Masayoshi Son's latest gambit is not a software bet. It is a shovel-and-steel play designed to become the dominant contractor of the AI infrastructure buildout — and he wants to cash out at a nine-figure valuation before the year is over. SoftBank is creating a new company called Roze, an AI and robotics venture that will use autonomous machines to design, build, and operate data centers, according to reporting by the Financial Times, confirmed by TechCrunch and CNBC. The target listing valuation is approximately $100 billion, with Son pushing for a U.S. IPO as early as the second half of 2026.

The timing is not accidental. Data center construction has become the single largest bottleneck in the generative AI supply chain. Hyperscalers committed more than $300 billion in combined capital expenditure in 2026 alone, but the cranes, welders, and electricians needed to actually pour those foundations remain stubbornly human and stubbornly scarce. Roze is SoftBank's answer: replace labor constraints with a proprietary fleet of construction robots, sell the service to every hyperscaler that needs a rack hall by next quarter, and then IPO the entity before the infrastructure race peaks.

Autonomous Construction as Roze's Core Mechanism

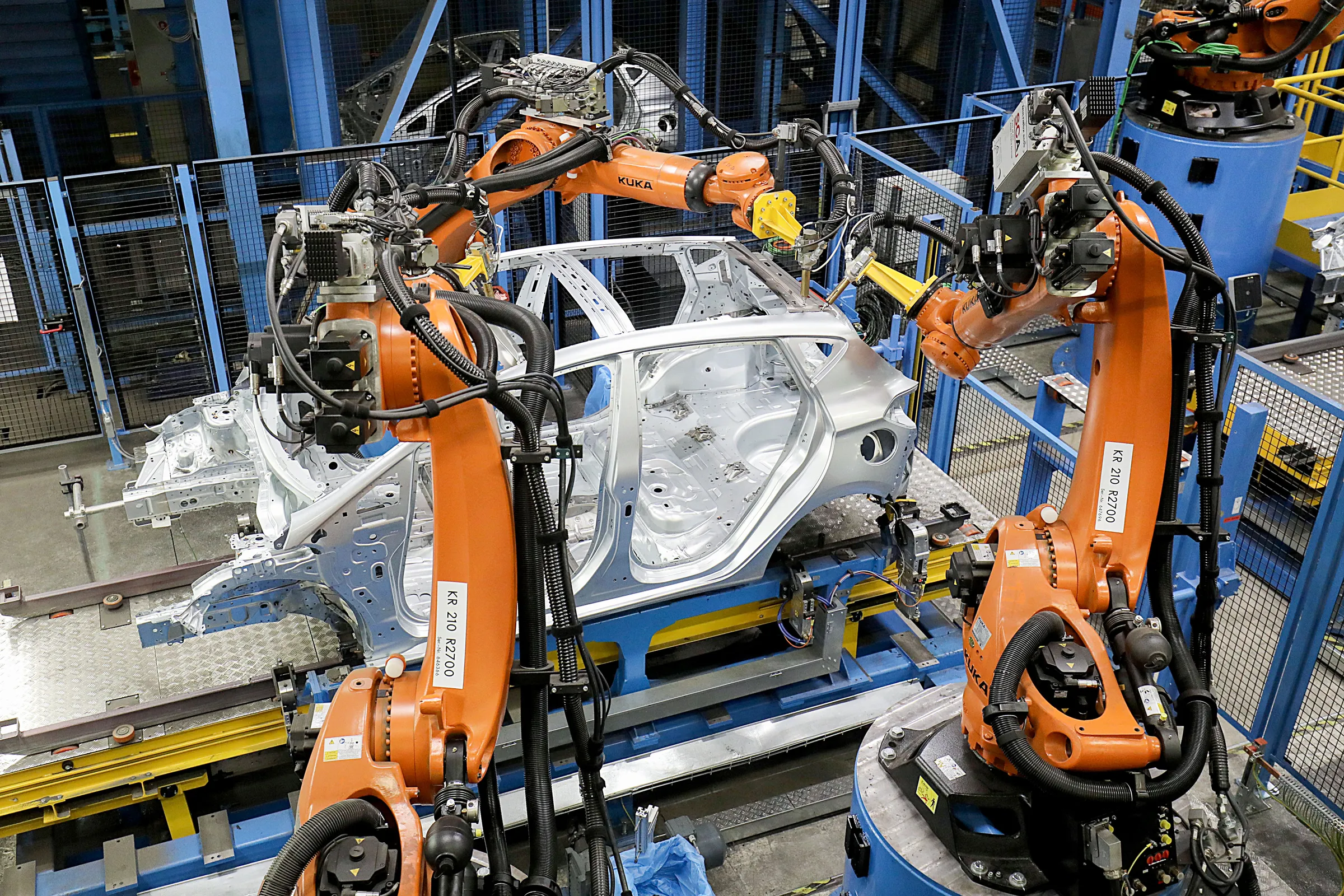

Roze will deploy autonomous robots to handle the most labor-intensive phases of data center construction: heavy lifting, steel assembly, welding, cabling, and mechanical-electrical-plumbing installation. The pitch to prospective customers is speed and repeatability at a scale no human crew can match. Where a conventional data center project can take 18 to 24 months from groundbreaking to power-on, Roze claims its robotic workflow compresses that timeline meaningfully, which translates directly into earlier rack revenue for hyperscalers whose capacity backlogs stretch well into 2028.

The technical substrate is ABB Robotics, which SoftBank agreed to acquire in 2025 and has been integrating into its portfolio. ABB is one of the world's largest suppliers of industrial automation equipment, with existing deployments in automotive, aerospace, and semiconductor fabs. Roze would wrap ABB's hardware and software capabilities in a purpose-built data center context, adding AI coordination layers to manage multi-robot job sites and real-time scheduling. SoftBank is also expected to bundle DigitalBridge assets, its existing digital infrastructure investment vehicle, along with land, power purchase agreements, and fiber corridors, effectively packaging the entire construction-to-operation stack as a single managed service.

The venture is distinct from SoftBank's earlier robotics investments, including Zume, the pizza-making robot startup that folded after burning through hundreds of millions of dollars. What separates Roze, at least in the pitch, is that data center construction is a volume, repeat-order business with clear unit economics, unlike bespoke food automation. Every hyperscaler that signs a multi-year capacity agreement is a recurring contract, not a one-off.

The IPO Math: Monetizing SoftBank's OpenAI Exposure

