The Federal Reserve held interest rates steady at its April 2026 meeting, a decision that markets largely expected but one that carries increasingly complex implications. The central bank's updated quarterly annualized inflation forecast, released alongside the rate decision, painted a concerning picture: inflation remains stubbornly above target, and the Fed's own projections show it will not cool as quickly as previously hoped. Yet equities rallied sharply on the news. The S&P 500 climbed 1.12% to 7,340.62, the Dow Jones Industrial Average rose 1.25% to 49,913.10, and the Nasdaq gained 1.31% to 25,656.77. The VIX, Wall Street's fear gauge, fell 2.30% to 16.98, signaling a risk-on mood. Gold surged 3.18% to $4,713.90, while crude oil plunged 7.11% to $95.00. Bitcoin edged down 0.20% to $81,391.02. The market's divergent reaction, with stocks and gold rising while oil fell, reflects deep uncertainty about the path of monetary policy. The real story, however, lies in the swaps market. Traders are now pricing in a greater than 50% probability that the Fed, under Chairman Warsh, will raise rates by April 2027 before any easing cycle begins. That expectation is reshaping everything from bank balance sheets to corporate capital allocation, and it makes this rate hold far more consequential than a simple pause.

Where the Rate Hike Probability Comes From

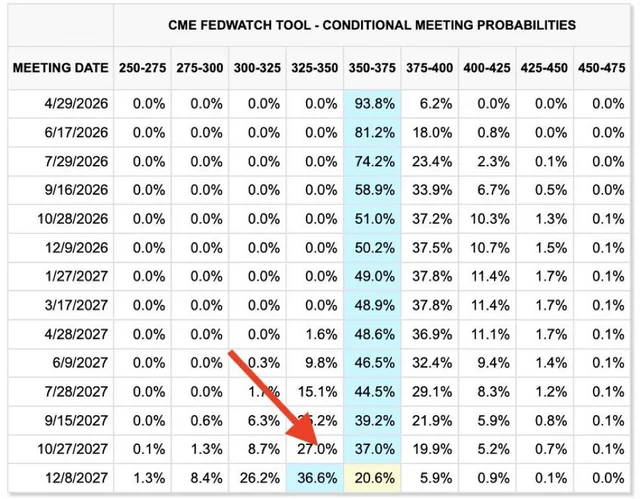

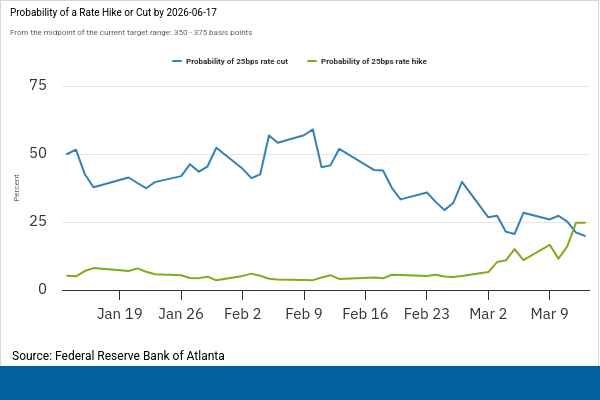

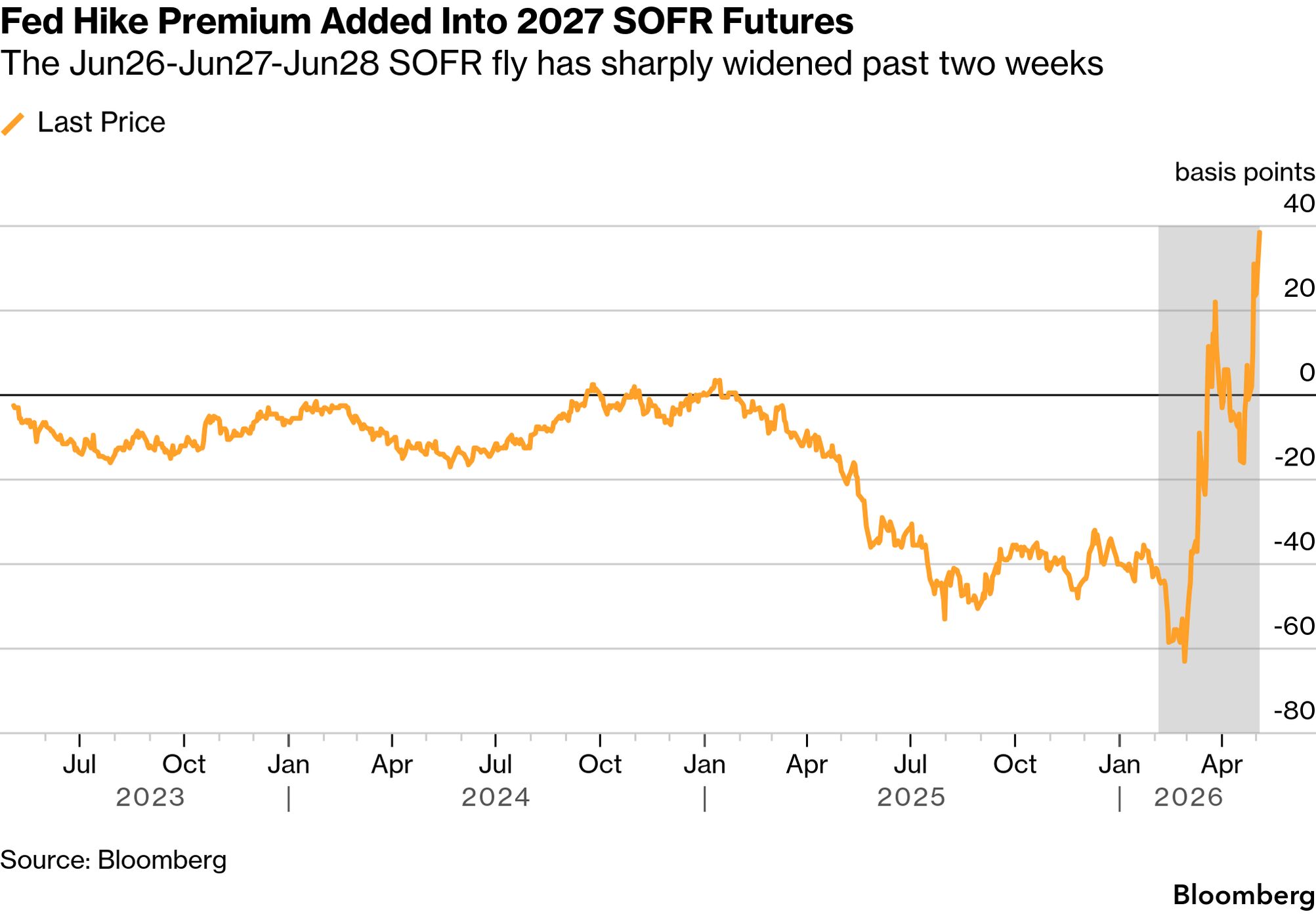

The swaps market's signal is unambiguous: traders see a better-than-even chance that the Federal Reserve will tighten policy within the next 12 months, not loosen it. Bloomberg data shows that swaps pricing implies a >50% probability of a rate hike by April 2027, before any subsequent easing. This is a striking inversion of the narrative that dominated 2025, when the Fed cut rates by 75 basis points. The shift reflects a reassessment of the inflation outlook. The Fed's own April and quarterly annualized inflation forecast, updated at the meeting, shows price pressures persisting at levels that