration. CoreWeave's business model relies on leasing GPU clusters to AI startups and enterprises, a market that is becoming increasingly competitive as Akamai, IREN, and Verda expand their cloud offerings. The guidance miss reflects delayed deployments, customer churn, or pricing pressure as GPU supply improves. CoreWeave's stock slide contrasts sharply with Akamai's surge, highlighting the market's preference for companies with long-term contracts and diversified revenue streams over pure-play capacity resellers. The 13% decline erased billions in market capitalization and will force CoreWeave to provide more granular disclosure on utilization rates and contract duration in upcoming earnings calls. Analysts note that a guidance range of $2.45 billion to $2.6 billion still implies substantial sequential growth, but in a sector where expectations are calibrated to hypergrowth, even a modest miss carries disproportionate consequences. The $90 million to $240 million gap versus consensus is a rounding error at scale, yet it crystallises investor anxiety about whether neocloud operators can sustain growth trajectories as GPU supply normalises and hyperscaler pricing grows more competitive. For the broader AI infrastructure sector, CoreWeave's miss serves as a cautionary tale: rapid growth does not guarantee profitability, and investors are beginning to demand evidence of sustainable demand.

IREN-Nvidia's 5 GW Deployment and the Hyperscaler Supply Chain

IREN Limited jumped 4% after announcing a deal with Nvidia to deploy up to 5 gigawatts of AI infrastructure, with Nvidia investing $2.1 billion in the partnership. The scale of the deployment, 5 GW enough to power several million homes, underscores the immense energy and capital requirements of the AI build-out. IREN, which began as a bitcoin miner, has pivoted to AI infrastructure, leveraging its existing power procurement expertise and data center sites. Nvidia's $2.1 billion investment is both a financial commitment and a strategic signal: the chipmaker is deepening its involvement in downstream infrastructure to ensure that GPU supply translates into deployed capacity. The deal also pressures hyperscalers like Amazon Web Services, Microsoft Azure, and Google Cloud, which are racing to secure power and data center space. IREN's 5 GW deployment will require massive capital expenditure, financed through a combination of debt, equity, and customer prepayments. The partnership with Nvidia gives IREN preferred access to GPU allocation, a critical advantage in a market where lead times for H100 and B200 chips stretch months. For the supply chain, the IREN-Nvidia deal drives demand for liquid cooling systems, high-bandwidth memory, and networking equipment from suppliers like Compal, which is expanding manufacturing in Taiwan, Vietnam, and the US. The 5 GW figure also highlights the growing role of former bitcoin miners in AI infrastructure, as companies like IREN and Core Scientific repurpose their power assets for compute workloads.

Compal-Verda's European-APAC Expansion and the Manufacturing Shift

Compal Electronics will supply next-generation GPU server systems to Verda, a European AI cloud provider headquartered in Helsinki that formerly operated as DataCrunch. The partnership aims to accelerate AI infrastructure build-out across Europe and APAC, with Compal expanding manufacturing capacity in Taiwan, Vietnam, and the United States. For Compal, the deal represents a strategic move beyond its traditional laptop and PC manufacturing business into high-margin AI server systems. The company's expansion into Vietnam and the US reflects the broader trend of supply chain diversification away from China, driven by geopolitical tensions and export controls. Verda, as a European neocloud operator, gains access to Compal's manufacturing scale and supply chain expertise, enabling faster deployment of GPU clusters in regions where hyperscaler capacity is limited. The partnership is particularly significant for the European AI ecosystem, which has lagged behind the US and China in compute infrastructure. Verda's focus on European and APAC markets positions it to serve enterprises and AI startups that require data sovereignty and low-latency access. For Compal, the Verda deal adds to a growing roster of AI infrastructure customers, diversifying revenue beyond its traditional OEM clients. The manufacturing expansion in Taiwan, Vietnam, and the US also creates capacity for future deals with other neocloud operators and hyperscalers. The Compal-Verda partnership exemplifies how the AI infrastructure boom is reshaping the global electronics manufacturing landscape, with traditional OEMs pivoting to high-growth server systems.

The convergence of these deals, including Compal-Verda's hardware partnership, DeepSeek's $7 billion raise, Akamai's $1.8 billion cloud commitment, IREN's 5 GW deployment with Nvidia, and CoreWeave's guidance miss, paints a picture of a market in transition. The next 12 months will test whether the massive capital deployed into AI infrastructure translates into sustainable revenue growth or creates a capacity glut. Akamai's long-term contract model and IREN's hyperscale partnership with Nvidia represent the winning formula: locked-in demand, diversified customer bases, and strategic alignment with the chip supply chain. CoreWeave's guidance miss and Upwork's 24% workforce reduction, announced on the same day, suggest that companies without durable revenue streams face increasing investor skepticism. The AI infrastructure build-out is no longer a speculative bet. It is a capital-intensive industrial cycle that will reward operators with execution discipline, power procurement expertise, and manufacturing scale. DeepSeek's $7 billion raise ensures that the startup funding spigot remains open, but the bar for monetization is rising. Investors should watch for further consolidation among neocloud operators, as well as capacity announcements from hyperscalers that compress margins for pure-play GPU resellers. The winners will be those who control the full stack: chips, servers, data centers, and long-term customer contracts.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.