Son wants Roze listed primarily because SoftBank needs capital to service its commitments on the other side of the ledger. SoftBank has committed over $30 billion to OpenAI, a figure CNBC confirms, and is the lead financier of the Stargate project, the $500 billion joint venture between OpenAI, Oracle, and SoftBank itself intended to build a national U.S. AI infrastructure network. Stargate draws down cash at scale; Roze, if it lists at anything near the $100 billion target, gives SoftBank a liquid currency to fund ongoing commitments without selling down Vision Fund positions at distressed prices.

There is also a margin logic at play. SoftBank reported a $2.4 billion gain in its Vision Fund in the December 2025 quarter, suggesting the portfolio has recovered meaningfully from 2022-era writedowns, but the underlying exposures are still heavily concentrated in pre-IPO tech. A $100 billion Roze IPO would unlock balance sheet capacity that allows Son to double down on OpenAI and Stargate while keeping Vision Fund positions intact. It is a financial engineering move as much as an operational one, and analysts quoted by TechCrunch note that some insiders at SoftBank are skeptical the $100 billion figure is supportable by current revenue projections.

OpenAI itself is preparing for an IPO that could value it at approximately $1 trillion, according to Reuters via Yahoo Finance. A Son strategy that owns both a major OpenAI stake and the primary infrastructure contractor for AI data centers would create a vertically integrated position across the full AI value chain, from model to rack.

Competitive Reshuffle: Prometheus, Turner, and the Construction Giants

Roze enters a field that is already drawing attention from capital-heavy operators. Jeff Bezos is backing Project Prometheus, an industrial AI automation venture with similar goals of deploying robots in construction and logistics settings. Prometheus is less specifically focused on data centers than Roze, but it competes for the same pool of enterprise customers and the same talent: robotics engineers with industrial deployment experience are among the scarcest workers in the technology sector.

Traditional general contractors such as Turner Construction, Whiting-Turner, and DPR have dominated the data center build market for decades. These firms carry multi-billion dollar data center backlogs for Meta, Microsoft, Amazon, and Google, and they have the licensed subcontractor networks that building codes require. Roze's disruption thesis hinges on whether regulators and hyperscalers will approve robotic workers for tasks that currently require licensed human electricians and welders in most U.S. jurisdictions. That regulatory question is unresolved and represents the clearest execution risk in the model.

Among hyperscalers, the dynamics cut differently. Microsoft, which announced plans to spend up to $80 billion on AI infrastructure in fiscal 2026, would benefit materially from a faster, cheaper construction vendor. Amazon Web Services, which reported 28 percent year-over-year revenue growth in its most recent quarter while flagging capacity constraints as a near-term ceiling, is the most directly exposed to construction timeline risk. Either of these companies as an anchor customer for Roze would validate the model in ways no press release can replicate.