would normally warrant a tightening bias. Chairman Warsh has not signaled a specific rate path, but the market is now pricing in a scenario where the Fed is forced to act. The mechanism is straightforward: if inflation does not decelerate meaningfully over the coming quarters, the Fed's dual mandate, balancing price stability and maximum employment, will tip toward action. The swaps curve is not predicting a crisis; it is predicting a policy error correction. Traders are betting that the 75 basis points of cuts delivered in 2025 were premature, and that the Fed will need to reverse at least some of that easing. The probability is no longer a fringe tail risk; it is the base case for a growing number of market participants.

How the Rate Hold Flows Through Bank and Consumer P&Ls

The Fed's decision to hold rates steady has immediate and measurable effects on the banking sector and consumer savings. The average savings account in the United States pays just 0.38%, according to FDIC data. But the best high-yield savings accounts continue to offer up to 5.00%, a spread that reflects the lagged pass-through of the 75 basis points of cuts delivered in 2025. With the Fed now on hold, those high-yield rates are set to plateau. Banks that raised deposit rates aggressively to attract funding during the tightening cycle are now in a stronger position to defend net interest margins. For consumers, the message is clear: the window to lock in 5.00% yields is closing, but it has not slammed shut. For banks, the hold is a reprieve. Net interest income, which had been compressed by the 2025 cuts, will stabilize. Regional banks, in particular, benefit from a pause in rate changes, as it reduces the volatility of deposit costs and loan repricing. The broader implication is that the rate hold acts as a floor under bank profitability, at least for now. If the swaps market is correct and a hike comes by April 2027, the dynamic reverses: banks see a tailwind from wider spreads, while loan demand weakens as borrowing costs rise. The hold is a temporary equilibrium, not a permanent solution.