Supply Chain and Capex Downstream Effects

If Roze scales, it redistributes spending across the data center supply chain in measurable ways. Steel fabrication and mechanical assembly, currently provided by specialty subcontractors at margins in the 8 to 14 percent range, would be internalized. Roze would capture that margin while simultaneously compressing the labor cost line. For power-distribution and cooling-systems suppliers: Vertiv, Schneider Electric, Eaton, a faster construction timeline means faster purchase order conversion, which is nominally positive for their revenue recognition schedules.

The materials side is less disrupted. Concrete, structural steel, copper, and fiber-optic cable remain physical commodities that robots still need humans to procure, transport, and inspect. Roze's robotics advantage is densest in the repetitive assembly tasks inside the building envelope, not in site preparation or utility hookup. That boundary sets a natural ceiling on the labor displacement percentage per project, which in turn constrains how aggressively the cost savings can compress hyperscaler capex per megawatt.

HBM and GPU allocation timelines are unaffected by Roze directly. The AI chip supply chain runs separately from the building-construction supply chain. However, faster rack commissioning means hyperscalers will absorb their chip allocations faster, increasing effective demand throughput for NVIDIA, AMD, and custom silicon vendors. At the margin, a six-month construction compression at a 100-megawatt campus translates to meaningful acceleration in chip revenue recognition for whoever holds the supply contracts.

ABB Robotics' integration is the near-term execution gate. ABB operates globally with existing contracts in automotive and pharmaceutical manufacturing; reorienting those capabilities toward custom data center workflows requires significant engineering work that likely extends well into 2027. Analysts at TechCrunch note the IPO timeline ambition (second half of 2026) is tight relative to the technical integration work required.

Son's Infrastructure Doctrine: Owning the Stack from Robot to Token

The creation of Roze completes a structural play Son has been building since at least 2024. The Stargate commitment gave SoftBank a position at the center of U.S. AI infrastructure policy. The OpenAI stake gave it exposure to the frontier model layer. ABB Robotics gave it industrial automation hardware. Roze would be the operating entity that binds those assets into a revenue-generating business with its own public float and market valuation.

This is not Son's first attempt at a vertically integrated technology empire. SoftBank's Vision Fund 1 tried to own the stack from co-working space (WeWork) to ride-sharing (Uber and Didi) to insurance (Lemonade), with famously mixed results. What differentiates the current architecture is that each component, OpenAI, ABB Robotics, Stargate, DigitalBridge, is a real business with real revenue and real enterprise customers, rather than pre-revenue consumer moonshots burning cash on customer acquisition.

The internal skepticism reported by TechCrunch is worth noting clearly. A $100 billion valuation for a company that does not yet exist, in a market segment it has not yet entered, deploying technology that has not yet been certified for commercial construction use in the United States, is an ambitious anchor. Comparable construction automation companies trade at far lower multiples. The premium Son is claiming reflects the AI infrastructure narrative, not construction industry fundamentals, which means Roze's listing price will be highly sensitive to whether the broader AI capex cycle continues through 2027 or begins to moderate.

Whether the public markets are still receptive to nine-figure infrastructure IPOs by the second half of 2026 depends on factors Son cannot control: interest rates, hyperscaler earnings revisions, and the pace of AI model adoption at the enterprise level. The window is real; it is also likely shorter than the Roze timeline assumes.

SoftBank's creation of Roze is the clearest signal yet that the AI infrastructure buildout is generating its own secondary investment cycle, with companies formed not to build the models or train the chips, but to construct the physical plants those models require. If Roze executes on its construction robotics thesis and lists successfully at a significant fraction of its target valuation, it will validate autonomous construction at a scale no prior proof point has established. If it cannot translate ABB's industrial robotics into certified, code-compliant data center construction by mid-2027, the $100 billion number will look like the kind of forward narrative that tends to age poorly. Son's track record includes both outcomes in roughly equal measure.

The BossBlog Daily

Essential insights on AI, Finance, and Tech. Delivered every morning. No noise.

Unsubscribe anytime. No spam.

Tools mentioned

AffiliateSelected partner tools related to this topic.

AI Copilot Suite

Content drafting, summarization, and workflow automation.

Try AI Copilot →

AI Model Monitoring

Track model quality, latency, and drift with alerts.

View Monitoring Tool →

Low-fee Global Broker

Multi-market access with transparent pricing.

Open Broker Account →

Some links above are affiliate links. We earn a commission if you sign up through them, at no extra cost to you. Affiliate revenue does not influence editorial coverage. See methodology.