The Competitive Reshuffle Among Tech and Industrial Giants

The rate hold creates winners and losers across the technology and industrial landscape. NVIDIA Corporation and Advanced Micro Devices, Inc., both heavily reliant on capital-intensive AI infrastructure spending, benefit from a stable rate environment that keeps financing costs predictable. Intel Corporation, which is executing a costly turnaround and foundry buildout, also gains breathing room, since higher rates would have increased the cost of its debt-funded capital expenditures. Super Micro Computer, Inc., a high-growth server and storage company, is similarly positioned to benefit from continued AI demand without the headwind of rising rates. On the other side, companies with high leverage or exposure to consumer discretionary spending face greater risk if the rate hold merely delays an eventual hike. CDW Corporation, a technology solutions provider, is sensitive to enterprise IT budgets, which tighten when borrowing costs rise. Klaviyo, Inc., a marketing automation platform, relies on small and medium business spending, which is often the first to be cut in a higher-rate environment. TransMedics Group, Inc., a medical device company, and NICE Ltd., a cloud software firm, are less directly exposed to rate cycles but face valuation compression when the market reprices risk premiums. Nokia Oyj, the telecom equipment maker, operates in a capital-intensive industry where rate stability supports carrier capex plans. Primoris Services Corporation, an infrastructure construction firm, benefits from long-term projects that are less sensitive to short-term rate moves. The net effect is a market that rewards companies with strong balance sheets and AI exposure, while punishing those with weak cash flows and high debt.

Downstream Effects on Hyperscalers, Fabs, and Enterprise Buyers

The rate hold has second-order effects that ripple through the semiconductor supply chain and enterprise technology spending. Hyperscalers, the cloud giants that drive demand for NVIDIA's GPUs and AMD's MI-series accelerators, are making multi-year capex commitments that are sensitive to the cost of capital. A stable rate environment supports those commitments, but a hike by April 2027 introduces uncertainty into 2027 budgets. Foundries and fabs, including Intel's new fabrication facilities, are long-duration assets financed with debt. The 75 basis points of cuts in 2025 lowered the cost of that debt, but the hold means those costs will not fall further. If the swaps market is right and a hike comes, the cost of funding new fab construction rises, delaying capacity additions. Enterprise buyers, who purchase IT hardware and software from companies like CDW and Super Micro, face a mixed signal. The rate hold keeps their borrowing costs stable in the near term, but the expectation of a future hike will cause them to accelerate purchases to lock in current financing terms. This pull-forward effect boosts demand in the second half of 2026, only to create a demand hole in 2027. The crude oil price drop of 7.11% to $95.00 adds another variable: lower energy costs reduce input prices for manufacturers and data centers, partially offsetting the impact of higher rates. The semiconductor industry is also watching utility rate filings closely, since data-center power contracts now exceed 1.5 gigawatts at single hyperscaler campuses, and lower oil flows directly into natural-gas-fired generation costs that anchor those contracts. The net effect is a complex web of cross-currents that makes corporate planning unusually difficult, and CFOs at Tier-1 enterprise buyers are now running 2027 capex scenarios under both a 25-basis-point hike and a continued hold.

What the Fed’s Hold Signals About the Policy Trajectory

The Fed's decision to hold rates steady, combined with the swaps market's expectation of a hike by April 2027, sends a powerful signal about the central bank's strategic posture. Chairman Warsh is effectively buying time. The 75 basis points of cuts in 2025 were a bet that inflation would recede; the April 2026 inflation forecast shows that bet has not paid off. By holding now, the Fed avoids the political and market disruption of an immediate reversal, while keeping the option to hike later. This is a deliberate strategy of optionality. The market's response, with stocks rising, gold rising, and oil falling, indicates that investors are not yet pricing in the full implications of a hike. Gold's surge to $4,713.90 reflects hedging against monetary uncertainty, while oil's collapse points to demand fears dominating supply concerns. The VIX at 16.98 is low, implying complacency. The policy signal is that the Fed is willing to tolerate above-target inflation in the near term, but only if the economy remains strong. If growth falters, the calculus changes. The swaps market's >50% probability of a hike by April 2027 is not a forecast of disaster; it is a recognition that the Fed's credibility is on the line. If inflation does not fall, the Fed will act. The hold is a strategic pause, not a directional pivot, and the calendar of the next four FOMC meetings becomes the rate market's center of gravity.

The most likely outcome over the next 12 months is that the Fed maintains its hold through the remainder of 2026, then delivers a 25-basis-point hike in early 2027 if inflation does not show sustained progress toward the 2% target. That scenario would reverse one-third of the 2025 cuts, leaving the federal funds rate still below its 2024 peak. The equity market rally on the April 2026 hold may prove to be a head fake. Better-than-expected corporate earnings and the AI evolution have boosted stocks, but those same forces are also keeping inflation elevated. The S&P 500 at 7,340.62 is pricing in a soft landing that the swaps market says is unlikely. The disconnect between the equity market and the rate market is the defining tension of this cycle. For investors, the right strategy is to favor companies with pricing power, low leverage, and exposure to secular growth trends like AI and infrastructure. High-yield savings accounts at 5.00% remain attractive relative to bonds, but the window is narrowing. The Fed has given the market a reprieve, but it has not changed the underlying math. The rate hold is a bridge to a decision, not a destination.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.